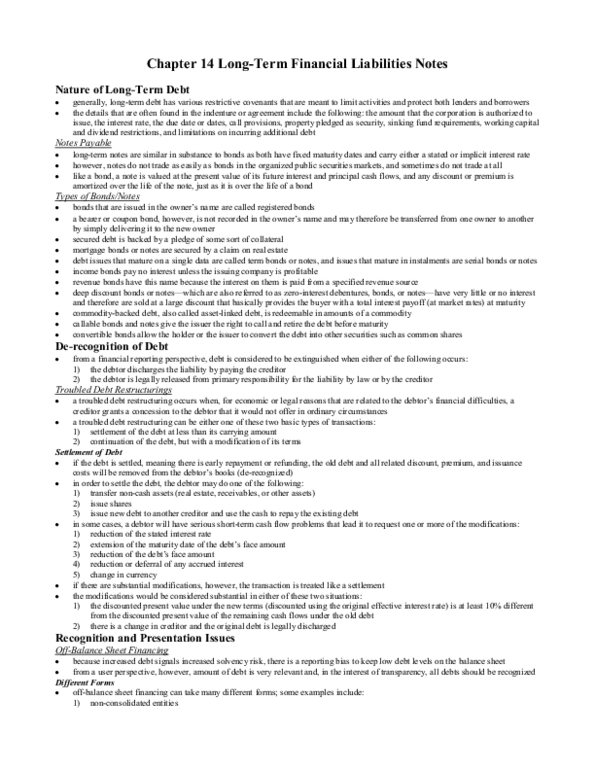

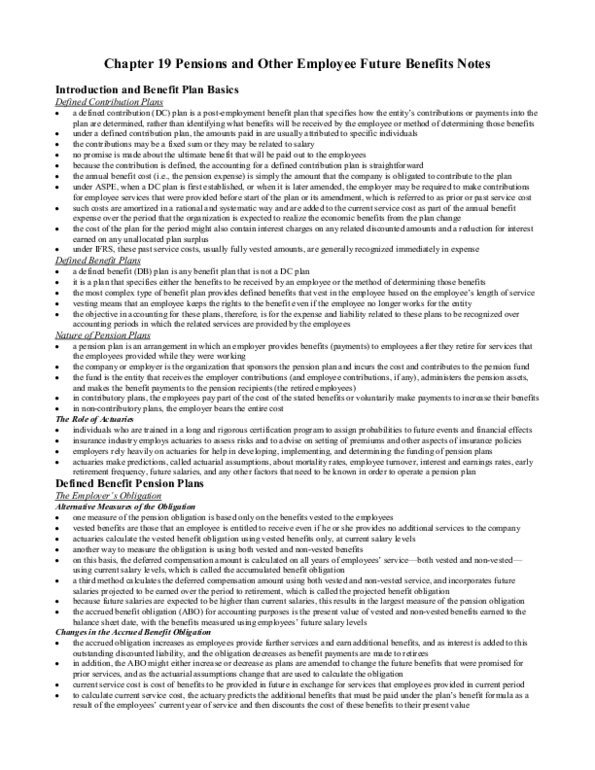

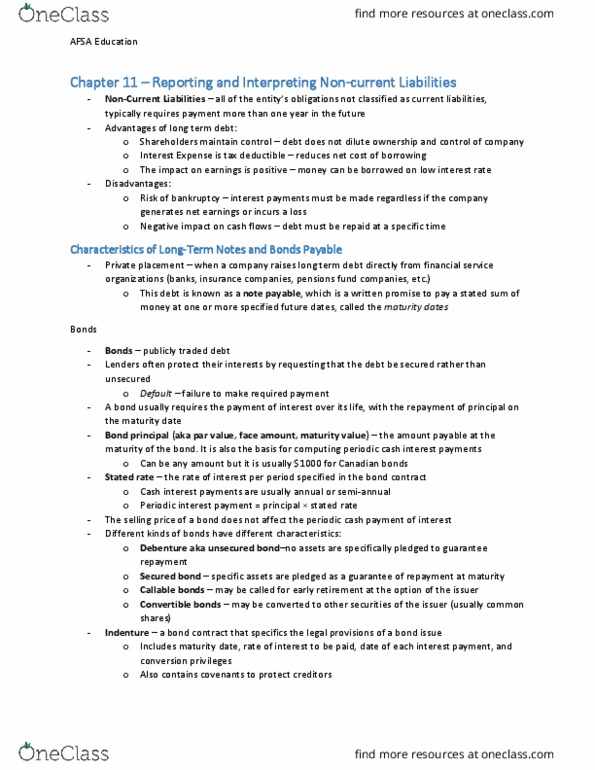

MGAC02H3 Chapter Notes - Chapter 11: Effective Interest Rate, Convertible Bond, Premium Bond

24 views4 pages

Document Summary

Private placement: raising debt from banks, insurance companies, and pension fund companies. Note payable: a written promise to pay a stated sum of money at one or more specified future dates (maturity date) Bonds: the amount payable at the maturity of the bond. It is also the basis for computing periodic cash interest payments. Requires payment of interest over its life. The amount payable at the maturity date. The basis for computing periodic cash interest payments. Par value and face amount: other names for bond principal or the maturity value of a bond. Stated rate: the rate of interest per period specified in the bond contract. Different types of bonds have different characteristics, for good economic reasons; different types of creditors have different types of risk and return preference. No assets are pledged as a guarantee of repayment at maturity. Specific assets are pledged as a guarantee of repayment at maturity.

Get access

Grade+

$40 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

10 Verified Answers

Class+

$30 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

7 Verified Answers

Related Documents

Related Questions

| For each of thebonds listed below, record the three requested journalentries. | ||||

| Dates and descriptions are notrequired. | ||||

| The Dorchester Companyinvested $100,000 in 5-year bonds. The bonds were purchased at parand bear interest at a rate of 8% per annum, payablesemiannually. | ||||

| (a) | Prepare the journal entry to record the initialinvestment. | |||

| (b) | Prepare the journal entry that Dorchester wouldrecord on each interest date. | |||

| (c) | Prepare the journal entry that Dorchester wouldrecord at maturity of the bonds. | |||

| a | Investment in bond | 100,000 | ||

| Cash | 100,000 | |||

| b | Cash | 4,000 | ||

| Interest income | 4,000 | |||

| c | Cash | 100,000 | ||

| Investment in bond | 100,000 | |||

| The Dorchester Companyinvested $100,000 of face amount of 5-year bonds. The bonds werepurchased at 103 and bear interest at a stated rate of 8% perannum, payable semiannually. | ||||

| (a) | Prepare the journal entry to record the initialinvestment. | |||

| (b) | Prepare the journal entry that Dorchester wouldrecord on each interest date. | |||

| (c) | Prepare the journal entry that Dorchester wouldrecord at maturity of the bonds. | |||

| a | ||||

| b | ||||

| c | ||||

| The Dorchester Companyinvested $100,000 of face amount of 4-year bonds. The bonds werepurchased at 98 and bear interest at a stated rate of 8% per annum,payable semiannually. | ||||

| (a) | Prepare the journal entry to record the initialinvestment. | |||

| (b) | Prepare the journal entry that Dorchester wouldrecord on each interest date. | |||

| (c) | Prepare the journal entry that Dorchester wouldrecord at maturity of the bonds. | |||