BU247 Chapter Notes - Chapter 10: Cash Flow, Income Statement

Document Summary

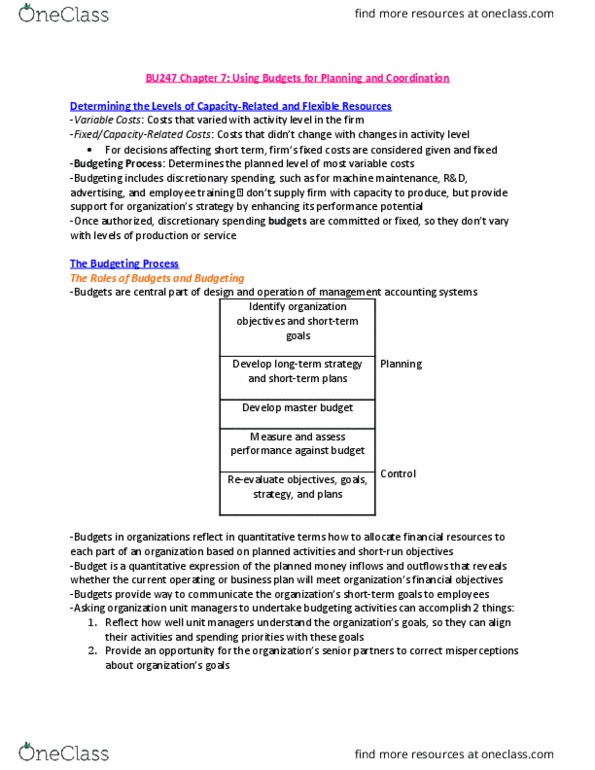

Budgets are a central part of the design and operation of management accounting systems. A budget is a quantitative expression of the planned money inflows and outflows that reveals whether the current operating or business plan will meet the organization"s financial objectives. Budgeting also serves to coordinate the many activities of an organization. A budget helps to anticipate potential problems and can serve as a tool to help provide solutions to these problems. The elements of budgeting: flexible resources that create variable costs ex. Lumber, glue, varnish: intermediate-term capacity resources that create fixed costs ex. A new fabrication facility for a computer chip manufacturer, which might take several years to plan and build and might be used for 10 years. The budgeting process describes the acquisition, production, selling, and logistical activities performed during the budget period. Planners present the expected financial results in three forms: a statement of expected cash flows, the projected balance sheet, the projected income statement.