FINS1612 Lecture Notes - Lecture 4: Financial Asset, Financial Instrument, Financial Transaction

FINS1612

Lecture 1

- Quiz 1: 20% (w4)

- Quiz 2: 30%

- Finance: art and science of managing scare resources of money

- Money: acts as a medium of exchange, represents a store of wealth, facilitates saving, solves

divisibility problem

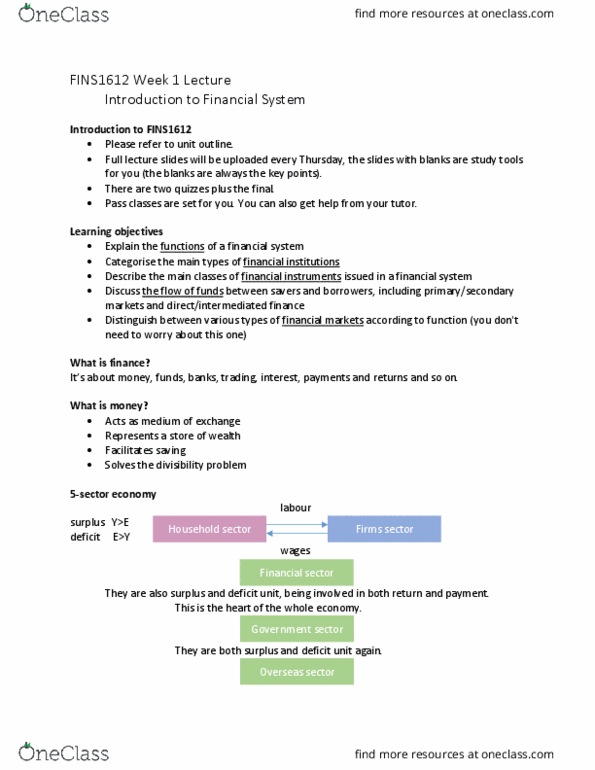

- Household (surplus suppliers of funds Y>E and deficit demanders of funds E>Y), firms

(investment surplus, deficit), financial (surplus from household → interest income, deficit →

loans and interest payment AND firms AND banks are also deficit units borrow w/ one

another), gov (local or o/s financial sector), o/s

- Fiscal+ monetary policy on savings/investm decisions

Functions of a financial system

- Financial institutions, instruments, markets which interact to facilitate the flow of funds

between deficit and surplus units within the economy

- Financial institutions permit the flow of funds between borrowers and lenders by facilitating

financial transaction

o Provide investment products (surplus units)

o Provide alternative funding sources (deficit)

o Provide risk management products (insurance)

- Facilitate the flow of funds- primary financial market (creation of new financial assets) +

secondary market (provide arrangement for transfer of funds by arranging trades in existing

financial assets)

- Efficient financial system should ensure that savings will be directed to the most EFFICIENT

users (vs needy) of those funds

- Central bank + prudential supervisor

Financial Institutions

Istitutios’ sources and uses classification

- Depository financial institutions (DFIs)

- Investment banks and merchant banks

- Contractual savings institutions (CSI)

- Finance companies

- Unit trust

Financial Instruments

- Financial asset: entitlement to future CF (deposit, unit trust), attributes:

o Return/yield: total financial compensation received from an investment expressed as

a % of amount invested

o Risk: probability that actual return on an investment will vary from expected return

find more resources at oneclass.com

find more resources at oneclass.com

o Liquidity: ability to sell asset w/in reasonable time at current market prices and for

reasonable transaction costs

o Time-pattern of the CF: when the expected CF from a financial asset at tb received

by the investor/lender

o Financial system (IIM) provides the potential suppliers of funds w the combos of risk,

return, liquidity, and cash flow patterns that est suit eah sae’s patiula eeds

o institutions utilise instruments to attract deficit and surplus units

o financial system facilitate flow of funds by utilising IIM

- Financial instrument: markets to describe financial assets and other instruments where there

is no organised secondary market where that instrument can be traded

▪ Types: Equity: ownership interest in an asset- ordinary, hybrid (quasi-equity)

security, preference, convertible notes

▪ Debt: contractual claim to periodic interest paym + repaym of principal

• ST M-LT

• Secured/unsecured

• Negotiable (ownership transferable commercial bills) or non (term

loan from bank)

