EC140 Chapter Notes - Chapter 24: Large Deviations Theory, Automatic Stabilizer, Output Gap

16 views5 pages

21

EC140 Full Course Notes

Verified Note

21 documents

Document Summary

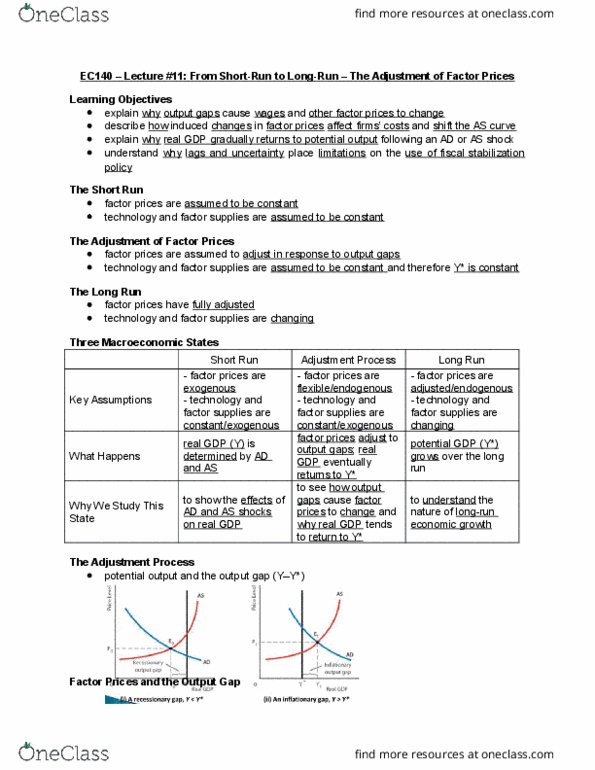

These are the two defining assumptions of the short run in our macroeconomic model: Factor prices are assumed to be exogenous; they may change, but any change is not explained within the model. Our theory of the adjustment process that takes the economy from the short run to the long run is based on the following assumptions: Factor prices are assumed to adjust in response to output gaps. Technology and factor supplies are assumed to be constant (and therefore y* is constant) Our theory of the adjustment process is useful for seeing how the effects of shocks or policies differ from the short run to the long run. The assumption that potential output is constant leads to the prediction that ad or as shocks have no long run effect on real gdp; output eventually returns to y* In reality, neither technology nor factor supplies are constant over time, however we hold them constant for simplification in our purposes.

Get access

Grade+

$40 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

10 Verified Answers

Class+

$30 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

7 Verified Answers

Related Documents

Related Questions

| a) | In the AD-AS model, stagflation does not persist, because the working of the self-correcting mechanism of the economy _____ the level of output and _____ the price level until the economy eventually returns to a long-run equilibrium state, where actual output _____ potential output.

|

| b) | The LRAS curve is drawn as a vertical line at potential output (Y*) to indicate that

|

| c) | Stagflation arises in the context of the AD-AS model when some external factor causes

|

| d) | If the SRAS curve is positively sloped, then a decrease in the demand for Canadian-made goods in Europe will lead to _____ in the price level, in the short run.

|

| e) | Which of the following will shift the aggregate demand curve to the right?

|

| f) | Suppose a stock market crash decreases the stock of household wealth and therefore causes autonomous consumption to fall. Which of the following is the likely result?

|

| g) | An economy is characterized by the AD equation P = 200 ? 0.02Y, SRAS equation P = 100 and LRAS equation Y* = 5000. In the absence of any change in policy or exogenous shocks, this economy will achieve a long-run price level of

|

| h) | The AD-AS model depicts a self-correcting economy. This means that the price level in the model adjusts automatically in response to a(n) _____ gap, so as to eliminate the _____ gap in the long run, without requiring any help from government policies.

|

| i) | The aggregate demand curve shows

|

| j) | Consider an economy initially at long-run equilibrium with output (Y) equal to potential output (Y*). If the SRAS is positively sloped, then a shift to the right of the AD curve will lead to _____ in the price level, in the short run. In the long run, the SRAS curve will shift to the _____ and the equilibrium will be at __________.

|