ECON20003 Lecture Notes - Lecture 15: Probit, Homoscedasticity, Sampling Error

27 Jul 2018

School

Department

Course

Professor

Document Summary

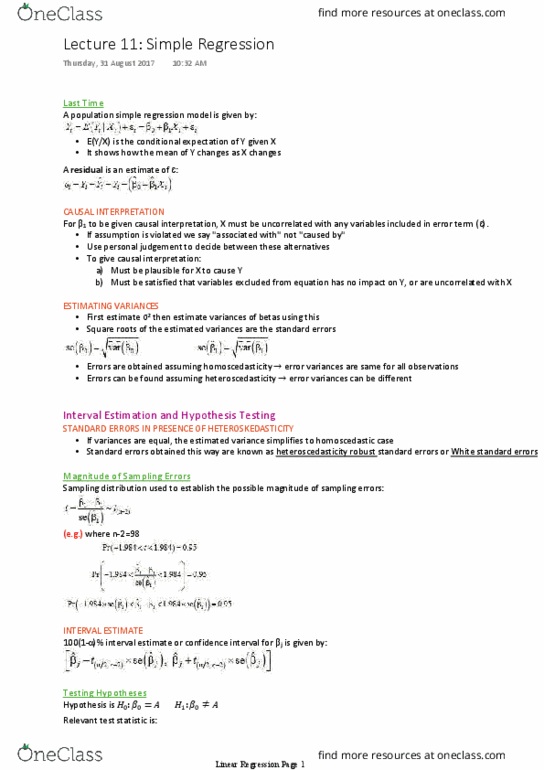

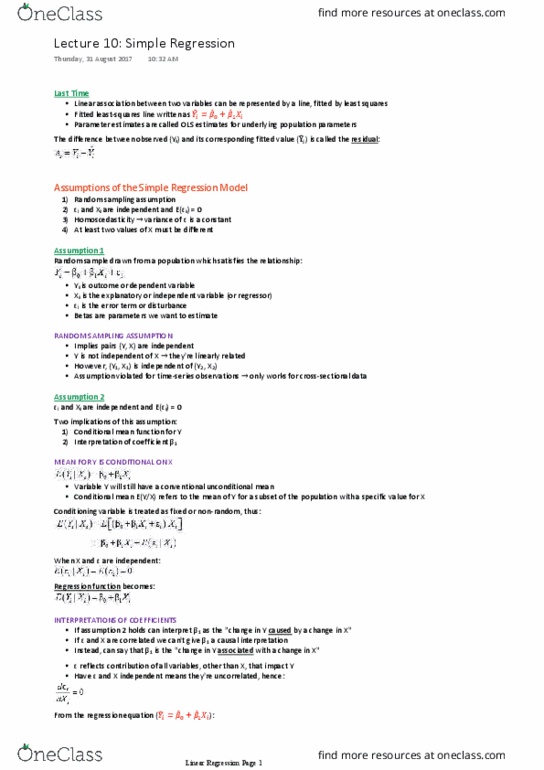

Prediction in a linear model: predict by substituting given values in equation, use prediction interval to check how reliable the prediction is. When predicting y for a given value of x0: Use sample estimates of s to get 0. Su(cid:271)t(cid:396)a(cid:272)t the a(cid:271)o(cid:448)e e(cid:395)uatio(cid:374)s a(cid:272)tual (cid:448)alue - predicted value: error has two sources: Sampling error of betas: error term ( 0) The variance of the prediction error is given by: assume the error term ( ) isn"t correlated with betas, assumption holds if we have random cross-section and we"re predicting out-of-sample Assuming homoscedasticity with var( )= 2, the standard error of the prediction error is: Ignoring coefficient uncertainty underestimates the standard error but only by small amount: 2 typically much larger than (cid:1870) (0 0) Note: for a model to be useful it has to have a higher r2 if (cid:374)ot, p(cid:396)edi(cid:272)tio(cid:374) i(cid:374)te(cid:396)(cid:448)al (cid:449)ill (cid:271)e too la(cid:396)ge.