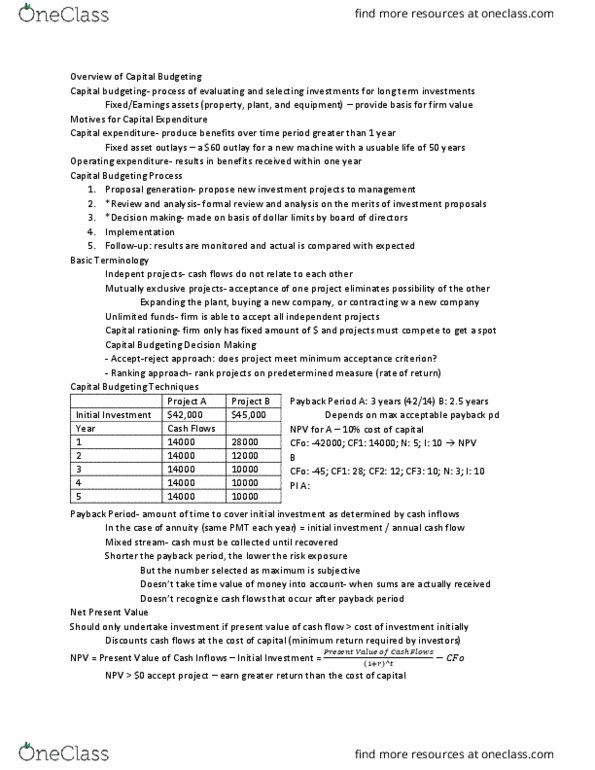

EFB210 Lecture Notes - Lecture 5: Payback Period, Cash Flow, Net Present Value

Week 5 Finance 1 Lecture Notes

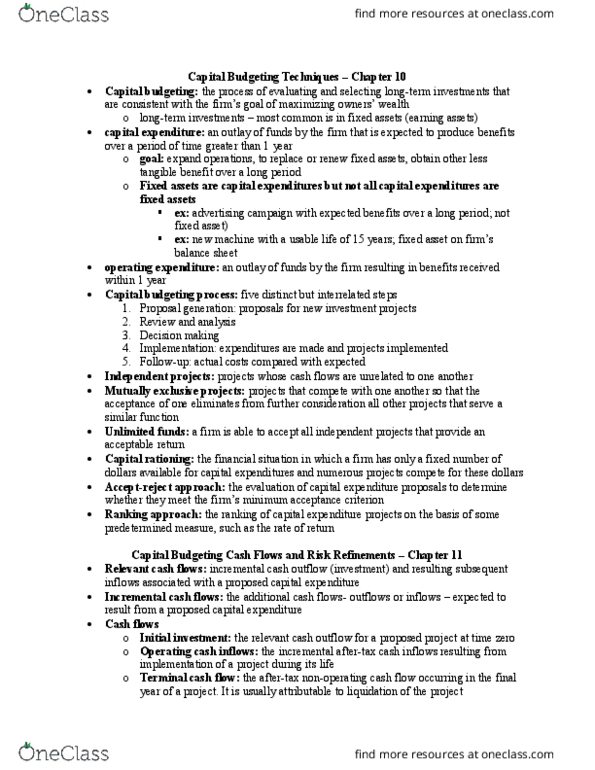

Capital Budgeting 1

Capital Budgeting Overview

• Investment project:

o … interpreted very broadly to include any proposal to outlay cash in

the expectation that future cash flows will result. Peirson et al. (2015)

p.104.

• Note that projects can be classified as

o Independent

▪ Investment in one does not prohibit investment in another.

o Mutually Exclusive

▪ Investment in one prohibits (financial or physical constraint) the

investment in another.

o Mutually Inclusive

▪ Investment in one requires investment in the other

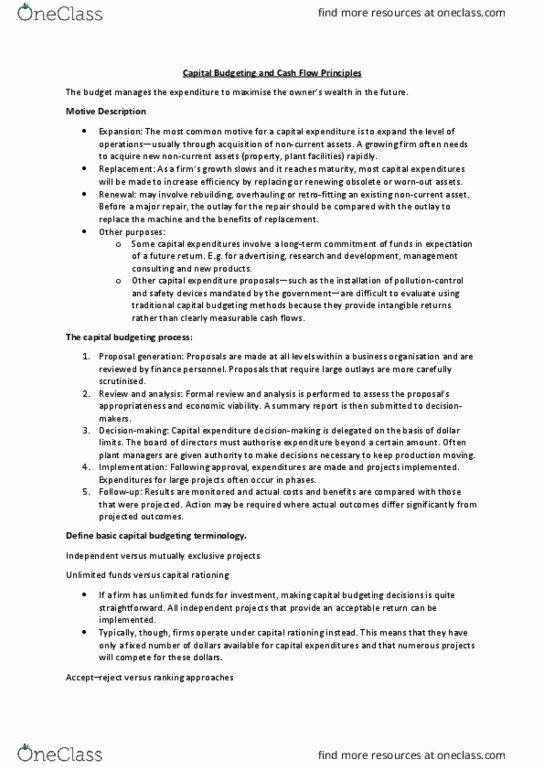

• Capital expenditure Process

1. Generation of investment proposals

2. Evaluation and selection (forward)

3. Approval and control of capital expenditure

4. Post-completion audit (forward & backward)

Evaluation Methods

• Percentage of Australian CFOs who responded use a particular evaluation metric

Payback period:

• The length of time it takes to recover our initial investment.

