AYB225 Lecture Notes - Lecture 5: Evaluation Strategy, Standard Cost Accounting, Cost Driver

Document Summary

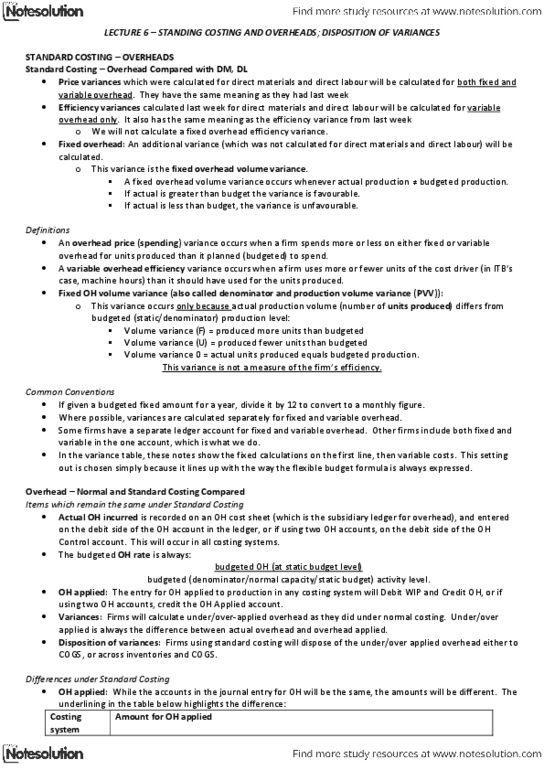

Lecture 5 standard costing; direct material and labour variances. Flexing the budget from the static budget is the starting point for all variance calculation, and variance calculation is an integral part of standard costing. Firms commonly prepare a variance report analysing the difference between: budgeted costs at budgeted activity level (static budget) far right column, and, actual costs (far left column) The report shows two levels of variances. First, the static budget variance, which is the difference between budgeted costs at budgeted activity level, and actual costs. The difference between the static budget and the actual cost is favourable (,050 f), suggesting that costs were less than expected: that is very misleading. If you analyse that variance further, it is evident that the favourable variance is attributable to the fact that the firm produced 10,000 fewer units than it expected to produce. In fact, for that level of production all costs except dm were higher than expected (unfavourable).