FIN3109 Lecture Notes - Lecture 4: Common Stock, Procyclical And Countercyclical, Call Option

FIN3109 – Module 4

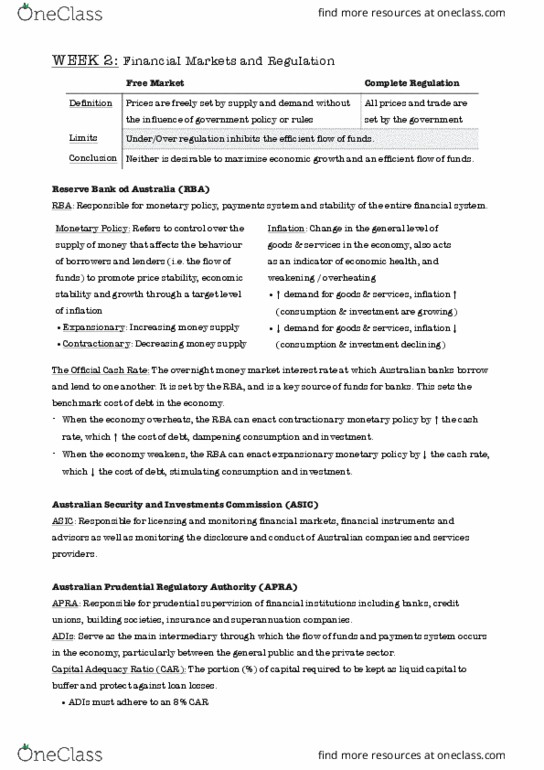

- Prudential Supervision

oThe Australian Prudential Regulation Authority (APRA)

Prudential regulator of financial institutions since 1998

oPrudential Regulation

Requirements that limit the risk-taking of banks and other Financial Institutions in

order to protect depositor’s funds, the finds of other creditors, and to maintain

financial system stability.

- Moral Hazard

oBank managers may take too much risk with depositors’ funds if the government guarantees

the finds or if they believe they are so important the government will always bail them out in

a crisis

- APRA’s Approach to Prudential Supervision

oAPRA aims to encourage responsible behaviour by financial institutions and ensure that

managers are responsible for their decisions

oThe prudential framework consists of:

Prudential Statements that aim to ensure ADIs effectively manage their risks

The capital adequacy requirements (CAR) including minimum prudential capital

ratios (PCRs)

- Prudential Standards

oThe role of the standards is to reduce the likelihood of illiquidity or insolvency

- The Capital Adequacy Requirement (CAR)

oCAR’s role is to ensure an ADI has sufficient equity capital to sustain its solvency should it

incur losses

Used internationally 0 The Basel Committee on Banking Supervision developed a

capital adequacy model (the Basel Accord or Basel 1) in 1988

It was revised and Basel 2 began in operation in 2008

New revisions, termed Basel 3 were introduced in 2013 and the staged roll-out is

continuing

- Basel 1 and Basel 2

oCAR =

oCapital: Provides a cushion to absorb losses

oRisk Adjustment: Different assets have different risk exposures and more capital should be

required where the risk is greater

oQualified Capital: Tier 1 (high quality) and Tier 2 (lower quality) capital

- Total Risk-weighted Assets

o1988: Banks estimated only credit risk: On-balance sheet + off balance sheet

o1996 Amendment: Banks also measure market risk

Interest rate risk + exchange rate risk + equity price risk + commodity price risk

o2008 Basel 2: Banks also estimate Operational Risk

- Basel 2 Amendments

oStandard CAR was unchanged: CAR =

oKey changes:

Revision to risk weightings, including the use of credit ratings by agencies such as

Standard & Poors. Credit ratings affect the risk weighting applied to loans.

The inclusion of operational risk in the calculation of the risk adjusted capital ratio

for a financial institution

The possible inclusion of Tier 3 capital as part of the capital base

find more resources at oneclass.com

find more resources at oneclass.com

- Tier 3 Capital

oConsisted of:

Subordinated debt with, among other qualities, a minimum initial maturity of at

least 2 years. It must also be unsecured.

Used to cover market risk only

- Measuring Operational Risk

o

oWhere,

The capital charge under the Standardised Approach

Annual gross income in a given year, as defined above in the Basic Indicator

Approach, for each of the eight business lines

A fixed percentage, set by the Committee, relating the level of required capital to

the level of the gross income for each of the eight business lines.

oOperational Risk: Based on gross income earned by each business line weighted by a factor

- Basel 3

oBasel 3 is a response to the Global Financial Crisis

oImplementation began on January 1 2013

oThe target date for full implementation after all transition periods is 2019

- Basel 3 changes include:

oTier 1 Capital has been abolished. The reason is to ensure that market risks are covered with

the same quality of capital as credit and operational risks.

oMinimum PCRs

Common Equity Tier 1 Capital (CET1)

