ACTG 1P91 Lecture Notes - Lecture 3: Income Statement, Accrual, Deferral

28 Oct 2018

School

Department

Course

Professor

ACTG 1P91 verified notes

3/26View all

Document Summary

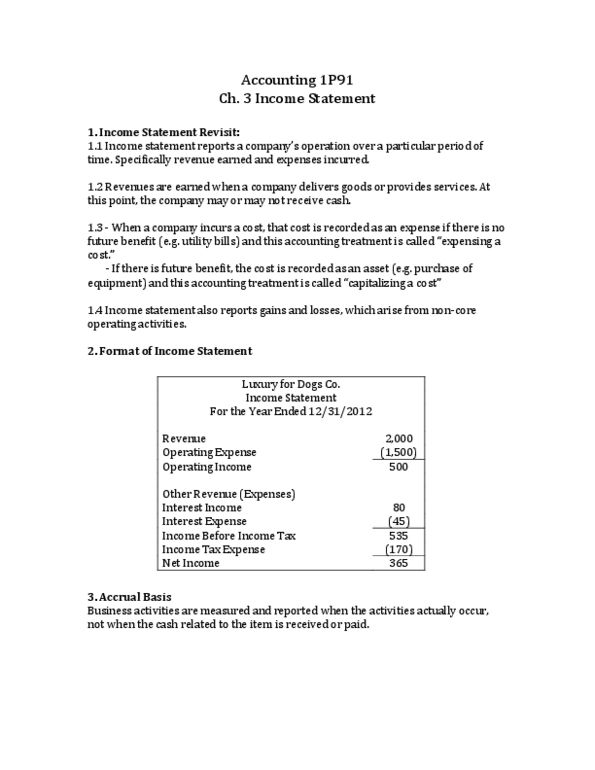

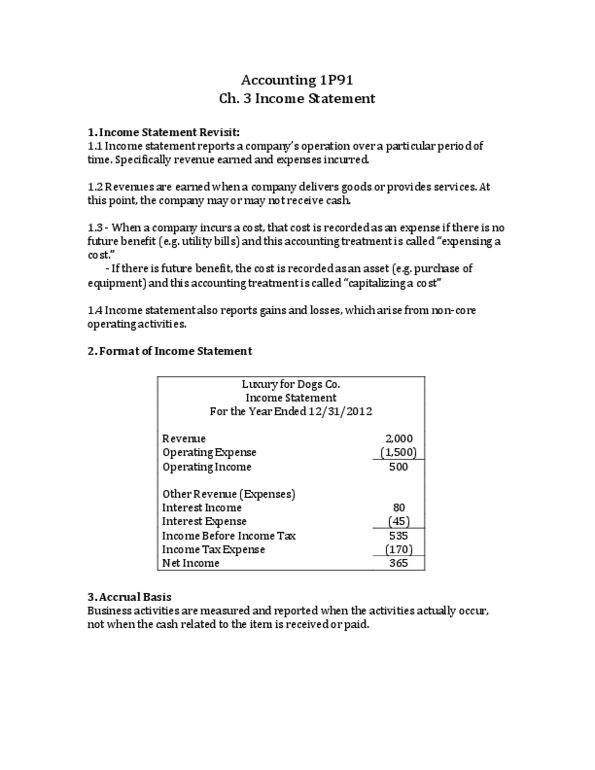

Time assumption: we can cut time in small pieces ex; ending the year at dec 31. Accrual basis: followed in tax accounting and has aspects of cash basis. Investors cannot wait till end of year 10 to know what is going on, o we use accrual basis and cash basis. Specifically reports revenues that are earned and expenses that are incurred. Revenues are earned when a company delivers goods or performs services. At this point, the company may or may not receive cash. When a company incurs a cost, that cost is recorded as an expense if there is no future (cid:271)e(cid:374)efit (cid:894)for e(cid:454)a(cid:373)ple; utilit(cid:455) (cid:271)ill(cid:895) a(cid:374)d this a(cid:272)(cid:272)ou(cid:374)ti(cid:374)g treat(cid:373)e(cid:374)t is (cid:272)alled (cid:862)e(cid:454)pe(cid:374)si(cid:374)g a (cid:272)ost(cid:863) If there is a future benefit, the cost is recorded as an asset (ex; purchase of a truck) and this a(cid:272)(cid:272)ou(cid:374)ti(cid:374)g treat(cid:373)e(cid:374)t i (cid:272)alled (cid:862)(cid:272)apitalizi(cid:374)g a (cid:272)ost(cid:863). Is also reports gains and losses, which arise from non-core operating activities.