MGMT 20000 Chapter Notes - Chapter 3: Deferral, General Ledger, Retained Earnings

30 Jun 2016

School

Department

Course

Professor

Document Summary

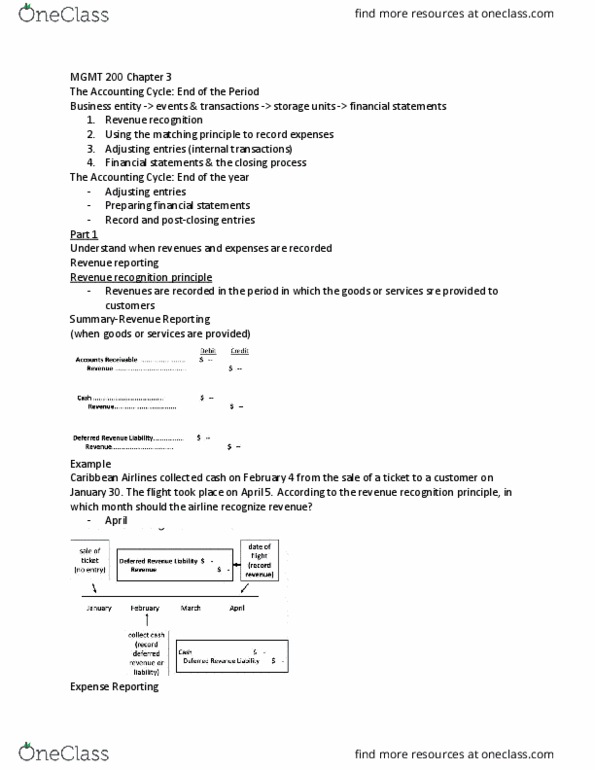

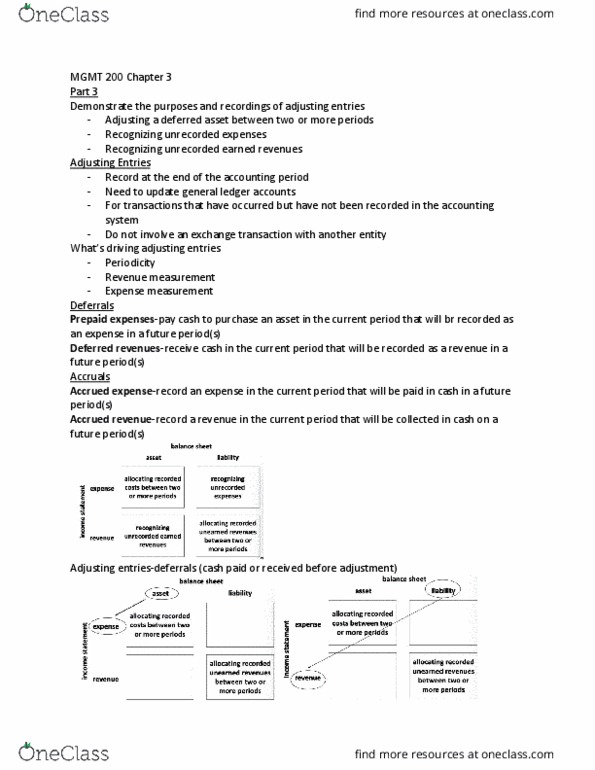

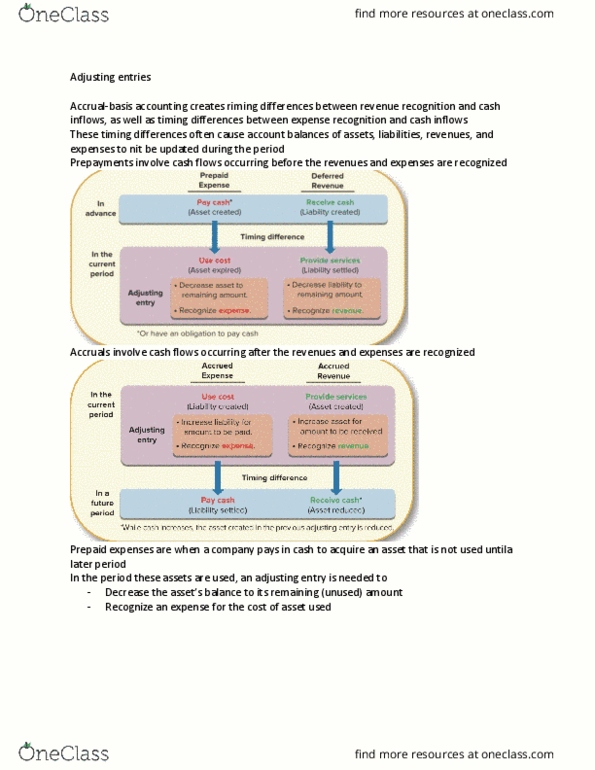

Learning objective 1 - understand when revenues and expenses are recorded. Expenses are reported with the revenues they help to generate. To account for transactions that have not been recorded by the tend of the period. Cost of assets acquired in one period that will be expensed in a future period: we paid in advance. Cash received in advance from a customer for products or services to be provided in the future: we owe the customer, accruals. Company has incurred a cost but hasn"t yet paid cash or recorded an obligation. Revenue earned but hasn"t yet received cash or recorded an amount receivable. Learning objective 4 - post adjusting entries and prepare an adjusted trial balance. Lists all account balances after updating them for adjusting entries. Prepared after posting the adjusting entries to the general ledger. Measures activities involving cash receipts and cash payments. To transfer the balances of temporary accounts to the retained earnings.