ECON 3P03 Lecture Notes - Interest Rate, Weighted Arithmetic Mean

19 Dec 2013

School

Department

Course

Professor

Document Summary

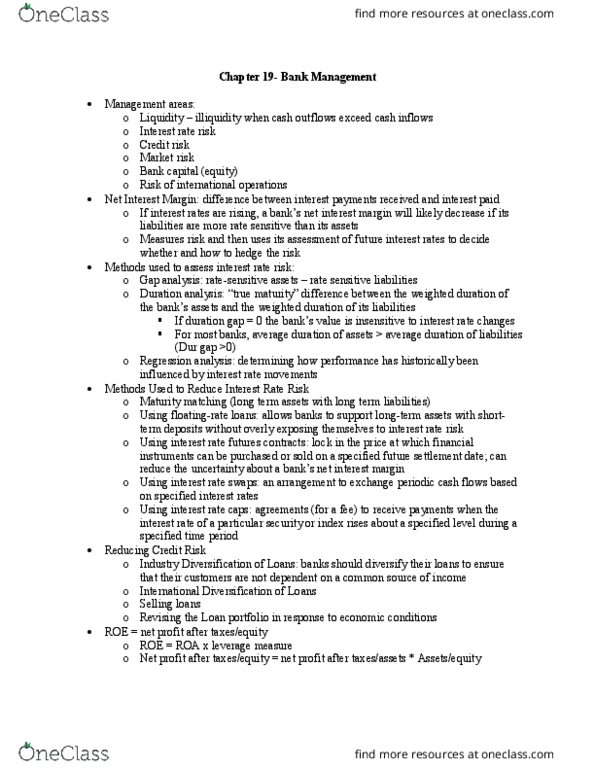

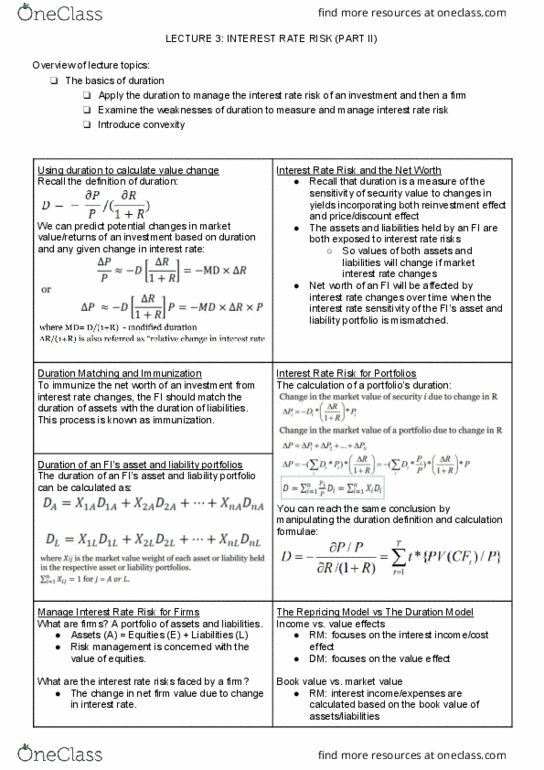

Higher interest rates also affect the value of fixed-rate assets and liabilities on the books of the bank and thus its net worth. The market value of longer-term assets and liabilities is more profoundly affected by changes in interest rates. In order to assess the effect of changes in interest rates on a bank"s net worth we need to develop measures of asset and liability average (weighted) duration. A measure of net duration is then used to assess how the bank"s net worth responds to changes in interest rates. In general, the following relationship between changes in interest rates and changes in the measure of net duration exists. % net worth = - ( i %) x (du r) where: du r represents net duration. Average duration is a weighted average of individual durations. The weights reflect the percentage of total assets or total liabilities to third parties that each asset or liability represents.