ACFI1001 Lecture Notes - Lecture 3: Book Value, Fixed Asset, Weighted Arithmetic Mean

Statement of financial performance – profit and loss – income statement –

statement 1

Purpose is to measure and report how much profit the business has generated over a period

Profit (or loss) is the difference between the increases in oes euity, known as income, and the

decreases in oes euity, known as expenses

Relationship between financial performance and financial position:

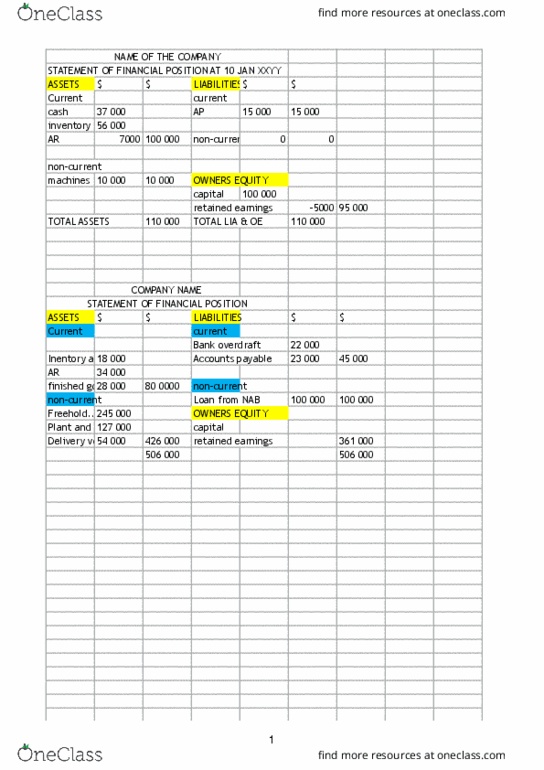

• Statement of financial position (Chapter 2) shows sapshot at a point in time

• Statement of financial performance shows generation of wealth over a period of time

• Links financial position at beginning of period to financial position at end of period

The accounting equation can show the link between statements of financial performance and

position:

• Total Assets = Total Liabilities + Owners Equity

• Total Assets = Total Liabilities + Capital + Retained Earnings

• Total Assets = Total Liabilities + Capital +/- {Profit or Loss}

• Total Assets = Total Liabilities + Capital + {Revenue – Expenses}

Format of the income statement:

Varies depending on:

• Entity structure

• Nature of operations

Gross profit refers to the difference between the revenues from sales and the cost of those sales

Operating profit refers to the increase in wealth for a period that is generated from normal

operations

Profit for the period is the profit for the year after a reasonable estimate of tax likely for the year

Cost of sales is the cost attributable to the sales revenues

find more resources at oneclass.com

find more resources at oneclass.com

Approach to cost of sales depends on type and scale of business

Normally expenses are classified under four main headings:

• cost of sales

• selling and distribution

• administration and general

• financial

Reporting period:

• For external reporting, the reporting cycle is normally one year

• For internal functions, it is common for profit figures to be prepared on a monthly basis

• An income statement can be prepared for any period, including weekly or daily depending

on need

Main criteria to recognise revenue are:

• the amount of revenue can be measured reliably

• it is probable that the eooi eefits will be received

• For sales of goods (as opposed to services) also ownership and control of the items should

pass to the buyer

• The revenue recognition criteria mean revenue is often recognised before related cash is

received

Alternatively, cash may be received in advance of revenue being recognised, e.g. a cash deposit

• This appoah is alled aual aoutig

• Cash aoutig eas recognising transactions at the time when cash flows take place –

record all transactions as and when they happen

The matching convention holds that expenses should be matched to the revenue that they helped

generate

This gives rise to three possibilities when recognising expenses in a period:

• the cash payments are the same as the expenses incurred (benefits used up or consumed)

• the cash payments are less than the expenses incurred, or

• the cash payments exceed the expenses incurred

Depreciation:

A measure of that portion of the cost (less residual value) of a fixed asset which has been consumed

during an accounting period

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Statement of financial performance profit and loss income statement statement 1. Purpose is to measure and report how much profit the business has generated over a period. Profit (or loss) is the difference between the increases in o(cid:449)(cid:374)e(cid:396)s(cid:859) e(cid:395)uity, known as income, and the decreases in o(cid:449)(cid:374)e(cid:396)s(cid:859) e(cid:395)uity, known as expenses. Varies depending on: entity structure, nature of operations. Gross profit refers to the difference between the revenues from sales and the cost of those sales. Operating profit refers to the increase in wealth for a period that is generated from normal operations. Profit for the period is the profit for the year after a reasonable estimate of tax likely for the year. Cost of sales is the cost attributable to the sales revenues. Approach to cost of sales depends on type and scale of business. Normally expenses are classified under four main headings: selling and distribution: cost of sales, administration and general financial.