FNCE 370 Lecture Notes - Lecture 17: Marginal Cost, Economic Equilibrium, Perfect Competition

Document Summary

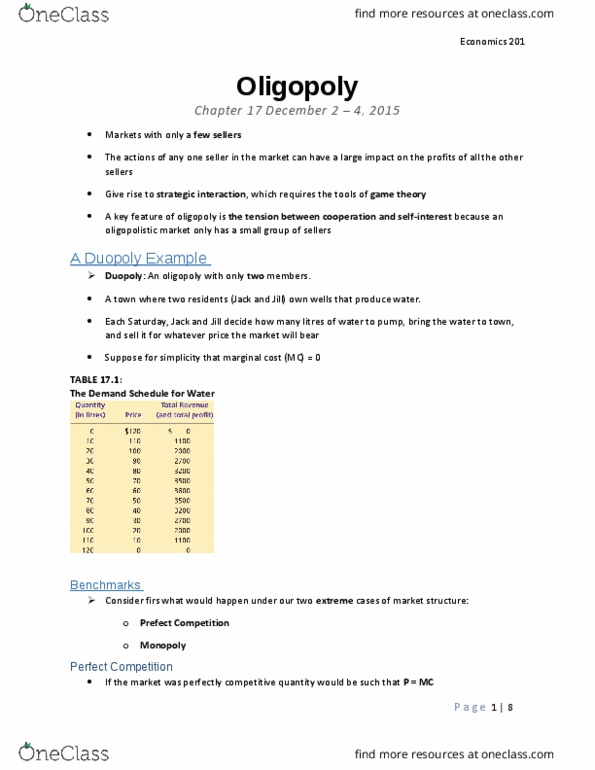

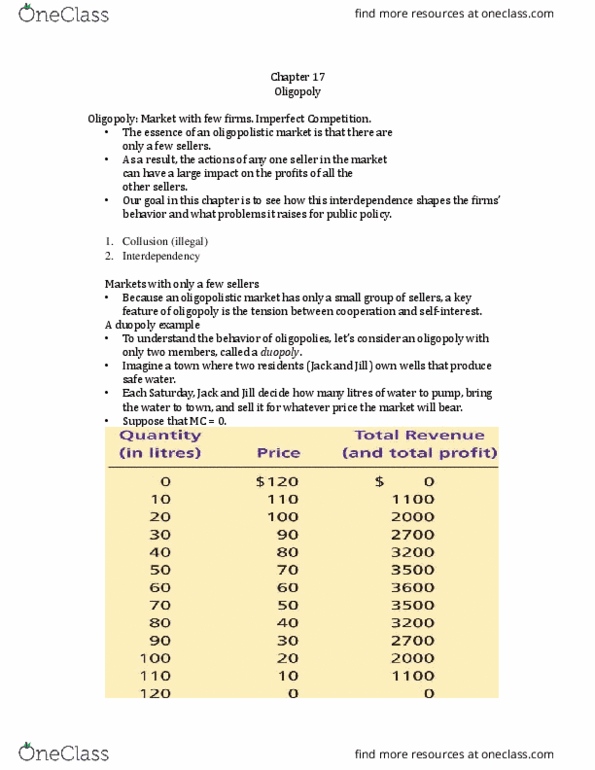

Chapter 17 - oligopoly: markets with only a few sellers. Imagine a town in which only two residents-jack and jill-own wells that pro- duce water safe for drinking. Each saturday, jack and jill decide how many litres of water to pump, bring the water to town, and sell it for whatever price the market will bear. To keep things simple, suppose that jack and jill can pump as much water as they want without cost. That is, the marginal cost of water equals zero. 17. 1 shows the town"s demand schedule for water. The first column shows the total quantity demanded, and the second column shows the price. If the two well owners sell a total of 10 l of water, water goes for per litre. If they sell a total of 20 l, the price falls to per litre. If you graphed these two columns of numbers, you would get a standard downward-sloping demand curve.