ECO 1104 Chapter Notes - Chapter 13: Average Cost, Variable Cost, Marginal Cost

13 Apr 2017

School

Department

Course

Professor

16

ECO 1104 Full Course Notes

Verified Note

16 documents

Document Summary

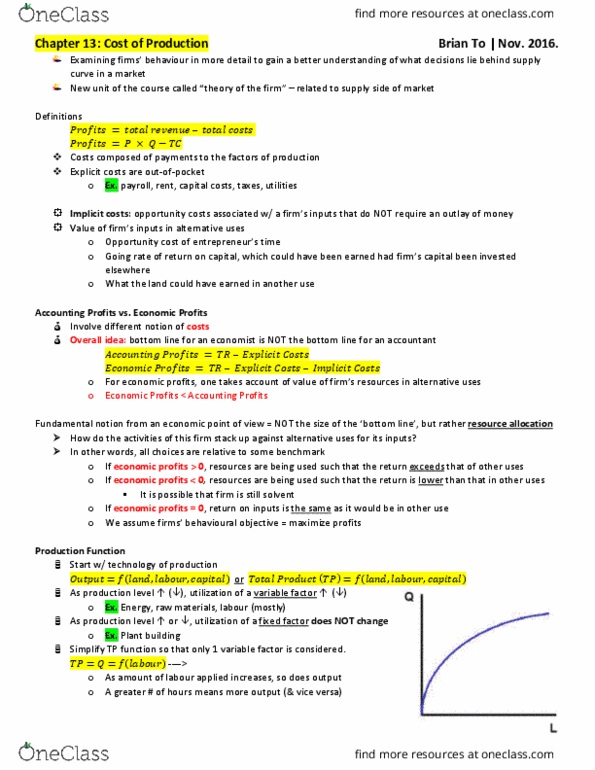

Profits = p x q tc: costs composed of payments to the factors of production, explicit costs are out-of-pocket. Payroll, rent, capital costs, taxes, utilities: implicit costs: opportunity costs associated with a firm"s inputs that do not require and outlay of money, value of firm"s inputs in alternative uses. Going rate of return on capital, which could have been earned had firm"s capital been invested elsewhere. What the land could have earned in another use. Economic profits = tr explicit costs implicit costs. Production and costs: the production function: the relationship between the quantity of inputs (workers) and quantity of output (cookies), example: A production function shows the relationship between the number of workers hired and the quantity of output produced. Here the number of workers hired (on the horizontal axis) is from the first column in table 13. 1, and the quantity of output produced (on the vertical axis) is from the second column.