MGMT 20000 Chapter Notes - Chapter 2: General Ledger, Retained Earnings, Regional Policy Of The European Union

30 Jun 2016

School

Department

Course

Professor

Document Summary

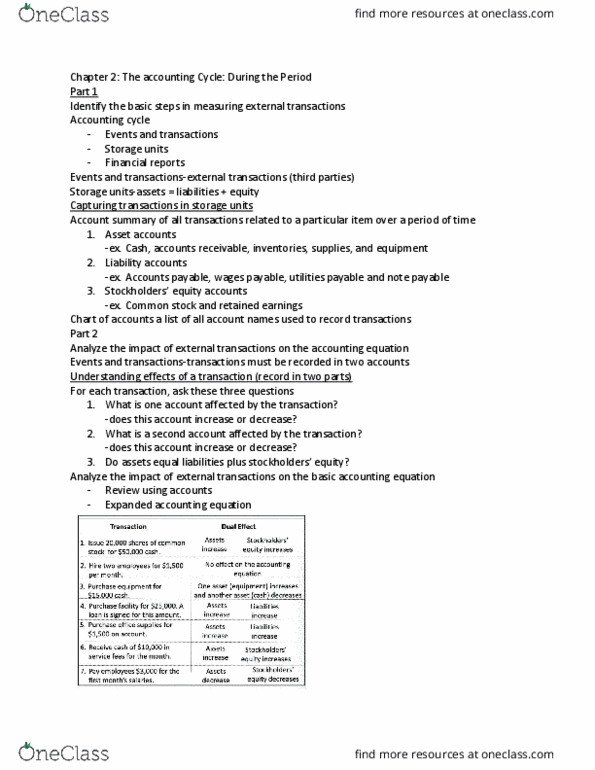

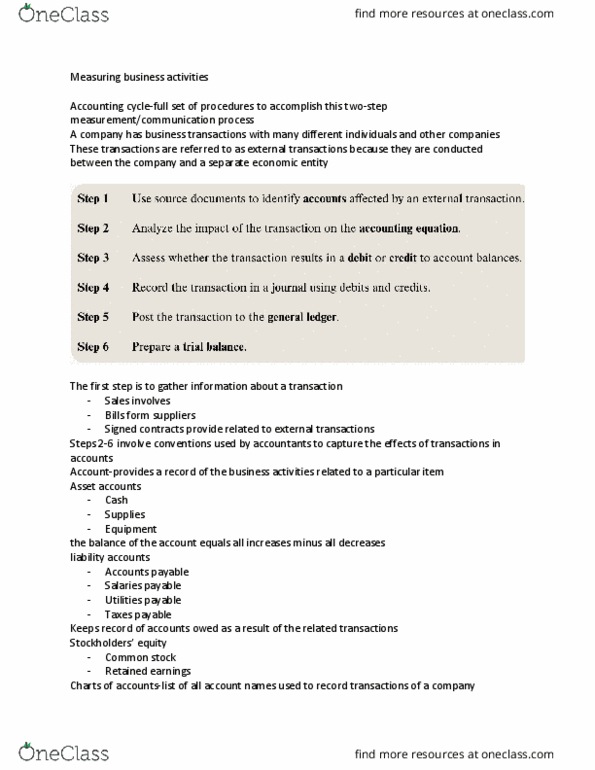

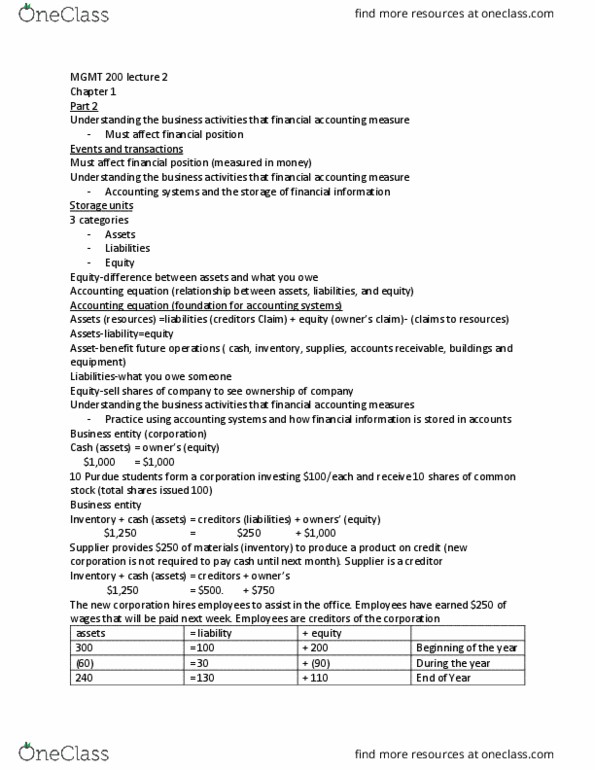

Learning objective 1 identify the basic steps in measuring external transaction. External transactions: transactions conducted with a separate economic entity. Internal transaction: events that affect the financial position of the company but do not include an exchange with a separate economic entity. Account: summary of all transactions related to a particular item over a period of time, asset accounts: Cash, supplies, and equipment: liability accounts: Accounts payable, salaries payable, utilities payable, and taxes payable: stockholders" equity account: Chart of accounts: a list of all account names used to record transactions. Measuring external transactions is a six-step process: gathering information about a transaction. Source documents such as sales invoices, bills from suppliers, and signed contracts provide information related to external transactions. These source documents are used to determine the accounts that will be affected: next, the effect of the transaction on elements of the accounting equation must be analyzed. After each transaction, assets must always equal liabilities plus stockholders" equity.