ECON10004 Lecture Notes - Lecture 3: Demand Curve, Time Horizon, Complementary Good

Microeconomics Week 3

CHAPTER 5: ELASTICITY AND ITS APPLICATION

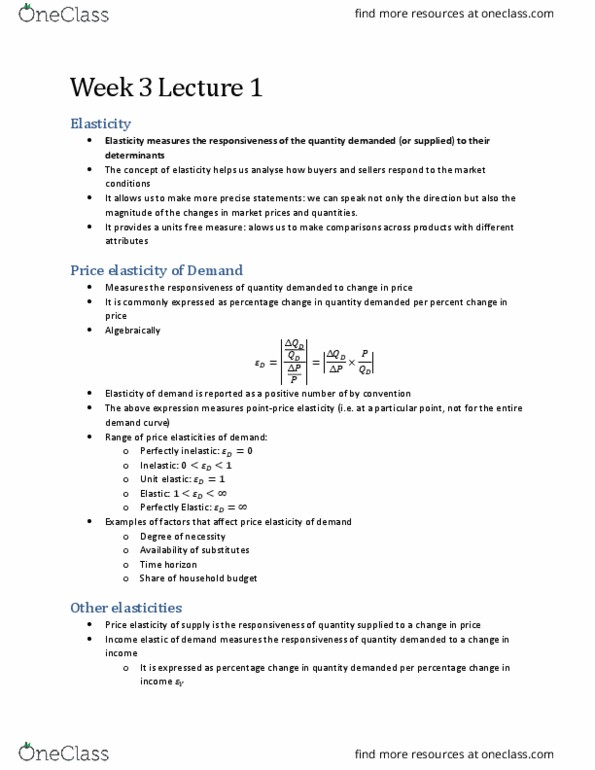

Elasticity: a measure of the responsiveness of quantity demanded or quantity supplied to

one of its determinants

Price Elasticity of Demand: a measure of how much the quantity demanded of a good

responds to a change in the price of that good, calculated as the percentage change in

quantity demanded divided by the percentage change in price

• Demand for a good said to be elastic if quantity demanded responds substantially to

price changes

• Inelastic is quantity demanded responds only slightly to changes in price

Availability of Close Substitutes

• Goods with close substitutes tend to have more elastic demand because it is easier

for consumers to switch

Necessities versus Luxuries

• Necessities tend to have inelastic demands

• Luxuries tend to have elastic demands

• Whether good is necessity or luxury depends on preferences of buyer, not intrinsic

properties of goods

Definition of the Market

• Narrowly defined markets tend to be have more elastic demand than broadly

defined markets since its easier to find close substitutes for narrowly defined goods

Time Horizon

• Goods tend to have more elastic demand over longer time horizons

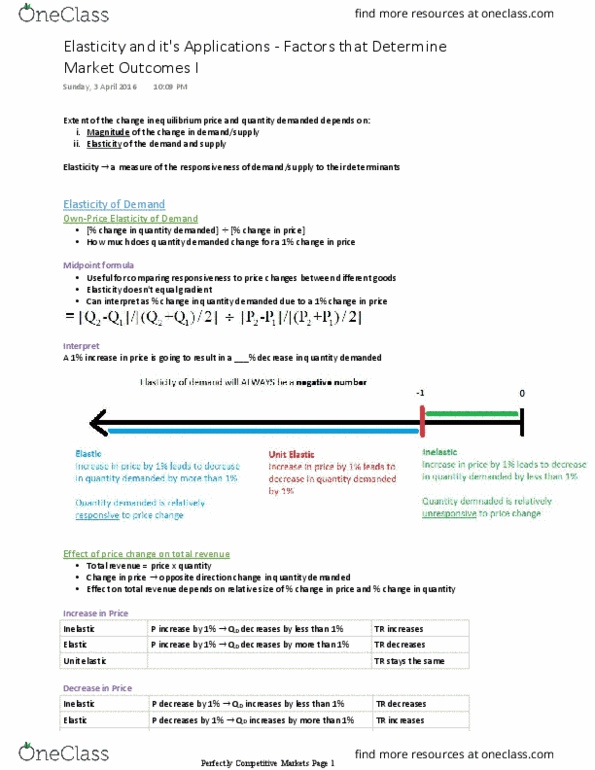

COMPUTING THE PRICE ELASTICITY OF DEMAND

Price elasticity of demand = % change in quantity demanded / % change in price

• Percentage change in quantity will always have opposite sign to percentage change

