ECON 103 Lecture Notes - Lecture 7: Tax Incidence, Economic Equilibrium, Price Ceiling

18 Aug 2018

School

Department

Course

Professor

Document Summary

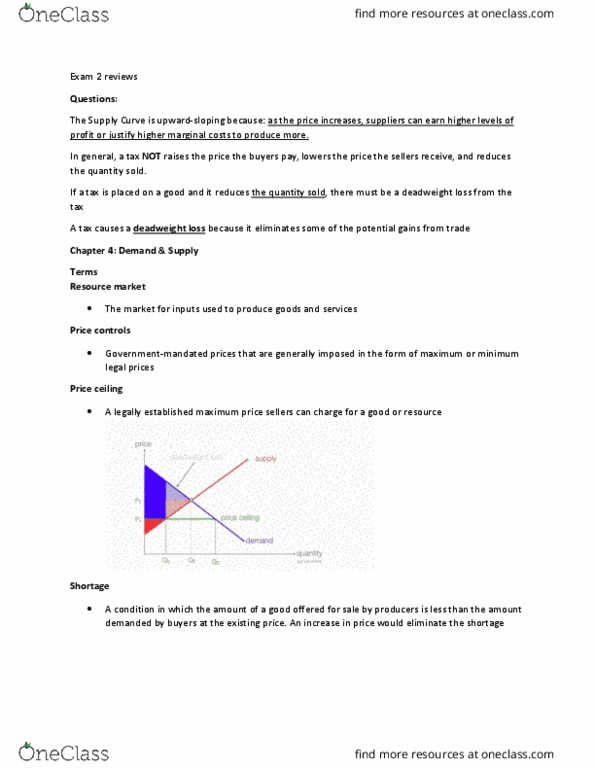

Chapter 4: demand and supply application and extensions cont. Price controls government mandated prices that are generally imposed in the form of maximum or minimum legal prices. Shortage a condition in which amount of good offered for sale by producer is less than amount demand: excess demand: Price ceiling a legally established maximum price sellers can charge for a good or resource: a price ceiling below market equilibrium price creates a shortage, a price ceiling above market equilibrium price does nothing. Rent controls lead to shortages as well as: black markets, a decline in the supply of future rental housing, a decline in quality of rental housing, non-price methods of rationing. A tax on a product will cause the supply curve to shift left by the amount of the tax: raises the price that buyers pay, reduces the amount sellers receive, reduces the quantity sold, creates deadweight loss.