• Decision Rule:

o Accept project if Payback < Target Payback Otherwise Reject

o Target is set arbitrarily (usually 2 - 5 years).

• Example 1

Method Percentage

(approx)*

Discounted Cash

Flow Method#

Internal Rate of Return (IRR) 72 Yes

Net Present Value (NPV) 70 Yes

Payback Period (PB) 57 No

Real Option Analysis 27 Yes

Accounting Rate of Return (ARR) 26 No

Project

Yr 0 Yr 1 Yr 2 Yr 3 Yr 4 PB

A

-9,000

3,000 3,000 3,000 3

B

-9,000

7,000 1,000 1,000 3

C

-9,000

3,000 3,000 3,000 9,000 3

D

-9,000

3,000 3,000 3,000 3

find more resources at oneclass.com

find more resources at oneclass.com

• Problems

o Does not account for Size, Timing and Risk of Cash Flows

o Selected projects are not necessarily profitable in the economic sense –

positive NPV

• Advantages

o Simple and asks a really important question

o Can be used in conjunction with other measures

o Places greater importance on early cash flows that can be considered less

uncertain than later cash flows

ARR:

• Accounting Rate of Return

o Uses accounting profits as a ratio of investment to measure the return on

investment. Common Definitions:

▪ ARRnet = Avg Acc Profit/ Average Investment

▪ ARRgross = Avg Acc Profit/ Initial Investment

• Decision rule:

o Accept project if ARR > Target ARR otherwise Reject

• Problems

o Does not use cash flows and ignores timing

o Target is set arbitrarily

• Advantages

o Can be used in conjunction with other measures

• Example 2: A firm proposes to install a labour-saving machine (cost $15,000) that will

save some cash operating expenses each year. Life of five years, no salvage value

and no tax.

o Payback

o ARR Gross

Year Outlay Saving

0

-

15,000

1 3,800

2 4,200

3 5,000

4 8,000

5 9,000

Year Outlay

Saving

Depr.*Profit

0 -15,000

1 3,800 -3,000 800

2 4,200 -3,000 1,200

3 5,000 -3,000 2,000

4 8,000 -3,000 5,000

5 9,000 -3,000 6,000

Average

3,000

find more resources at oneclass.com

find more resources at oneclass.com

• Discounted Cash Flow (DCF) Methods

o Net Present Value (NPV)

o Internal Rate of Return (IRR)

o Benefit-Cost Ratio (BCR)

o Annual Equivalents (AE)

• All account for cash flows, timing and risk

• They are all linked to NPV

o IRR corresponds to NPV = 0

o BCR indicates value created per dollar invested

o AE is NPV annuitised (if thats a word, turned in to an annuity…)

• Assume - timing of cash flows known and cash flows (except initial outlay) occur at

end of year

NPV:

• NPV represents the increase in value of the firm which accrues from a project

o To be consistent with the objective of the firm, the firm should

▪ Accept all +NPV projects

▪ Reject all -NPV projects

Example 3: NPV

IRR

• IRR is that rate of return which produces a zero NPV

• Found by trial and error

• IRR rule is accept project if IRR > r otherwise reject

• Project may not necessarily have one IRR. It may have no IRR (e.g. all negative cash

flows) or multiple IRRs (e.g. if the project has more than one negative Cash Flow)

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Investment project: (cid:1688) interpreted very broadly to include any proposal to outlay cash in the expectation that future cash flows will result. (cid:1689) peirson et al. (2015) p. 104, note that projects can be classified as. Investment in one does not prohibit investment in another: mutually exclusive. Investment in one prohibits (financial or physical constraint) the investment in another: mutually inclusive. Investment in one requires investment in the other: capital expenditure process, generation of investment proposals, evaluation and selection (forward, approval and control of capital expenditure, post-completion audit (forward & backward) Internal rate of return (irr: percentage of australian cfos who responded use a particular evaluation metric. Payback period: the length of time it takes to recover our initial investment, decision rule, accept project if payback < target payback otherwise reject, target is set arbitrarily (usually 2 - 5 years), example 1. Arr: accounting rate of return, uses accounting profits as a ratio of investment to measure the return on investment.