ACCT2102 Lecture Notes - Lecture 9: Income Statement, Operating Budget, Controllability

Lecture 9: Responsibility Centres and Responsibility Accounting

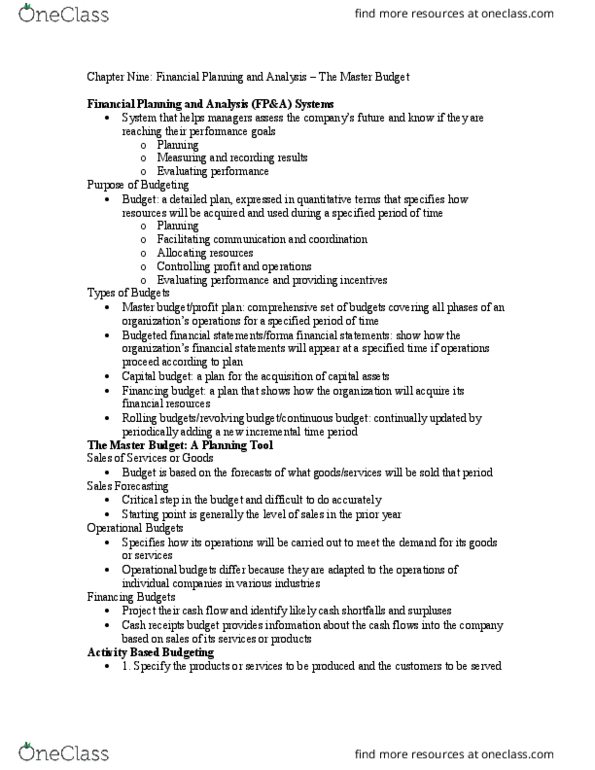

A quantitative expression of a proposed plan of action prepared by management for a specified time period

AND an aid to co-ordinate the actions needed to implement the plan.

Budget: The plan (in financial and quantitative terms) that specifies how an organisation will acquire and

use resources during a particular period of time (the next year) to achieve strategy.

■Operating decisions deal with how to best use the limited resources of an organization.

■ Financing decisions deal with how to obtain the funds to acquire those resources.

Useful when integrated with the organisation’s strategy. Budgets should be prepared when their expected

benefits exceed their expected costs.

Most widely used accounting tool for organisational:

- planning

- controlling

Organisation’s goals: Profitability, Growth, Service

Usually a rolling budget is preferred: a budget that is continually updated by adding a new time period to the

period that just ended.

-Planning vs Control

-Benefits of Budgeting

- Defines goals and objectives

- Communicates plans

- Coordinates activities

- A means of allocating resources, measuring performance and rewarding employees

-Limitations of Budgeting

-Time-consuming

-Responsibility accounting

It is a system that measures the plans, budgets, actions and actual results of each responsibility centre. It

evaluates the performance of managers of responsibility centres based on activities under their supervision.

-Responsibility centre. Why are they needed?

Each (higher-level) manager is responsible for a responsible centre. A responsible centre is a subunit of an

organisation whose manager is accountable for a specified set of activities. It is needed to ensure each

manager in the organisation is striving toward the overall goal set by top management.

- It is a functional approach

-It is about the degree of influence, rather than control

-Focuses on information sharing, not on laying blame.

4 types of responsibility centres:

1. Cost centre: the manager is accountable for costs only. (e.g. maintenance manager)

2. Revenue centre: the manager is accountable for revenues only. (e.g. sales manager)

3. Profit centre: the manager is accountable for costs and revenues. (e.g. hotel manager)

4. Investment centre: the manager is accountable for costs, revenues and investments. (regional manager)

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

A quantitative expression of a proposed plan of action prepared by management for a speci ed time period. And an aid to co-ordinate the actions needed to implement the plan. Budget: the plan (in nancial and quantitative terms) that speci es how an organisation will acquire and use resources during a particular period of time (the next year) to achieve strategy. Operating decisions deal with how to best use the limited resources of an organization. Financing decisions deal with how to obtain the funds to acquire those resources. Budgets should be prepared when their expected bene ts exceed their expected costs. Usually a rolling budget is preferred: a budget that is continually updated by adding a new time period to the period that just ended. A means of allocating resources, measuring performance and rewarding employees. It is a system that measures the plans, budgets, actions and actual results of each responsibility centre.