RSM222H1 Chapter Notes - Chapter 3-5: Cross-Functional Team, Cost Driver, Activity-Based Costing

Document Summary

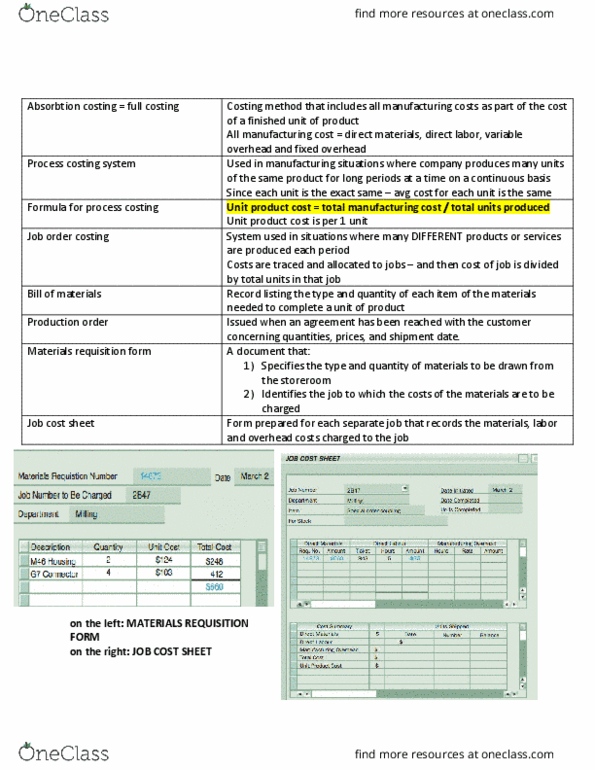

The way a product is costed can have an impact on net income and management decisions. The purpose is to provide cost data to help managers plan, control, direct, and make decisions. However, external financial reporting and tax requirements may affect how costs are summarized in managerial reports. Absorption costing a method of costing that includes all manufacturing costs direct materials, direct labour, and both variable and fixed overhead as part of the cost of a finished product. Process costing system used in manufacturing situations where a single, homogeneous product is produced for long periods of time (like paper, bottles, and hot dogs). Unit product cost is calculated by dividing total manu cost by the total units produced. Job-order costing system used in situations where many different products, jobs, or services are produced each period. Usually products are done in batches or jobs.