BLAW30002 Lecture Notes - Lecture 9: Ordinary Income, Kims, Tertiary Education Fees In Australia

15 Nov 2018

School

Department

Course

Professor

Document Summary

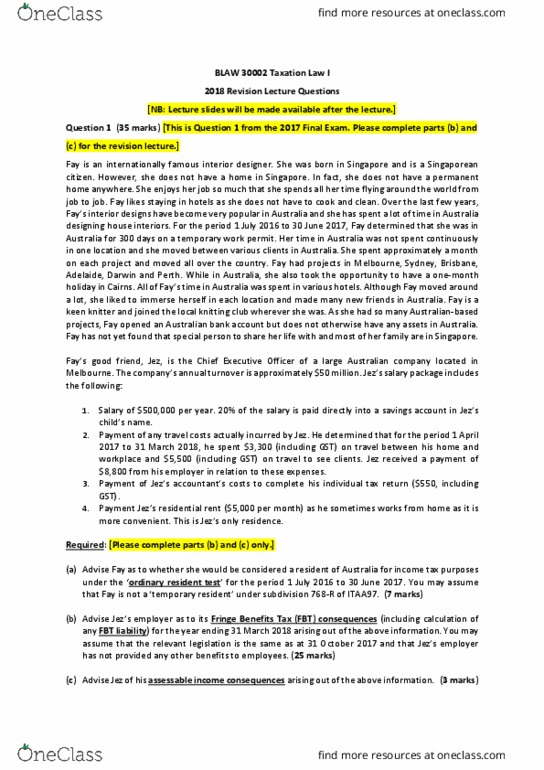

Ki(cid:373) ru(cid:374)s a garde(cid:374)i(cid:374)g (cid:271)usi(cid:374)ess pro(cid:448)idi(cid:374)g garde(cid:374) (cid:373)akeo(cid:448)er ser(cid:448)i(cid:272)es to i(cid:374)(cid:374)er (cid:272)it(cid:455) reside(cid:374)(cid:272)es. Her annual income from the business is approximately ,000. The (cid:373)eals (cid:449)ere all di(cid:374)e i(cid:374) at a large local restaurant which has annual revenue of more than m. (a) advise bob as to his income tax consequences arising from the above information. Income and deductions, i. e. received and spent. Do(cid:374)"t (cid:374)eed to talk a(cid:271)out fri(cid:374)ge (cid:271)e(cid:374)efits, just ordi(cid:374)ar(cid:455) i(cid:374)(cid:272)o(cid:373)e a(cid:374)d the(cid:374) ha(cid:455)es (cid:272)ase. Similar to the case of lunney(1958), bob"s home to work travel is a private expense and thus is not deductible. It will only be deductible in the case where he is transporting bulky items in which is a deduction is allowed in cases vogt (1975) and brandon (cs12. 27) Following the principles in ballesty (1997), as an alternative workplace, bob is entitled to a deduction. (b) advise kim as to her income tax consequences arising from the above information.