AYB200 Lecture 11: Lecture 11

Lecture 11: Income & Expenses

Income, Expenses and Matching

AASB Framework (para 70a) defines income as: ieases i eooi eefits duig the

accounting period in the form of inflows or enhancements of assets or decreases in liabilities that

result i a iease i euit, othe tha those elatig to otiutios fo euit pates

2 Categories of Income

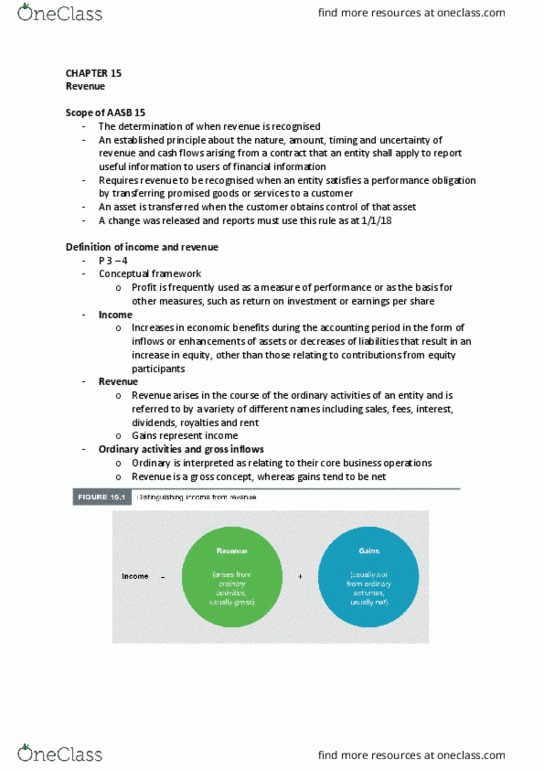

- Revenue (AASB Framework para 74):

o aises i the ouse of odia atiities of a etit ad is efeed to a aiet

of different names iludig sales, fees, iteest, diideds, oalties ad et.

- Gains represent (AASB Framework paras 75 & 76):

o othe ites that eet the defiitio of ioe ad a, o a ot, aise i the

ouse of the odia atiities of a etit e.g. disposal of non-current assets,

unrealised gains)

Income – revenue or income?

- INCOME – REVENUE OR GAINS?

• Professional judgment involved in differentiating

What is a odia atiit fo oe usiess a ot e odia fo aothe—so the benefits

might be deeed eeue i oe etit ad a gai i aothe

• Gains represent increases in economic benefits and as such are not different in nature

from revenue.

• Gains are usually displayed separately in income statement when recognised

Knowledge of them is useful in making economic decisions

• Gains are often reported net of related expenses.

• Classification as revenue or gain does not affect reported profit

- Income Recognition

• Recognition of income: AASB Framework paras 92 – 93

• Recognised in income statement when:

a iease i futue eooi eefits elated to a iease i a asset o a deease

of a liailit has aise that a e easued elial (i.e. occurs simultaneously with

recognition of increases in assets or decreases in liabilities)

• Procedures for recognising income:

Revenue should be EARNED

‘estit eogitio to those ites that a e easued elial ad hae a

suffiiet degee of etait

Accounting for Income

- DR Asset (increase e.g. cash, accounts receivable) or Liability (decrease)

- CR Income (revenue)

find more resources at oneclass.com

find more resources at oneclass.com

Expenses

- Expense is a PERFORMANCE measure

- AASB Framework (para 70 (b)) defines expenses as:

deeases i eooi eefits duig the aoutig peiod i the fo of

outflows or depletions of assets or incurrence of liabilities that result in decreases in

euit, othe tha those elatig to distiutios to euit patiipats

- Iludes losses, as ell as those epeses that aise i the ouse of the odia

atiities of the etit AA“B Faeok paa

- Expenses from course of ordinary activities:

e.g. ost of sales, ages, depeiatio outflo o depletio of assets suh as ash,

ash euialets, ieto, popet, plat ad euipet AA“B Faeok paa

78)

Expenses and Losses

- Losses: othe ites that eet defiitio of epeses.

- May (or may not) arise in course of ordinary activities

- They are a decrease in economic benefits

- Examples of losses: Disasters (fire, floods etc.), disposal of non-current assets.