in price as quantity demanded of good is negatively related to its price

THE VARIETY OF DEMAND CURVES

• Demand elastic when elasticity greater than 1, so that quantity moves

proportionately more than price

• Inelastic when less then 1, quantity moves proportionally less than price

• If elasticity is 1, percentage change in quantity equals percentage change in price;

demand is said to have unit elasticity

• The flatter the demand curve that passes through given point, the greater the price

elasticity of demand

• The steeper the demand curve, the smaller the price elasticity of demand

• Zero elasticity = perfectly inelastic = vertical, perfectly elastic = horizontal

find more resources at oneclass.com

find more resources at oneclass.com

TOTAL REVENUE AND THE PRICE ELASTICITY OF DEMAND

Total Revenue (in a market): the amount paid by buyers and received by sellers of a good,

calculated as the price of the good times quantity sold

General Rules:

• When a demand curve is inelastic (a price elasticity less than 1), a price increase

raises total revenue and a price decrease reduces total revenue.

• When a demand curve is elastic (a price elasticity greater than 1), a price increase

reduces total revenue and a price decrease raises total revenue.

• In the special case of unit elastic demand (a price elasticity exactly equal to 1), a

change in the price does not affect total revenue.

find more resources at oneclass.com

find more resources at oneclass.com

OTHER DEMAND ELASTICITIES

Income Elasticity of Demand: a measure of how much the quantity demanded of a good

respods to a hage i osuers’ ioe, alulated as the peretage hage i

quantity demanded divided by the percentage change in income

Income elasticity of demand = % change in quantity demanded / % change in income

Cross-Price Elasticity of Demand: a measure of how much the quantity demanded of one

good responds to a change in the price of another good, computed as the percentage

change in quantity demanded of the first good divided by the percentage change in the

price of the second good

Cross-Price Elasticity of Demand = % change in quantity of good 1 / % change in price of

good 2

THE ELASTICITY OF SUPPLY

Price Elasticity of Supply: a measure of how much the quantity supplied of a good responds

to a change in the price of that good, calculated as the percentage change in quantity

supplied divided by the percentage change in price

• Supply of good is elastic if quantity supplied responds substantially to changes in

price

• Inelastic if quantity responds only slightly to changes in price

• Price elasticity of supply depends on flexibility of sellers to change the amount of

good they produce

• In most markets, key determinant of price is time period being considered; supply

usually more elastic in long run than short run

COMPUTING THE PRICE ELASTICITY OF SUPPLY

Price elasticity of supply = % change in quantity supplied/ % change in price

THE VARIETY OF SUPPLY CURVES

• Zero elasticity = supply is perfectly inelastic = vertical

• Perfectly elastic = horizontal

• In some markets, the elasticity of supply is not constant but varies over supply curve

• As quantity supplied rises, firms begin to reach capacity, once capacity reached,

increasing production requires more expenses so supply becomes less elastic

• Because firms often have a maximum capacity for production, the elasticity of supply

may be high at low levels to quantity supplied and low at high levels of quantity

supplied

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Elasticity: a measure of the responsiveness of quantity demanded or quantity supplied to one of its determinants. Inelastic is quantity demanded responds only slightly to changes in price. Availability of close substitutes: goods with close substitutes tend to have more elastic demand because it is easier for consumers to switch. Necessities versus luxuries: necessities tend to have inelastic demands, luxuries tend to have elastic demands, whether good is necessity or luxury depends on preferences of buyer, not intrinsic properties of goods. Definition of the market: narrowly defined markets tend to be have more elastic demand than broadly defined markets since its easier to find close substitutes for narrowly defined goods. Time horizon: goods tend to have more elastic demand over longer time horizons. The variety of demand curves: demand elastic when elasticity greater than 1, so that quantity moves proportionately more than price. Inelastic when less then 1, quantity moves proportionally less than price.