ACCT 2102 Chapter Notes - Chapter 9: Cost Driver, Profit Margin, Contribution Margin

2 May 2016

School

Department

Course

Professor

Document Summary

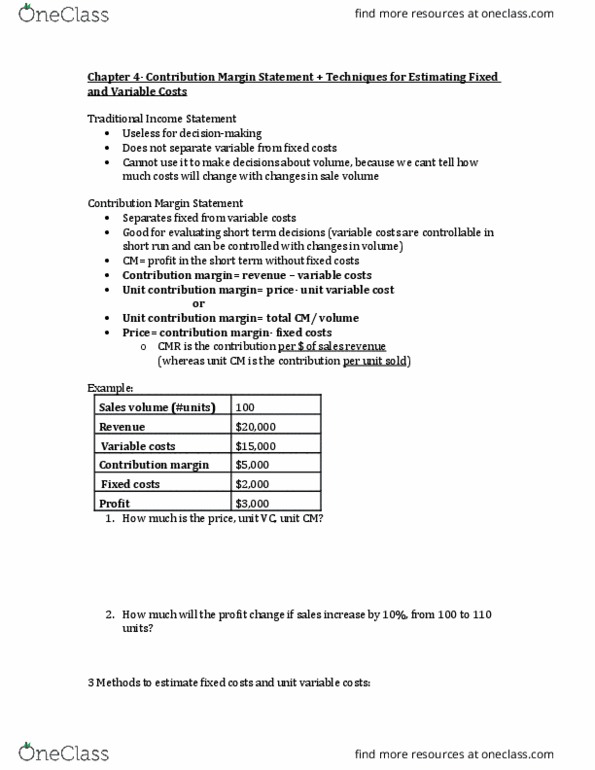

Capacity costs are controllable in the long term: aka fixed costs, ex. adding/removing machines, hiring/firing workers. In the long-term, we focus on maximizing the profit margin, not the contribution margin. Profit margin (for a given product line) = = contribution margin allocated capacity costs aka fixed costs. = (revenue variable cost) allocated capacity costs aka fixed costs: to evaluate long-term decisions, need to estimate the change in capacity costs => use cost allocation to do that. Cant be traced to individual product lines. A large fraction of total costs: want to know: How to divide them among the two product lines. How they will change with decisions in the long term. % capacity costs used by each product line is roughly proportional to its % use of the cost driver in the long term, capacity costs change roughly in proportion to changes in the cost driver amounts.