BUS 101 Lecture : Chap6BUS101N2

Document Summary

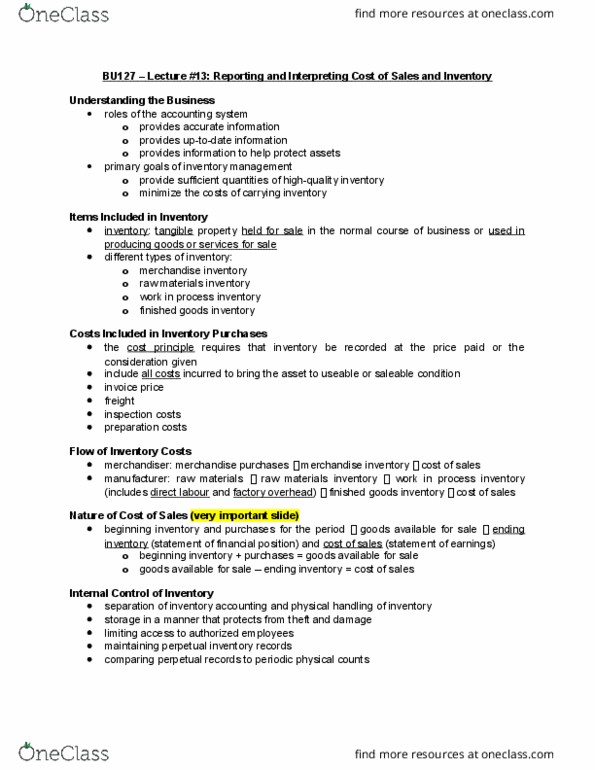

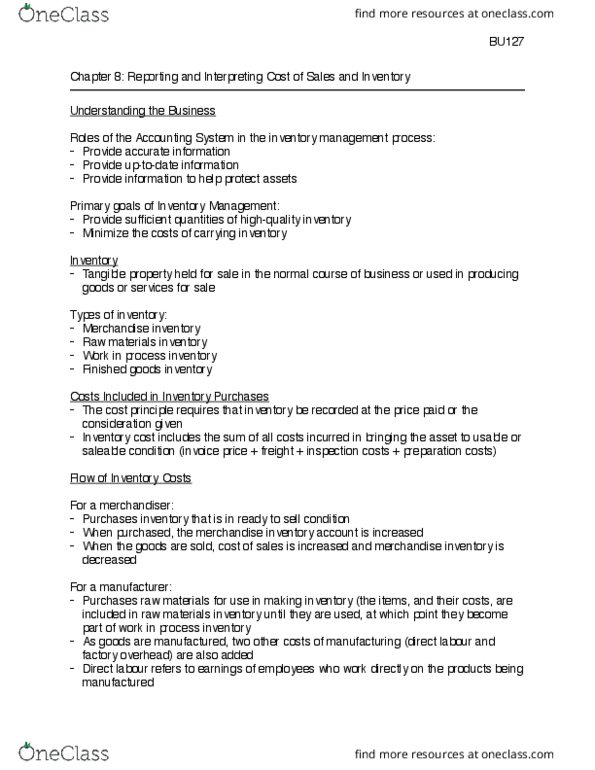

Chapter 6 inventories and cost of sales notes. Most businesses do a physical inventory count at least once a year. An adjustment must be made if the physical count does not match the. To assign costs to inventories and cost of goods sold, four approaches are used: unique identification, first-in, first-out (fifo, first in, first out (lifo, average weighted. Compute inventory in a perpetual system using the methods of specific identification, fifo, lifo and weighted average. The unique identification approach is related to inventory valuation, specifically tracking each individual item in inventory and assigning costs separately rather than grouping products together. When a corporation can identify, mark, and track each item or unit in its inventory, it is functional and useable. First in, first out (fifo) is an accounting principle that states that assets purchased or acquired first are disposed of first. Fifo assumes that the remaining inventory comprises of the most recently acquired products.