ACIS 3115 Chapter Notes - Chapter 20: Error Detection And Correction

2 Nov 2016

School

Department

Course

Professor

Document Summary

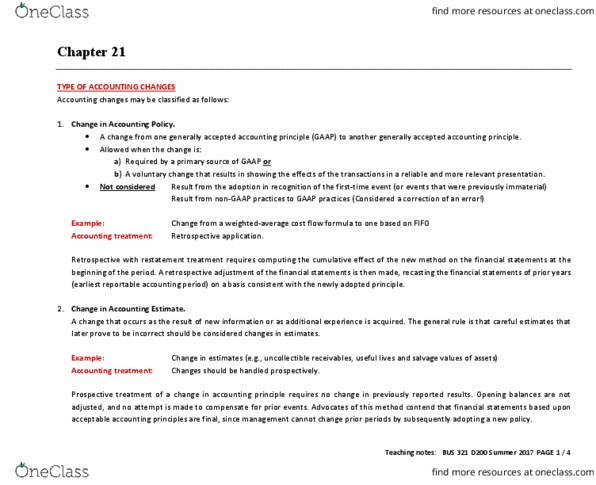

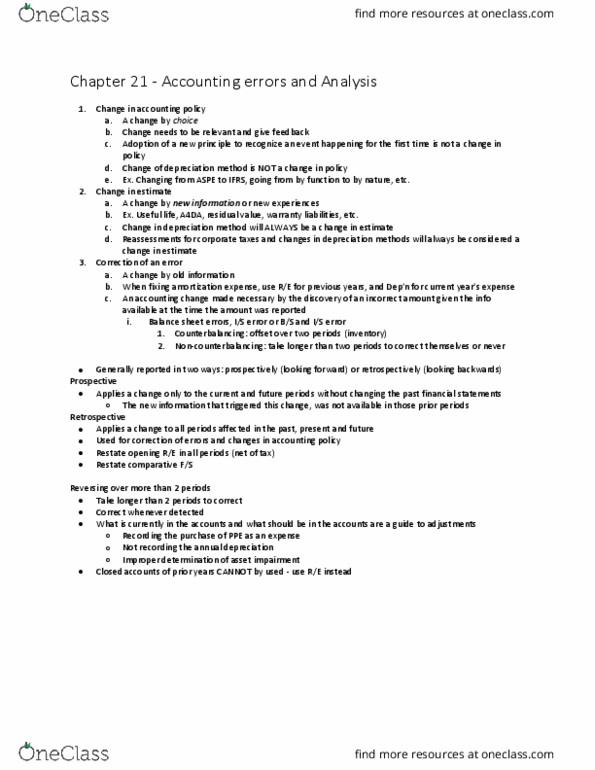

Accounting changes: changes in accounting principle, change from 1 method to another, inventory, adopt new standard, usually reported retrospectively, redo prior f/s with the new method, make je to adjust, disclosure note!! Changes in reporting entity ---report consolidated f/s in place of individual statements. When transaction is recorded incorrectly or not at all. Can retrospecitvley change inventory but have to repat taxes. Lifo produces higher cogs than fifo & lower inventiory. When rising costs, fifo produces lower cogs, hight ni & re. Sometimes cant do if don"t have enough info. If its impractiale to ajdust each year reported, apply change retrospecitibley as of earlist practile datew. Effects on mgt compensation, existing debt, union negotions, income smoothing. Full retrospective application of ifrs for co"s first ifrs f/s. First must include at least 3 b/s & two of each of other f/s. Full retrospective is basic requirment but theres exeception to avoid costs or difficultures.