ACCT2102 Lecture 7: By-product Journal Entries (both production and sales method)

This preview shows half of the first page of the document.

Unlock all 2 pages and 3 million more documents.

Get access

Related Documents

Related Questions

| ||||||||||||||||||||

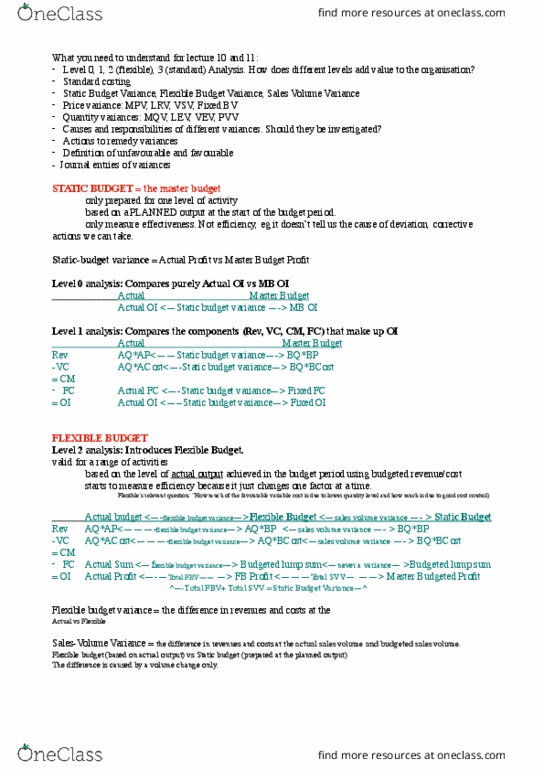

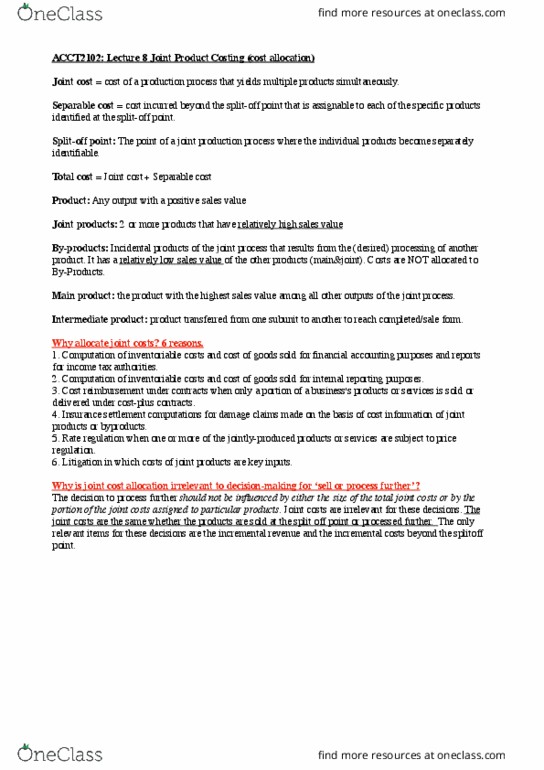

a) Joint costs up to the split off point are $187,500.

b) If joint costs are allocated based upon the sales value atsplit off, what amount of joint costs will be allocated to thewidgets?

c) Explain the difference between a joint product and abyproduct. Can a byproduct ever become a joint product? Also, can ajoint product ever become a byproduct?

Pyramid Printing Company is a printer of magazines and retailinserts. In addition, there are two joint products (food wrappingand book covers) and one byproduct (shipping-box inserts) thatoriginate from the trimmings of Pyramidâs paper rolls inproduction. The food wrapping and book covers are the same size.The shipping-box inserts are sold to online retailers for shippingbooks. All joint products and byproducts are sold as sustainablealternatives to other recycling opportunities.

Pyramidâs cost information by process follows:

| Pyramid Products | Pounds of Production | Cost |

| Magazines | 400,000 | $ 1,400,000 |

| Retail inserts | 360,000 | $ 1,000,000 |

| Food wrapping | 100,000 | $ 1,200,000 |

| Book covers | 240,000 | $ 1,600,000 |

| Shipping-box inserts | 20,000 | $ 40,000 |

The shipping-box inserts are able to be sold for $800,000 toonline retailers.

Requirements:

1 Determine the cost of food wrappingand book covers if the sales method is used for shipping-boxinserts.

2 Determine the cost of food wrappingand book covers if the production method is used for shipping boxinserts.

3 Which method would you suggest is thebest for Pyramid?

Change from the fair method to the equitymethod

Assume that an investor has accounted for a $320,000 cost, 8%investment in the investee using the fair value method(available-for-sale designation). The following additionalinformation is available:

| Cumulative Dividends Received from Investee | 8% of the Cumulative Profits Recorded by Investee | Cumulative Fair Value Adjustment for 8% Interest | |

|---|---|---|---|

| $37,500 | $98,300 | $117,600 |

Now, assume that the investor acquires an additional 17% interestin the investee (bringing the total to 25%) and concludes that itcan now exert significant influence over the investee.

Required

a. Provide the required journal entries to account for the changefrom the fair value method to the equity method for the originalinvestment.

| General Journal | ||

|---|---|---|

| Description | Debit | Credit |

b. Now, assume that the investor has accounted for its investmentusing the cost method. Provide the required journal entries toaccount for the change from the cost method to the equity methodfor the original investment.

| General Journal | ||

|---|---|---|

| Description | Debit | Credit |