FINS2624 Lecture Notes - Lecture 5: Expected Return

41 views1 pages

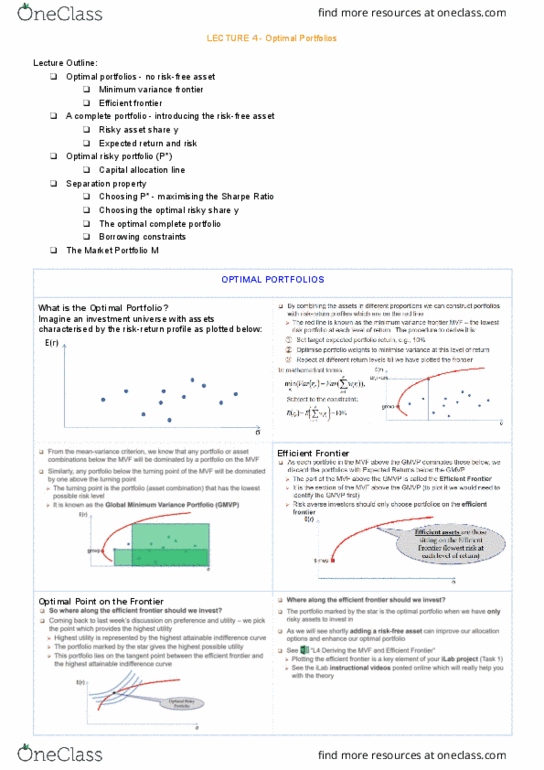

5 – Optimal Portfolios

Expected return of risk free asset = variation of risk free asset = 0

Return of complete portfolio, C:

• Fraction invested in risk-free asset = (1-y)

Expected return of complete portfolio, C:

Risk of a complete portfolio:

find more resources at oneclass.com

find more resources at oneclass.com

Unlock document

This preview shows half of the first page of the document.

Unlock all 1 pages and 3 million more documents.

Already have an account? Log in

Get access

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Class+

$8 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

30 Verified Answers

Related Documents

Related Questions

Asset W has an expected return of 10.4 percent and a beta of 1.25. If the risk-free rate is 3.2 percent, complete the following table for portfolios of Asset W and a risk-free asset. (Round your expected return answers to 2 decimal places. (e.g., 32.16) and beta answers to 3 decimal places. (e.g., 32.161))

| Percentage of Portfolio in Asset W | Portfolio Expected Return | Portfolio Beta | |||

| 0 | % | % | |||

| 25 | % | ||||

| 50 | % | ||||

| 75 | % | ||||

| 100 | % | ||||

| 125 | % | ||||

| 150 | % | ||||

| If you plot the relationship between portfolio expected return and portfolio beta, what is the slope of the line that results? (Round your answer to 2 decimal places. (e.g., 32.1616)) |

| Slope of the line | % |