ACCT3321 Lecture Notes - Lecture 7: Book Value, Financial Statement, Natural Gas Field

CHAPTER 34

Accounting for mineral resources

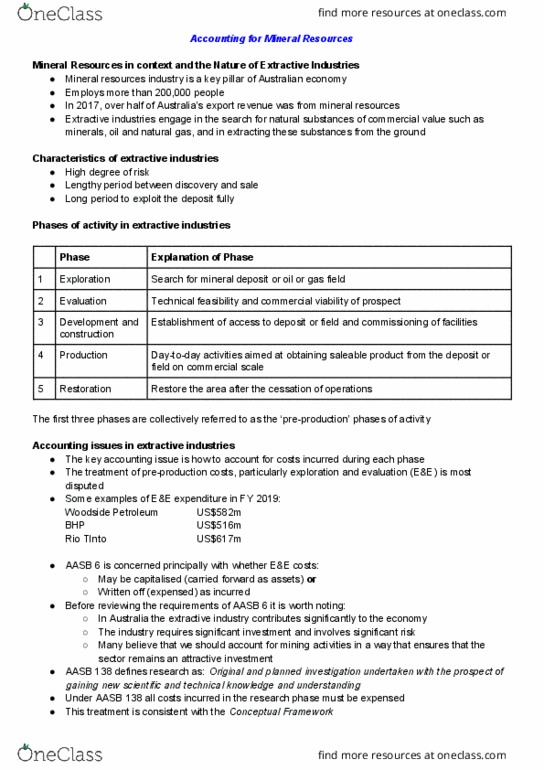

- Extractive industries are those industries involved in finding and removing wasting

natural resources in or near the earths’ crust

- Descriptions

- AASB 6 provides limited guidance on accounting policy because:

oHigh risk with the potential for, but no guarantee of, high rewards.

Costs are incurred for the hope of finding resources

oTime and cost to produce

Once mineral reserves are discovered, there can be considerable

additional expenditure involved in developing and producing those

reserves

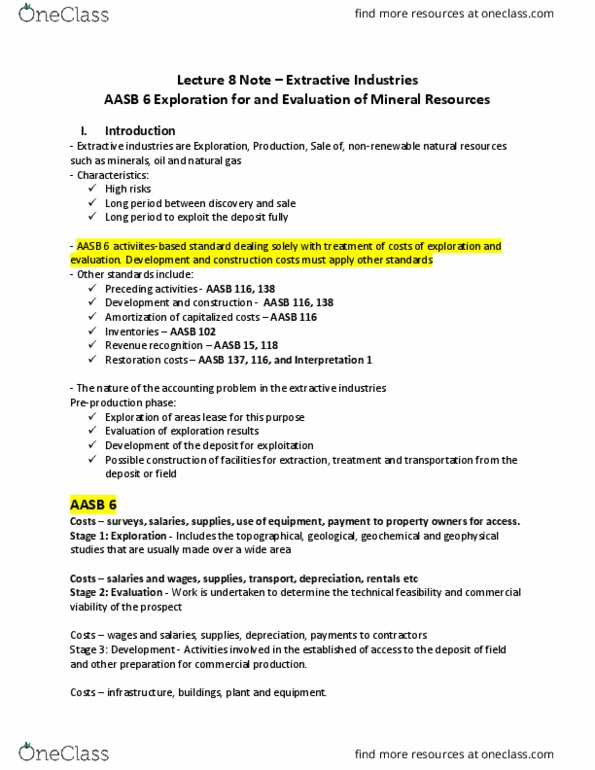

OBJECTIVE OF AASB 16

- limited to specifying the financial reporting for the exploration for and evaluation of

mineral resources

SCOPE

- Limited to accounting for E&E expenditures and does not address other aspects of

accounting by entities engaged in the exploration for and evaluation of mineral

resources

- Does not deal with prospecting, development and productions

RECOGNITION OF EXPLOATION AND EVALUATION ASSETS

-Temporary exemption from AASB 108 para 11 and 12

oCan defer capitalising on the balance sheet – nearly all exploration and

evaluation expenditure to recognising all such expenditure in profit or loss

oE&E relates to areas of interest – an individual geological area which is

considered to constitute a favourable environment for the presence of a

mineral deposit or an oil or natural gas field, or has been proved to contain

such a deposit or field

oExemption – allows the continued application or use of much of the existing

industry accounting practices for recognition and measurement of E&E assets

and expenditures

oMost common ways to account

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Extractive industries are those industries involved in finding and removing wasting natural resources in or near the earths" crust. Aasb 6 provides limited guidance on accounting policy because: high risk with the potential for, but no guarantee of, high rewards. Costs are incurred for the hope of finding resources: time and cost to produce. Once mineral reserves are discovered, there can be considerable additional expenditure involved in developing and producing those reserves. Limited to specifying the financial reporting for the exploration for and evaluation of mineral resources. Limited to accounting for e&e expenditures and does not address other aspects of accounting by entities engaged in the exploration for and evaluation of mineral resources. Does not deal with prospecting, development and productions. Successful efforts method only those costs directly related to the discovery, acquisition or development of specific, distinct mineral reserves are capitalised and accumulated as part of a cost centre.