RSM324H1 Chapter 4: RSM324H1 Chapter : Taxable+benefits

Document Summary

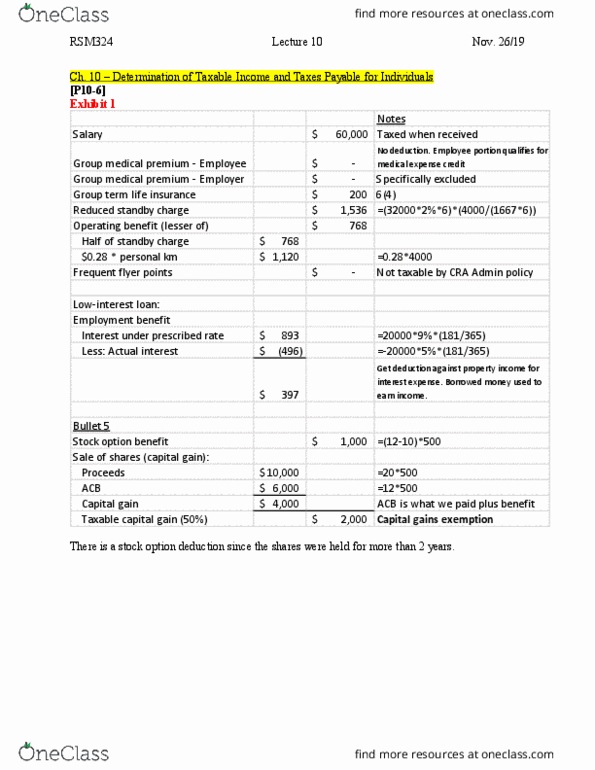

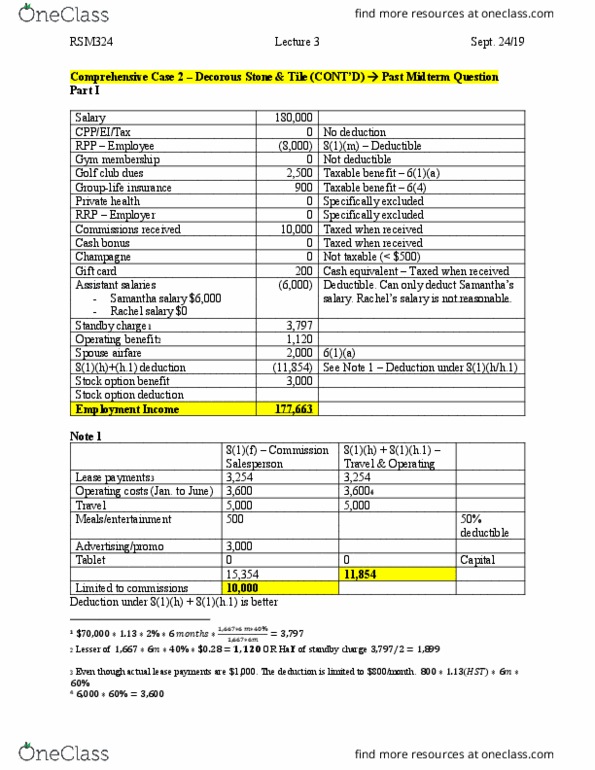

A taxable benefit arises to the extent that an employer provided automobile is for personal use. Reduced standby charge: applicable when distance travelled is primarily (i. e. , greater than 50% of the total use) for employment duties, reduced standby charge = (personal km driven / 1,667 km per month) x standby charge. Operating benefit (costs associated with operating the vehicle) Employer provides automobile: based on actual personal use of employer provided automobile, operating benefit = prescribed rate [sh. 26] x # personal km driven [ita 6(1)(k)] If automobile is used primarily for employment duties (i. e. , greater than 50% of the total use), the taxpayer may choose an alternative method to compute the operating benefit: one-half of the standby charge [ita 6(1)(k)] If employee uses own automobile and employer pays some (or all) of the operating expenses, the operating benefit is actual operating costs paid by the employer prorated for personal use by the employee [ita 6(1)(l)]