▪ Derivatives

• Do provide actual funds for borrower, but rather facilitate the mgmt.

of certain related risk (price risk exposure + speculate)

• Futures, forward, option, swaps contracts

▪ hybrid

• incorporate both characteristics of debt + equity (pref share)

- Financial security: financial asset that can be traded in secondary market

- 1.27.00

Financial Markets

- Lending and borrowing of funds, creation and trading of financial asset (transactions)

- matching principle

o ST assets should be funded w ST liabilities + LT w LT (usually lend long and fund w ST)

- primary vs secondary market transactions

o primary: issue new financial instruments (funds obtained by the issuer) + 2ndary

existing instruments w trade (no new funds raised → no direct impact on original

issuer of security- transfer ownership from savers, provides liquidity which facilitates

restructuring of portfolios of security owners)

- direct vs intermediated financial flow markets (provider surplus, fin intermediary, user deficit)

o direct: users of funds obtain finance direct from savers- contractual agreement

between purchasers of funds and the users of funds)

o intermediated: 2 separate contractual arrangements, intermediary repackages funds

and funds are returned to intermediary before returning to supplier e.g DFI)

▪ ad: asset, atuity, edit isk diesifiatio sae’s edit isk is ltd to

intermediary) and transformation, liquidity transformation, eco of scale

- wholesale vs retail markets

- money vs capital markets

Flow of Funds and Market relationships

- financial system is composed of financial institutions, instruments and makes facilitating

transactions for goods and services and financial transactions

4 types of instruments (E,D,D,H)

find more resources at oneclass.com

find more resources at oneclass.com

- debt instruments can be ST (money <1y) or LT (capital >1y)

- equity instruments can only be in capital markets (ownership in company)

Lecture 2

- authorised deposit-taking institutions (ADIs): financial intermediation

- Main activities of commercial banking

o Importance of banks (deregulation, largest share of assets of all institutions)

o Prior to dereg (asset management- loan portfolio tailored to match available deposit

base → liability mgmt. (deposit base and other funding sources are managed to fund

loan demand- borrow direct from cap market or OBS business)

- Sources of funds (L or SE on BS)

o Deposit and investm products w liquidity, return, maturity, risk, CF structure to

attract surplus units)

o Current deposit (liquid), call/demand deposits (savings account), term deposits

(lodged- term, liquidity, IR) [financial assets- not tradable vs CDs]

o (4) negotiable certificates of deposit (CDs)

o bill acceptance liabilities

o bill of exchange: a security issued into the money market at a discount to FV (repaid

at maturity)

▪ the business (deficit unit) that issues the bill will sell the bill to an investor w

bank guarantee to increase creditworthiness- bank as acceptor

▪ bank may agree to buy bill → bank sell bill into money market – bank as

discounter→ ROLE of bank is different

o debt liabilities (M-LT issued by bank)

o debenture: bond supported by a form of security, being a charge over the assets of

the issuer

o unsecured note: bond issued w no supporting security

o foreign currency liabilities

▪ debt instruments issued into the international capital markets that are

denominated in a foreign currency

• allows diversification of funding sources, facilitate matching of fx

denominated assets

o loan capital: sources of funds w characteristic of both debt + equity (hybrid) →

subordinated (holder of security has claim on interest paym/asset of issuer, after all

other creditors are paid

o SE: ordinary shares, retained funds

- Uses of funds (asset on BS)

o Loans that give rise to entitlement to fut CF (interest+repaym)

▪ personal (investm property, fixed term loan, credit card) and housing

(mortgage, amortised loan) finance

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Finance: art and science of managing scare resources of money. Money: acts as a medium of exchange, represents a store of wealth, facilitates saving, solves divisibility problem. Financial institutions, instruments, markets which interact to facilitate the flow of funds between deficit and surplus units within the economy. Financial institutions permit the flow of funds between borrowers and lenders by facilitating financial transaction: provide investment products (surplus units, provide alternative funding sources (deficit, provide risk management products (insurance) Facilitate the flow of funds- primary financial market (creation of new financial assets) + secondary market (provide arrangement for transfer of funds by arranging trades in existing financial assets) Efficient financial system should ensure that savings will be directed to the most efficient users (vs needy) of those funds. Financial security: financial asset that can be traded in secondary market. Lending and borrowing of funds, creation and trading of financial asset (transactions)