FINS2624 Lecture Notes - Lecture 4: Risk Premium, Risk Aversion, Expected Return

4 – Markowitz Portfolio Theory

Preferences – aim to satisfy as many preferences as possible

• Utility functions assign value to each outcome (preferred outcomes = higher values)

Utility – depending only on wealth & convenience

In finance, risk refers to possibility that realized outcomes differ (better or worse) from

what is expected – neither good nor bad

• Prefer certain outcomes to stochastic ones (if everything else is equal)

Risk premium induces risk averse investors to take investments with uncertain outcome

Utility function based on investment return:

• U = utility value we assign to potential investment portfolio

• r = portfolio’s future uncertain return, Er is its expected value

• Variance measures risk (if risk free, variance = 0)

• A = constant, meaning degree of risk aversion

• U of a risky investment can be interpreted as its certainty equivalent return

Mean-variance criterion

• Utility function expresses that we like high expected returns & dislike high risk

• Some portfolios rank higher than others

i) E.g. if one portfolio has both higher E(r) & lower variance than another portfolio

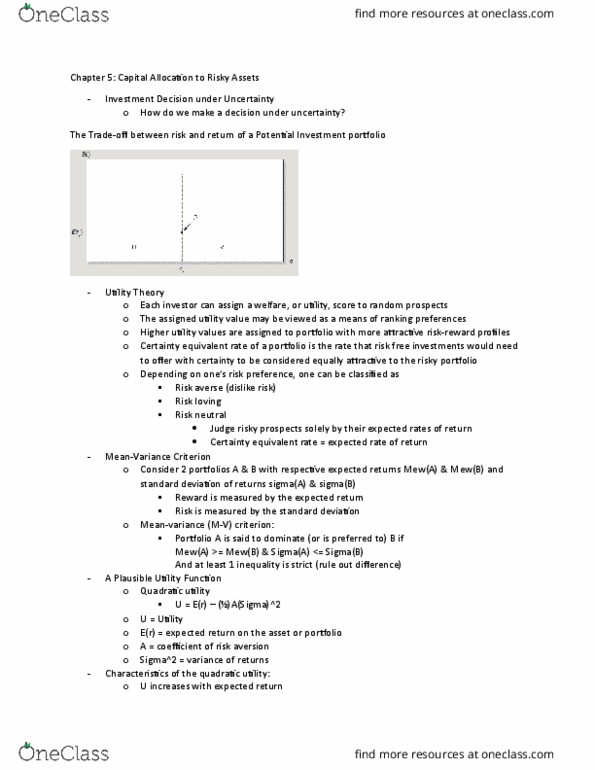

Utility – Indifference Curves

• Curves in risk-return space that connect points giving equal utility

• Two indifference curves with different levels of utilities will never intersect

Objective of investment is to achieve optimal outcome that maximizes utility

Returns of Portfolios – weighted average of returns of assets that make up portfolio

Expected return – returns generally stochastic so we deal with expected returns

• Multiply return under each possible state with associated probability of that state

Expected return of portfolio – weighted average of expected returns of its assets

Covariance – tendency of two variables to co-move (be higher of lower than respective

mean values at the same time)

Risk – variance, or standard deviation (easier to interpret) of returns

Standard deviation of the portfolio is a weighted average of the standard deviations of

its assets – just as expected return is

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Preferences aim to satisfy as many preferences as possible: utility functions assign value to each outcome (preferred outcomes = higher values) Utility depending only on wealth & convenience. In finance, risk refers to possibility that realized outcomes differ (better or worse) from what is expected neither good nor bad: prefer certain outcomes to stochastic ones (if everything else is equal) Risk premium induces risk averse investors to take investments with uncertain outcome. Mean-variance criterion: utility function expresses that we like high expected returns & dislike high risk, some portfolios rank higher than others, e. g. if one portfolio has both higher e(r) & lower variance than another portfolio. Utility indifference curves: curves in risk-return space that connect points giving equal utility, two indifference curves with different levels of utilities will never intersect. Objective of investment is to achieve optimal outcome that maximizes utility. Returns of portfolios weighted average of returns of assets that make up portfolio.