MAF101 Lecture 7: Finance Notes - Week 7

15 Aug 2018

School

Department

Course

Professor

Document Summary

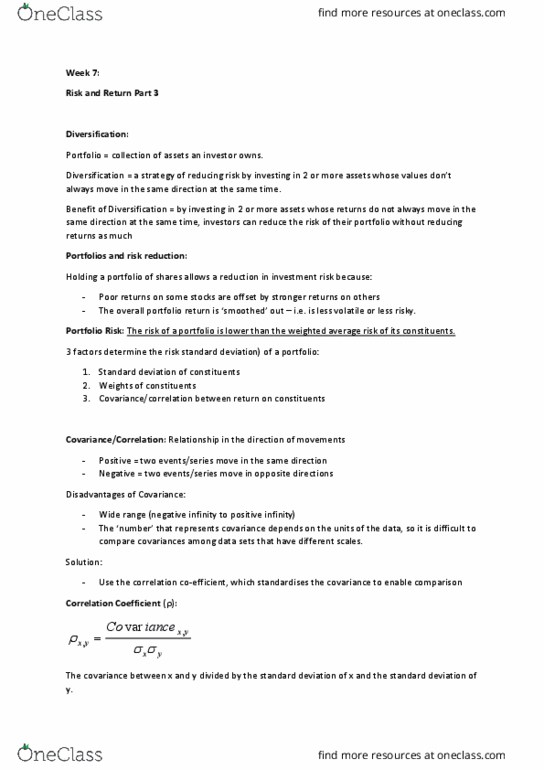

Correlation coefficient standardised ssr, yx y x r yx yx. Volitivity of a portfolio may be less than having individual investments, as the risk can decrease with more investments. Positive cov implies two investments move in same direction, negative move. Zero cov means returns on two investments are irrelevant (one most likely to be. Covariance has a wide range between - and . Spot crude oil and near-month crude oil futures contract (approximately equals to +1) >(?a)=2(bc >(?c)) bc=de[[f" &f[wu eg h_v ^__uv c4) de[[f" &f[wu eg "e"vge[ze. Portfolio risk var and sd (weight in decimals, sd in percentage) Weighted average sd cannot properly describe the risk of a portfolio and is most likely to overstate the risk. By combining investments with low or negative p, aggregate risk level can be reduced. 1 < < +1 = risk is less than weighted average.