- May be unrealised (e.g. effect of changes in foreign exchange rates)

- Often reported net of related income

- Displayed separately if useful knowledge for decision making

Expense Recognition

- Recognition of expenses (AASB Framework paras 94 – 98):

he a deease i futue eooi eefits elated to a deease i a asset o a

iease of a liailit has aise that a e easued elial

- Occurs simultaneously with recognition of increase in liabilities or decrease in assets

- Recognised in direct association with earning of income (matching of costs with

revenues)

- If expenses spread over more than one period, recognise them systematically over time

Accounting for Expenses

- DR Expense

- CR Asset (decrease) or liability (increase)

Matching Income and Expenses

find more resources at oneclass.com

find more resources at oneclass.com

Journal Entries

Financial Statements

Othe opehesie ioe

- AASB 101 Para 7

o othe opehesie ioe opises ites of ioe ad epese that ae

ot eogized i pofit o loss as euied othe AA“

- Additional and material items: up to the company -> can provide as many lines as they

want

The need for change

- Why change the standard?

o Remove inconsistencies and weaknesses in existing revenue requirements

(between standards and the Conceptual Framework)

o Provide a more robust framework

o Improve comparability of revenue recognition practices

o Provide more useful information to users

o Simplify preparation of financial statements

- What does it mean for business? (Implications)

o There will be more judgement for disclosure

o Compensation and bonus plans – changes in timing of revenue recognition may

affect these

o Contracts. Existing terms could take on a new meaning

o Technology. Businesses may have to update current software to capture new

information

o Tax implications: timing of cash payments may be affected, e.g. if recognizing

revenue sooner than in the past

o Investor relations: stakeholders will want to know how the new standard will

hage the opas fiaial pitue

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Revenue (aasb framework para 74): (cid:862)a(cid:396)ises i(cid:374) the (cid:272)ou(cid:396)se of o(cid:396)di(cid:374)a(cid:396)(cid:455) a(cid:272)ti(cid:448)ities of a(cid:374) e(cid:374)tit(cid:455) a(cid:374)d is (cid:396)efe(cid:396)(cid:396)ed to (cid:271)(cid:455) a (cid:448)a(cid:396)iet(cid:455) of different names i(cid:374)(cid:272)ludi(cid:374)g sales, fees, i(cid:374)te(cid:396)est, di(cid:448)ide(cid:374)ds, (cid:396)o(cid:455)alties a(cid:374)d (cid:396)e(cid:374)t(cid:863). Income revenue or gains: professional judgment involved in differentiating. Knowledge of them is useful in making economic decisions: gains are often reported net of related expenses, classification as revenue or gain does not affect reported profit. Est(cid:396)i(cid:272)t (cid:396)e(cid:272)og(cid:374)itio(cid:374) to (cid:862)those ite(cid:373)s that (cid:272)a(cid:374) (cid:271)e (cid:373)easu(cid:396)ed (cid:396)elia(cid:271)l(cid:455) a(cid:374)d ha(cid:448)e a suffi(cid:272)ie(cid:374)t deg(cid:396)ee of (cid:272)e(cid:396)tai(cid:374)t(cid:455)(cid:863) Dr asset (increase e. g. cash, accounts receivable) or liability (decrease) I(cid:374)(cid:272)ludes (cid:862)losses(cid:863), as (cid:449)ell as (cid:862)those e(cid:454)pe(cid:374)ses that a(cid:396)ise i(cid:374) the (cid:272)ou(cid:396)se of the o(cid:396)di(cid:374)a(cid:396)(cid:455) a(cid:272)ti(cid:448)ities of the e(cid:374)tit(cid:455)(cid:863) (cid:894)aa b f(cid:396)a(cid:373)e(cid:449)o(cid:396)k pa(cid:396)a (cid:1011)(cid:1012)(cid:895) Expenses from course of ordinary activities: (cid:862)e. g. (cid:272)ost of sales, (cid:449)ages, dep(cid:396)e(cid:272)iatio(cid:374) (cid:894)outflo(cid:449) o(cid:396) depletio(cid:374) of assets su(cid:272)h as (cid:272)ash, (cid:272)ash e(cid:395)ui(cid:448)ale(cid:374)ts, i(cid:374)(cid:448)e(cid:374)to(cid:396)(cid:455), p(cid:396)ope(cid:396)t(cid:455), pla(cid:374)t a(cid:374)d e(cid:395)uip(cid:373)e(cid:374)t(cid:863) (cid:894)aa b f(cid:396)a(cid:373)e(cid:449)o(cid:396)k pa(cid:396)a. Losses: (cid:862)othe(cid:396) ite(cid:373)s(cid:863) that (cid:373)eet defi(cid:374)itio(cid:374) of e(cid:454)pe(cid:374)ses.