BSB110 Lecture Notes - Lecture 5: Accounting Software, Accounting Equation, Financial Statement

Week 4 Accounting Lecture Notes

The Recording Process

Accounting Procedures

• How do accountants record information to produce financial statements?

o This lecture will explain the processes which all businesses use.

o Remember, this topic is a critical foundation for learning accounting so it is

vital that you practise with practice questions.

o Many businesses use accounting software such as MYOB or Reckon but it is

vital that students understand the manual accounting processes to be able

to use software correctly and to correct errors

Analysing Transactions

• Pays $600 for insurance in cash for a 1 year insurance policy:

The Journal

• A journal is a chronological record of all transactions.

• Discloses the complete effect of a transaction.

• This helps prevent errors as debit and credit amounts are easily compared.

Debit (Dr) and Credit (Cr) Rules

• Based on the Accounting Equation.

• Assets have a debit nature (i.e. assets have a debit balance).

• Because of the accounting equation, Liabilities and Equity are on the opposite side to

assets.

• Liabilities and Equity accounts have credit natures (i.e. liabilities and Equity have

credit balances)

find more resources at oneclass.com

find more resources at oneclass.com

• Because Revenues increase Equity, they have a credit nature (i.e. revenues have

credit balances)

• Because Expenses decrease Equity, they have a debit nature (i.e. expenses have

debit balances)

• Assets have a debit nature or debit balances

• Liabilities have a credit nature or credit balances

• Equity has a credit nature or credit balances

• Revenues have a credit nature or credit balances

• Expenses have a debit nature or debit balances

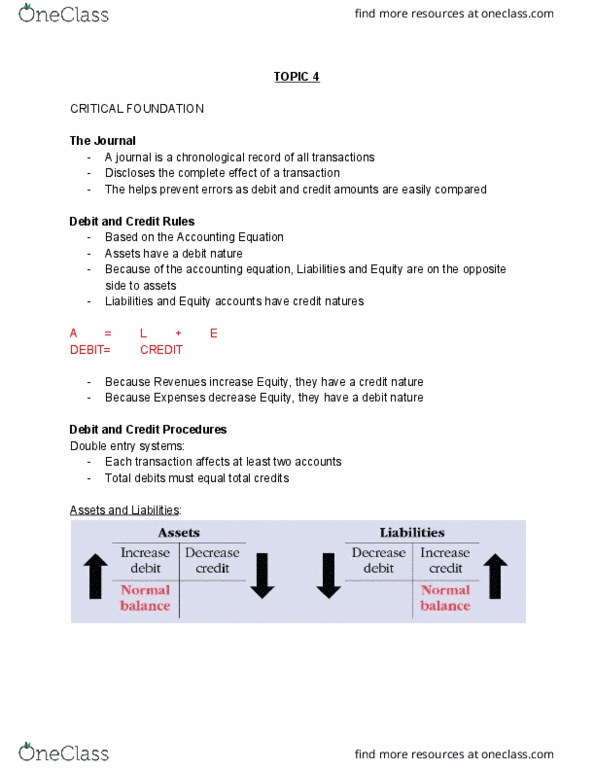

Debit and Credit Procedures

• Double entry system:

o Each transaction affects at least two accounts

o Total debits must equal total credits

• Debit and Credit procedures for Assets and Liabilities:

find more resources at oneclass.com

find more resources at oneclass.com

• Debit and Credit procedures for Equity:

o Share Capital:

o Retained Earnings:

o Dividends:

• Debit and Credit procedures for Revenue and Expenses:

Enter Transactions into the Journal

• When entering transactions into the Journal:

o Think about the analysis you did previously, as this will tell you which

accounts are affected and for how much.

o You now also need to think for each of the accounts affected, does the

account need to be debited or credited.

• Remember: total Debits = total Credits

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Analysing transactions: pays for insurance in cash for a 1 year insurance policy: The journal: a journal is a chronological record of all transactions, discloses the complete effect of a transaction, this helps prevent errors as debit and credit amounts are easily compared. The recording process- posting information to the ledger. The general ledger: contains all asset, liability and equity, revenue and expense accounts. The account in the ledger: an account is an individual accounting record of increases and decreases in a specific asset, liability or equity item. Debits and credits in the ledger: debit, refers to the left side of the account, commonly abbreviated as dr, credit, refers to the right side of the account, commonly abbreviated as cr. The trial balance: a trial balance is a list of all the accounts and their balances at a given time listed in order as they appear in general ledger.