Comprising ordinary shares and retained earnings, which are the main

component of Tier 1 capital, must be at least 4.5% of the risk adjusted assets

Total Tier 1 capital must be at least 6% of risk adjusted assets

And Total Capital (Tier 1 + Tier 2) must be at least 8% of risk adjusted assets

APRA implemented these strict minimums capital on January 1 2013

oConservation buffer: Outside periods of stress, banks hold capital above the regulatory

minimum, large enough to remain above the minimum even in a sector-wide downturn. The

recommended or benchmark size of the buffer is 2.5% of risk-adjusted assets and the buffer

should be comprised of Common Equity Tier 1 Capital (CET1)

oGlobally, the buffer will be phased in from 2016 to 2019.

oHowever, the APRA has decided that it will be fully implemented in Australia from January 1

2016.

oCountercyclical Buffer:

In addition to the conservation buffer, from 1 January 2016, APRA may, by notice in

writing to all ADIs, require them to hold additional Common Equity Tier 1 Capital, of

between 0 and 2.5% of total risk-weighted assets, as a countercyclical capital buffer.

Hence, there will be a capital buffer (CB) comprising the conservation buffer plus

any countercyclical buffer.

CB = Conservation Buffer + Countercyclical Buffer

oIt is not mandatory that banks meet the capital buffer (CB) fully, but they will face

restrictions if they do no. E.g. Restrictions on dividend issues, staff bonuses etc.

oAssuming there is no countercyclical buffer in place, banks will generally need to hold a

benchmark level of 7% CET1 capital from Jan 2016 (4.5% + 2.5%)

oHowever, our 4 largest banks will need to hold a benchmark of level 8% because they have

been designated ‘systemically important banks’

oAPRA has announced that stronger capital benchmarks, to ensure Australian banks are

‘unquestionably strong’ will be implemented as of January 2020.

find more resources at oneclass.com

find more resources at oneclass.com

oLeverage Ratio: A supplementary (or back-stop) ratio to measure to further limit risk.

The trial minimum leverage ratio is:

Leverage Ratio:

oLiquidity Coverage Ratio (LCR) introduced on January 1 2015. Larger banks must maintain an

adequate level of unencumbered, high-quality liquid assets that can be converted into cash

to meet its liquidity needs for a 30 calendar day time horizon under a significantly sever

liquidity stress scenario specified by supervisors.

LCR:

oCommitted Liquidity Facility (CLF)

Because Australia has had relatively low levels of HQLAs in recent years, the Basel

Committee permitted Australia to alter the definition of HQLAs so as to allow banks

to access liquidity from their central bank.

Hence, the RBA has initiated a Committed Liquidity Facility. Banks will pay an

ongoing access fee of 15 basis points of the size of their facility, and borrowed

liquidity will incur interest of 25 basis points above the cash rate.

Hence, the LCR requirement in Australia could be written as

LCR =

oNet Stable Funding Ratio: As of January 1 2018, banks under the LCR rules must adhere to a

second, longer term liquidity measure. The time horizon for this ratio is 1 year.

NSFR:

- Financial System Enquiry

oIn addition to increasing mortgage risk weights for major banks, the Financial System

Enquiry made a number of recommendations regarding banking regulation and the

government endorsed these in October 2015.

oAmong these is the development of a template for reporting ADI capital ratios that is

transparent against the minimum Basel capital framework

oAlso included is the continuation of the financial claims scheme that covers depositors to a

maximum of $250000 per account holder per ADI. It will continue to be funded in an ex-

poste manner rather than through a bank deposit tax.

oThat is, the government will initially supply the funds in the event of insolvency and these

will be recovered in the liquidation process.

- Banking System Stability

oBanking systems have always experienced crises.

oThe RBA promotes stability through

Monetary policy to influence inflation and economic growth

Overseeing the payments system

Acting as lender-of-last resort

Monitoring financial and economic data – it reports half-yearly

oThe RBA examines key indicators of financial performance:

Profitability of Australian Banks

A direct indicator of viability

Losses by and ADI can trigger runs on deposits in that similar institutions

Asset Quality of Australian Banks

Look at the proportion of impaired assets and losses on loan defaults

Capital Holdings of Australian Banks

The amount of a bank’s capital relative to its size indicates its ability to

withstand losses

Liquidity of Australian Banks

Does and ADI hold adequate liquid assets?

The Share Market’s Assessment of Australian Banks

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Prudential supervision: the australian prudential regulation authority (apra) Prudential regulator of financial institutions since 1998: prudential regulation. Requirements that limit the risk-taking of banks and other financial institutions in order to protect depositor"s funds, the finds of other creditors, and to maintain financial system stability. Moral hazard: bank managers may take too much risk with depositors" funds if the government guarantees the finds or if they believe they are so important the government will always bail them out in a crisis. Apra"s approach to prudential supervision: apra aims to encourage responsible behaviour by financial institutions and ensure that managers are responsible for their decisions, the prudential framework consists of: Prudential statements that aim to ensure adis effectively manage their risks. The capital adequacy requirements (car) including minimum prudential capital ratios (pcrs) Prudential standards: the role of the standards is to reduce the likelihood of illiquidity or insolvency.