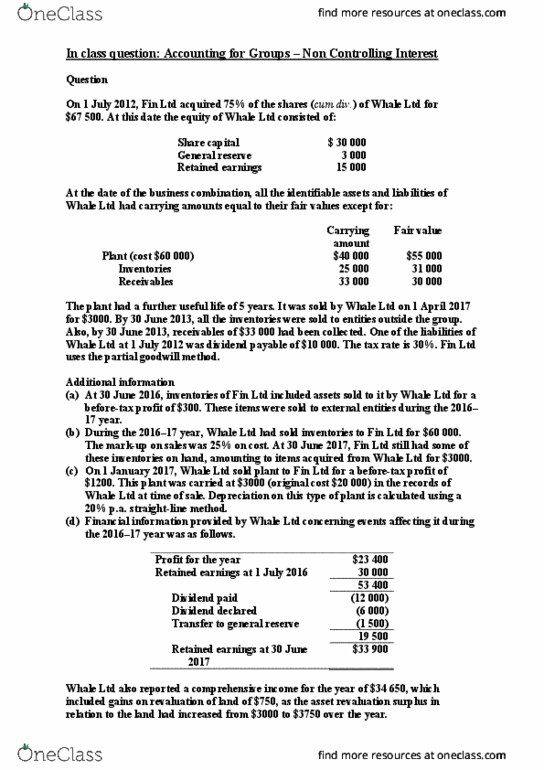

ACCT20002 Lecture Notes - Lecture 9: Net Impact, Comprehensive Income, Share Capital

5 Jun 2018

School

Department

Course

Professor

IN CLASS TUTORIAL SOLUTIONS: CONSOLIDATIONS – INTRAGROUP

Case study 28.2

Depreciation expense

At the beginning of the current period, Jessica Ltd sold a depreciable asset to its wholly owned

subsidiary, Amelie Ltd, for $80 000. Jessica Ltd had originally paid $200 000 for this asset, and at

time of sale to Amelie Ltd had charged accumulated depreciation of $150 000. This asset is used

differently in Amelie Ltd from how it was used in Jessica Ltd; thus, whereas Jessica Ltd used a 10%

p.a. straight-line depreciation method, Amelie Ltd uses a 20% straight-line depreciation method.

In calculating the depreciation expense for the consolidated group (as opposed to that recorded

by Amelie Ltd), the group accountant, Rui Xue, is unsure of which amount the depreciation rate

should be applied to ($200 000, $50 000 or $80 000) and which depreciation rate to use (10% or

20%).

Required

Provide a detailed response, explaining which depreciation rate should be used and to what

amount it should be applied.

For the group, depreciation of an asset transferred intragroup is based on the depreciation rate

applied by the entity using the asset and on the carrying amount of the asset at the moment of the

intragroup transfer.

Note that when an asset is transferred within the group, consolidation adjustments are not based on

just reversing the intragroup transaction. The purpose of the adjustments is to remove all the effects

of the intragroup transaction so that only the group’s position in relation to external entities is

reported. As the usage of the asset in the group has changed as a result of transfer within the group,

then the depreciation rate used by the group must reflect the actual consumption of benefits within

the group. This depreciation rate will then be applied to the carrying amount of the asset at the

moment of the intragroup transfer to get the depreciation expense for the asset from the group’s

perspective.

In this example, the carrying amount at the time of the intragroup transfer is $50 000 ($200 000

(original cost) - $150 000 (accumulated depreciation)). The asset is now being used by Amelie Ltd

which applies a 20% depreciation rate. Therefore, the depreciation expense from the group’s

perspective for the current period will be calculated as 20% multiplied by $50 000 (i.e. $10 000)

assuming that the asset was transferred intragroup on the first day of the current period. Given that

Amelie Ltd would have recognised a depreciation expense of 20% x $80 000 = $16 000, on

consolidation an adjustment is posted against the depreciation expense decreasing it by $6000 or 20%

of the profit on the intragroup transfer of $30 000 (i.e. $80 000 (price paid intragroup) - $50 000

(carrying amount at the moment of the intragroup sale)).

Exercise 28.14

Consolidation with differences between carrying amount and fair value at acquisition date and

intragroup transactions

Zoe Ltd purchased 100% of the shares of Matilda Ltd on 1 July 2017 for $50 000. At that date the

equity of the two entities was as follows.

At 1 July 2017, all the identifiable assets and liabilities of Matilda Ltd were recorded at fair value

except for the following.

All of the inventories were sold by December 2017. The plant and equipment had a further 5-year

useful life. Any valuation adjustments are made on consolidation.

Financial information for Zoe Ltd and Matilda Ltd for the period ended 30 June 2019 is shown

below.

Additional information

(a) Zoe Ltd records dividend receivable as revenue when dividends are declared.

(b) The beginning inventories of Matilda Ltd at 1 July 2018 included goods which cost Matilda Ltd

$2000. Matilda Ltd purchased these inventories from Zoe Ltd at cost plus 33 1/3% mark-up.

(c) Intragroup sales totalled $10 000 for the period ended 30 June 2019. Sales from Zoe Ltd to

Matilda Ltd, at cost plus 10% mark-up, amounted to $5600. The ending inventories of Zoe Ltd

included goods which cost Zoe Ltd $4400. Zoe Ltd purchased these inventories from Matilda

Ltd at cost plus 10% mark-up.

(d) On 31 December 2018, Matilda Ltd sold Zoe Ltd office furniture for $3000. This furniture

originally cost Matilda Ltd $3000 and was written down to $2500 just before the intragroup

sale. Zoe Ltd depreciates furniture at the rate of 10% p.a. on cost.

(e) The asset revaluation surplus relates to land. The following movements occurred in this

account.

(f) The income tax rate is 30%.

Required

1. Prepare the acquisition analysis at 1 July 2017.

2. Prepare the consolidation worksheet journal entries for the preparation of the consolidated

financial statements for the period ended 30 June 2019.

3. Prepare the consolidated statement of profit or loss and other comprehensive income for the

period ended 30 June 2019.

(LO3, LO4, LO5, LO6 and LO7)

Document Summary

At the beginning of the current period, jessica ltd sold a depreciable asset to its wholly owned subsidiary, amelie ltd, for 000. Jessica ltd had originally paid 000 for this asset, and at time of sale to amelie ltd had charged accumulated depreciation of 000. This asset is used differently in amelie ltd from how it was used in jessica ltd; thus, whereas jessica ltd used a 10% p. a. straight-line depreciation method, amelie ltd uses a 20% straight-line depreciation method. Provide a detailed response, explaining which depreciation rate should be used and to what amount it should be applied. For the group, depreciation of an asset transferred intragroup is based on the depreciation rate applied by the entity using the asset and on the carrying amount of the asset at the moment of the intragroup transfer. Note that when an asset is transferred within the group, consolidation adjustments are not based on just reversing the intragroup transaction.