ACCT 101 Lecture Notes - Lecture 2: Promissory Note, Retained Earnings, Accounts Payable

Document Summary

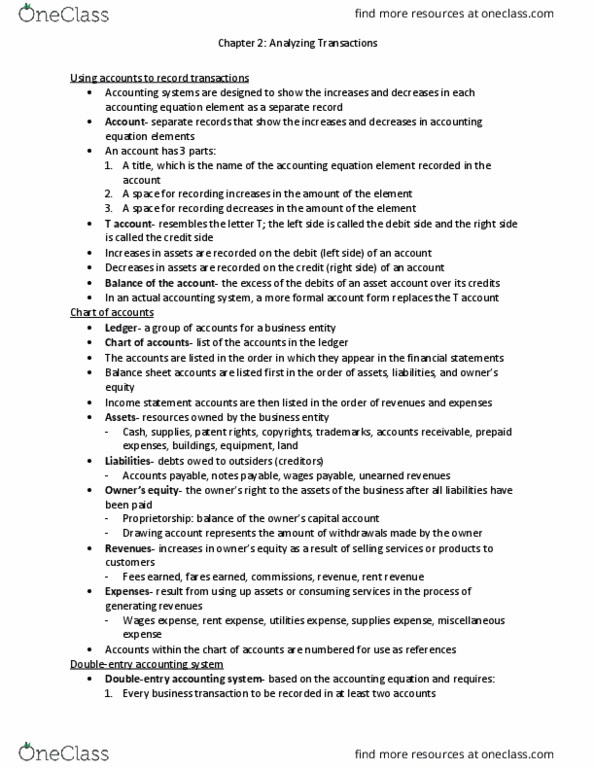

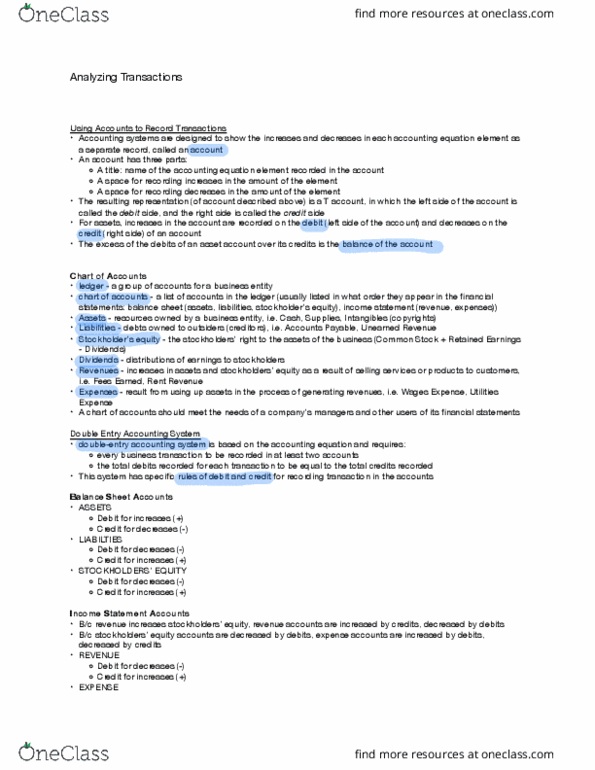

Accounting systems are designed to show the increases and decreases in each accounting equation element as a separate record. To illustrate, the cash column of exhibit 1 records the increases and decreases in cash. Likewise, the other columns in exhibit 1 record the increases and decreases in the other accounting equation elements. Each of these columns can be organized into a separate account. An account, in its simplest form, has three parts: A title, which is the name of the accounting equation element recorded in the account. A space for recording increases in the amount of the element. A space for recording decreases in the amount of the element. The account form that follows is called a t account because it resembles the letter: the left side of the account is called the debit side, and the right side is called the credit side.