ACC1200 Lecture Notes - Lecture 11: Financial Analysis, Trend Analysis, Financial Statement

22 May 2018

School

Department

Course

Professor

Week 11: Analysis and Interpretation

Analysis and interpretation of financial statement: To provide useful information to assist users to

make informed decisions relevant to their circumstances.

• Whether to grant loans

• Supplying on credit

Fundamentals analysis

• Refers to analyzing many aspect of an entity to assess the entity, including reviewing the state

of the industry in which the entity operates in, as well as the entity's financial statements, its

management and governance, and its competitive positioning.

• While fundamental analysis is conducted on historical data and current information, the

purpose of the analysis is to make predictions about the entity's future.

Ratios

• When interpreting a ratio, it is important to understand what the ratio is measuring and

compare it to an appropriate benchmark

• An entity's accounting policy choices and management estimations affect the reporting

numbers and this should be taken into consideration when comparing the ratios

Financial Analysis

• One aspect of this fundamental analysis is financial analysis.

• An analytical method in which reported financial numbers are used to form opinions as to the

entity's past and future performance and positions

o Financial analysis adds further meaning to the reported numbers, allowing users to

make a better assessment of an entity's profitability, efficiency, liquidity, capital

structure and market performance.

• There are limitations associated with financial analysis.

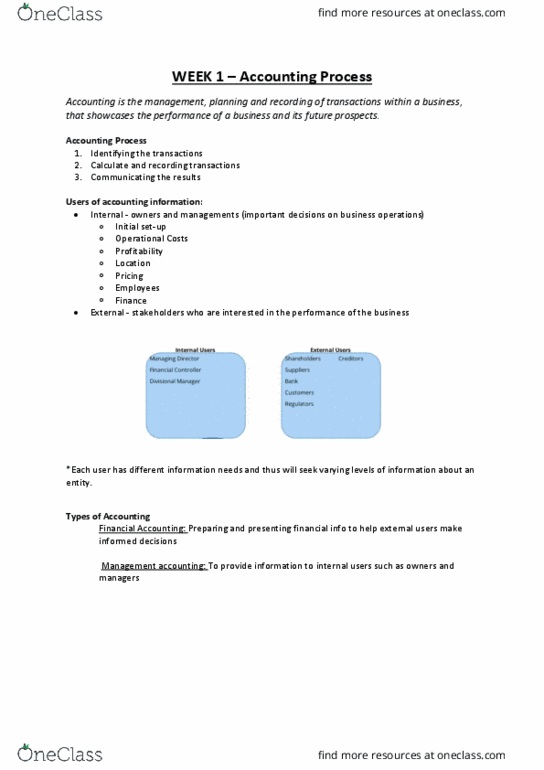

Users and decision making

• User groups are interested in different aspects of the entity and various sources are available

to interested parties to facilitate their decision making

o Resource providers (creditors, shareholders, employees)

o Recipients of goods and services ( customers and debtors)

o Parties performing an overview or regulatory function (taxation, corporate regulators)

Types of methods

• Horizontal analysis: compares the reported numbers in the current period with the equivalent

numbers for the previous period, usually the immediate preceding period.

o Permits the users to readily calculate the absolute dollar change and the percentage

change in the reported numbers between the periods, highlights the magnitude and the

significance of the dollar changes

find more resources at oneclass.com

find more resources at oneclass.com

• Trend analysis: predict the future direction of the various items on the basis of the direction of

the item in the past. To calculate a trend, at least 3 years of data are required.

o Useful in identifying the significance of an item relative to its base value

o Useful in formulating predictions as to the future prospects of the entity

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Analysis and interpretation of financial statement: to provide useful information to assist users to make informed decisions relevant to their circumstances: whether to grant loans. Identifies the importance of an item relative to the anchor item: ratio analysis: comparisons of one item in a financial statement relative to another item in the financial statement. This per(cid:373)its users to assess the stability and/or directional changes in the ratios over time. Unfavourable trends should be investigated by financial statement users: a (cid:272)o(cid:373)pariso(cid:374) of the e(cid:374)tit(cid:455)"s ratios (cid:449)ith those of other e(cid:374)tities operati(cid:374)g i(cid:374) the sa(cid:373)e industry, referred to as intra-industry analysis. For example, a potential investor who wishes to invest in banking shares has identified four entities operating in that economic industry sector. The investor can use ratios to compare their respective returns and risks: a (cid:272)o(cid:373)pariso(cid:374) of the e(cid:374)tit(cid:455)"s ratios (cid:449)ith the i(cid:374)dustr(cid:455) a(cid:448)erages.