JSB171 Lecture Notes - Lecture 1: Tariffs In United States History, State Income Tax, Canadian Airlines

Document Summary

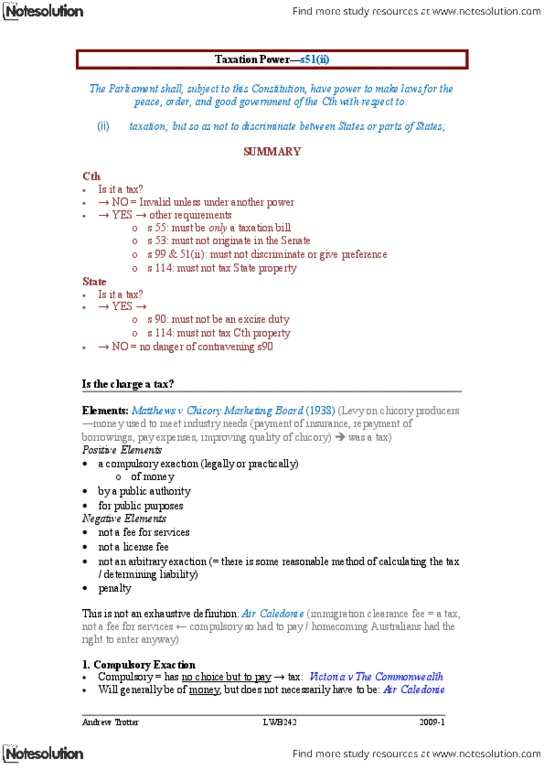

The parliament shall, subject to this constitution, have power to make laws for the peace, order, and good government of the cth with respect to: (ii) taxation; but so as not to discriminate between states or parts of states; Is it a tax: yes , s 90: must not be an excise duty, s 114: must not tax cth property, no = no danger of contravening s90. Elements: matthews v chicory marketing board (1938) (levy on chicory producers. Money used to meet industry needs (payment of insurance, repayment of borrowings, pay expenses, improving quality of chicory) was a tax) Positive elements a compulsory exaction (legally or practically: of money by a public authority for public purposes. Negative elements not a fee for services not a license fee not an arbitrary exaction (= there is some reasonable method of calculating the tax. Practical compulsion to pay tax imposed on another will suffice: maccormick v.