ACTG 1P12 Lecture Notes - Lecture 13: Contribution Margin, Fixed Cost, Earnings Before Interest And Taxes

Document Summary

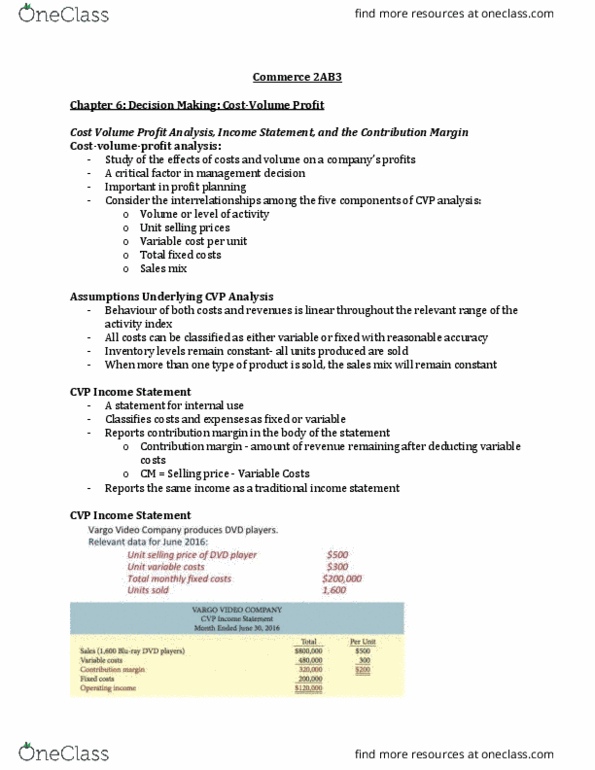

Examines the behaviour of total revenues, total costs and operating income as changes occur in the output level, selling price, variable costs or fixed costs. Inventory levels remain constant all units produced are sold. The amount of revenue that remains after variable costs have been deducted: total amount, per unit basis. Contribution margin/unit = selling price (sp) variable cost per unit (vc) Contribution margin percentage = c(cid:2925)(cid:2924)(cid:2930)(cid:2928)i(cid:2912)(cid:2931)(cid:2930)i(cid:2925)(cid:2924) m(cid:2911)(cid:2928)(cid:2917)i(cid:2924) p(cid:2915)(cid:2928) (cid:2905)(cid:2924)i(cid:2930) (cid:4666)(cid:2903)p (cid:2906)c(cid:4667) (cid:2903)(cid:2915)lli(cid:2924)(cid:2917) p(cid:2928)i(cid:2913)(cid:2915) p(cid:2915)(cid:2928) (cid:2905)(cid:2924)i(cid:2930) Contribution margin per unit is constant because both revenue and variable costs per unit have been defined as being constant. Total contribution margin fluctuates in direct proportion to sales volume. Naylor manufacturing inc. sold 8000 units and recorded sales of 000 for the first month of: in making the sales, the company incurred the following costs and expenses: 40 000: prepare an income statement, calculate the contribution margin per unit, calculate the contribution margin ratio.