ACFI2070 Lecture Notes - Lecture 4: Economic Value Added, Discounted Cash Flow, Cash Flow

29 Jun 2018

School

Department

Course

Professor

0

2

21

)1(

...

)1(

)1(

C

k

C

k

C

k

C

N PVo r

n

n

Module 2: Project Evaluation: weeks 4-5.

Learning Objectives:

LO1: Understand the capital expenditure process.

LO2: Outline the decision rules for each of the main methods of project evaluation.

LO3: Explain advantages and disadvantages of the main project evaluation methods.

LO4: Compare discounted cash flow methods and non-discounted cash flow methods.

LO5: Explain the principles used in estimating project cash flows.

LO6: Explain why the net present value method is preferred to all other methods.

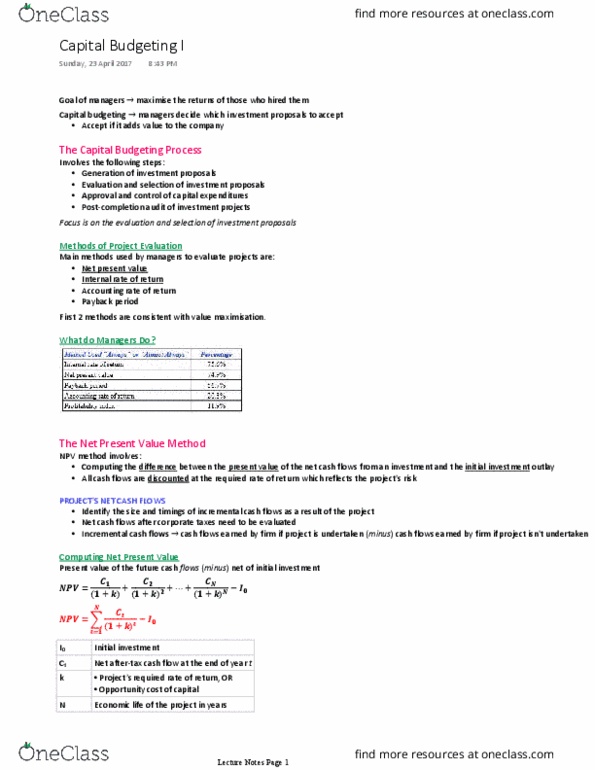

LO1: The Capital Expenditure Process.

The objective of investment decisions is to maximise shareholder wealth.

The capital expenditure process involves:

1. Generation of investment proposals.

2. Evaluation and selection of those proposals.

3. Approval and control of capital expenditures.

4. Post-completion audit of investment projects.

LO2: Discounted Cash Flow Methods:

Discounted cash flow methods involve the process of discounting a series of net cash flows to their

present values. They involve the following methods:

NPV

… Initial cash OUTFLOW (investment) + PV of all future cash flows.

It is the difference between the net cash flows from an investment, discounted at the required rate

of return, and the initial investment outlay. By measuring a project’s net cash flows, we can forecast

expected net profit from a project, and estimate the net cash flows directly.

The standard formula for NPV is:

n

t

t

t

C

k

C

NPV

1

0

1

If NPV > 0 Accept project

If NPV <0 Reject project

0

where:

= initial cash outlay on project

= net cash flow generated by project at time t

= life of the project

= required rate of return

t

C

C

n

k

find more resources at oneclass.com

find more resources at oneclass.com

A project’s required rate of return (k) is sometimes termed ‘the opportunity cost of capital’ because:

a) Undertaking the project would mean that other alternative investment

opportunities may have to be foregone; and

b) The market provides the funds to invest, but demands the rate of return (k)- thus k

is the cost of obtaining capital.

NPV and Required Rate of Return:

The NPV method is consistent with the company’s objective of maximising shareholders’ wealth. A

project with a positive NPV will leave the company better off than before the project, and other

things being equal, the market value of the company’s shares should increase.

Example:

Investment of $9000, net cash flows of $5090, $4500 and $400 at end of years 1,2 and 3

respectively. Assumed required RoR is 10% p.a. What is NPV of project?

n

t

t

t

C

k

C

NPV

1

0

1

= 5090/(1.10) + 4500/(1.10)2 + 4000/(1.10)3 - 9000

= 4627.272727 + 3719.008265 + 3005.259204 – 9000

= 2351.540195

= $2,351.54

Thus, using a discount rate of 10%, the project’s NPV = +2 352, which is greater than 0 and therefore

acceptable.

Internal Rate of Return

The IRR is the discount rate at which NPV=0 (initial investment / outlay= PV of future benefits). It is

compared to the required rate of return (k). Meaning, if the discount rate is set at this rate, the

project breaks even. If the discount rate is greater than this rate (NPV<0), the project would reduce

firm value, but if the discount rate is lower than this rate (NPV>0), the project would increase firm

value.

Decision Rule: If IRR greater than K, accept project.

By setting the NPV formula to 0, and treating the rate of return as the unknown, the IRR is given by:

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Lo2: outline the decision rules for each of the main methods of project evaluation. Lo3: explain advantages and disadvantages of the main project evaluation methods. Lo4: compare discounted cash flow methods and non-discounted cash flow methods. Lo5: explain the principles used in estimating project cash flows. Lo6: explain why the net present value method is preferred to all other methods. The objective of investment decisions is to maximise shareholder wealth. The capital expenditure process involves: generation of investment proposals, evaluation and selection of those proposals, approval and control of capital expenditures, post-completion audit of investment projects. Discounted cash flow methods involve the process of discounting a series of net cash flows to their present values. Initial cash outflow (investment) + pv of all future cash flows. It is the difference between the net cash flows from an investment, discounted at the required rate of return, and the initial investment outlay.