ACCT 2001 Chapter : Ch 02 Study Guide HERO

Document Summary

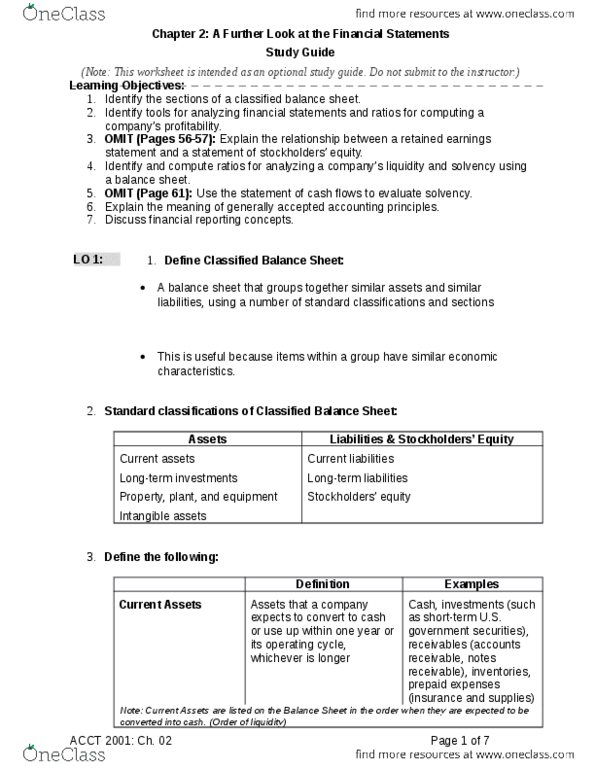

Chapter 2: a further look at the financial statements. Assets that companies expect to convert to cash or use up within one year or the operating cycle, whichever is longer. Cash, investments, receivables (accounts receivable, notes receivable, and interest receivable), inventories, prepaid expenses (insurance and supplies) Note: current assets are listed on the balance sheet in the order when they are expected to be converted into cash. (order of liquidity) The average time required to purchase inventory, sell it on account, and then collect cash from customers- that is, go from cash to cash. Assets that can be converted into cash, but whose conversion is not expected within one year. Assets not intended for use within the business. Assets with relatively long useful lives that are currently used in operating the business. Investments of stocks and bonds of other corporations. The allocation of the cost of an asset to a number of years.