22107 Lecture Notes - Lecture 7: Perpetual Inventory, Moving Average, Current Asset

UTS 2014 – Accounting for Business Decisions A

Page 30

LECTURE 7 – INVENTORY – RETAIL OPERATIONS

LEARNING OBJECTIVES

Describe inventory and how it is recorded, expensed and reported.

Inventory is a tangible resource that is held for resale in the normal course of operations.

The phrase “intended for resale” differentiates inventory from other assets.

For a retailer, inventory is the stock (merchandise) on the shelves or in the warehouse.

For a manufacturer, inventory also includes the raw materials and work in process related to

producing a finished product.

RECORDING INVENTORY

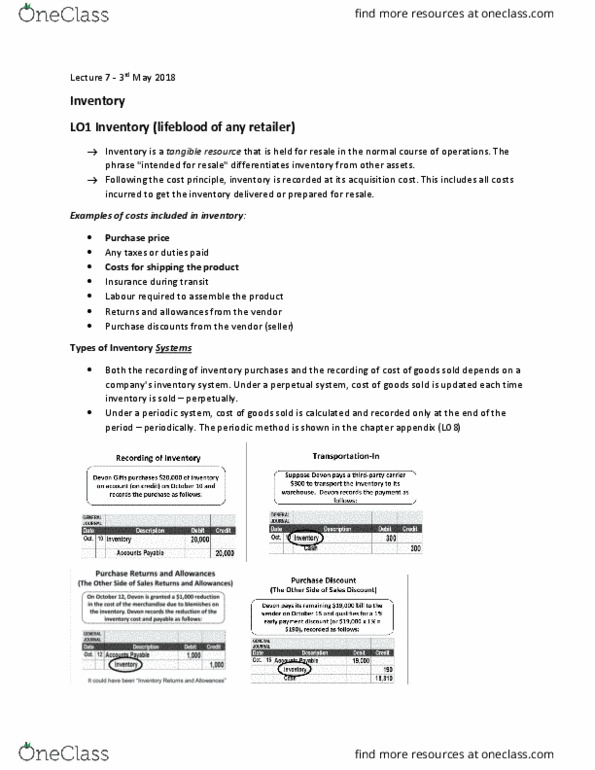

Following the cost principle, inventory is recorded at its acquisition cost. This includes all

costs incurred to get the inventory delivered and, if necessary, prepared for resale. It also

includes any reductions granted by the vendor or supplier after purchase.

Examples of items affecting the cost of inventory would include, but not be limited to –

purchase price, taxes paid, costs for shipping the product, insurance during transit, labour

required to assemble product, returns to and allowances/ purchase discounts from supplier.

A perpetual inventory system updates the inventory account each time inventory is bought

or sold – that is, perpetually.

Therefore, purchases of inventory are recorded directly into the inventory account.

In contrast, a periodic (physical) inventory system updates the inventory account only at

the end of an accounting period – that is, periodically.

Instead of recording purchases into inventory account, they are recorded in account called

Purchases, which is a temporary account that is closed into Inventory at end of the period.

This lecture will demonstrate inventory accounting under a PERPETUAL SYSTEM.

UTS 2014 – Accounting for Business Decisions A

Page 31

EXPENSING INVENTORY

Inventory becomes an expense when it is sold. The account Cost of Goods Sold or Cost of

Sales is used to capture the amount of inventory expensed during a period.

Like the recording of inventory purchases, the recording of cost of goods sold depends on a

company’s inventory system.

Under a perpetual system, COGS is updated each time inventory is sold.

Under a periodic system, COGS is calculated + recorded only at the end of the period.

REPORTING INVENTORY AND COST OF GOODS SOLD

Inventory is reported on the statement of financial position as a current asset since it is

expected to be sold within a year.

Because it is usually large, cost of goods sold is normally reported as a separate line on the

statement of comprehensive income just below sales.

Calculate the cost of goods sold using different inventory costing methods.

To determine the cost of inventory sold, companies use one of the following methods.

- Specific identification, FIFO, LIFO and moving average.

In Australia, AASB 102 does not permit the use of the third method (LIFO) – however, this

method is used in other parts of the world, primarily Japan and the US.

SPECIFIC IDENTIFICATION

The specific identification method determines cost of goods sold based on the actual cost of

each inventory item sold.

To use this method, a retailer must know which inventory item is sold + exact cost of that

particular item. So method is most likely to be used by firms whose inventory is unique.

Examples might include an antiques store or a fine jewellery store.

FIRST-IN, FIRST-OUT (FIFO)

The first-in, first-out (FIFO) method calculates cost of goods sold based on the assumption

that the first unit of inventory available for sale is the first unit sold.

That is, inventory is assumed to be sold in the order that it is purchased.

For most companies, FIFO assumption matches the actual physical flow of their inventory.

However, companies are not required to choose assumption that matches physical flow.

LAST-IN, FIRST-OUT (LIFO)

The last-in, first-out (LIFO) method calculates cost of goods sold based on the assumption

that the last unit of inventory available for sale is the first unit sold.

That is, inventory is assumed to be sold in the opposite order of its purchase.

UTS 2014 – Accounting for Business Decisions A

Page 32

MOVING AVERAGE

The moving average method calculates cost of goods sold based on the average unit cost of

all inventory available for sale.

That is, the cost of each inventory item sold is assumed to be the average cost of all

inventories available for sale at that time.

To calculate cost of goods sold at each sale date, a retailer must calculate the average unit

cost of the inventory available for sale on that date. This is conducted as follows:

EXAMPLE

Because most companies cannot track the actual cost of each inventory item that is sold,

they cannot use the specific identification method.

Instead, they must make an ASSUMPTION about the cost of inventory sold.

They can ASSUME that the cost of the inventory sold is the cost of the first unit purchased,

the last unit purchased or an average of all purchases.

Each of these three assumptions is shown below.