MKTG 3P24 Lecture 7: Tax 1

3 Nov 2017

School

Department

Course

Professor

Document Summary

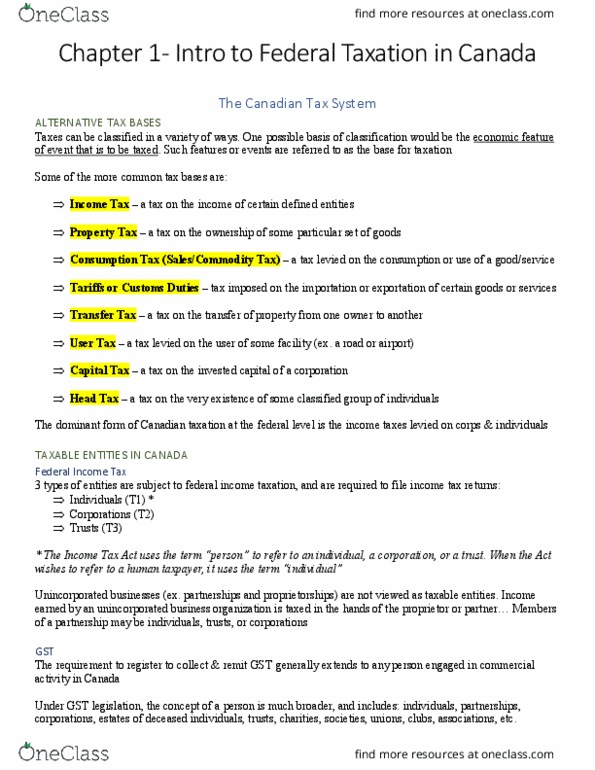

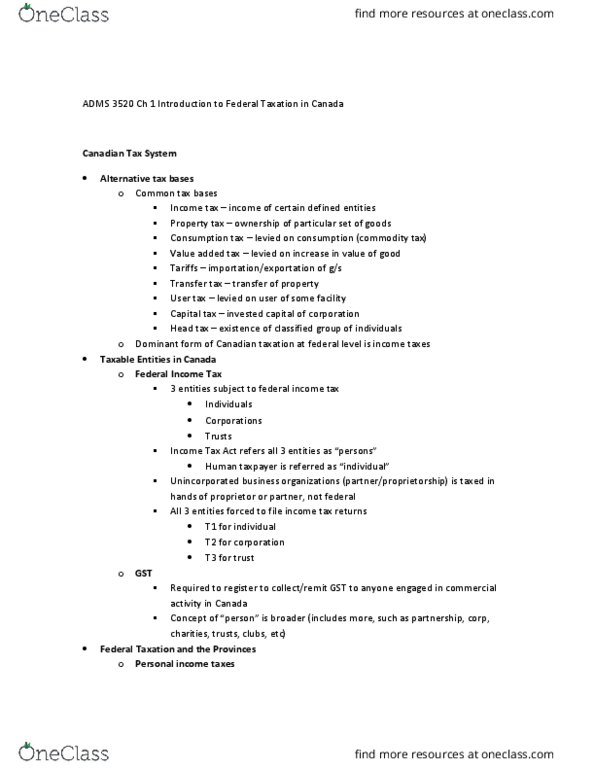

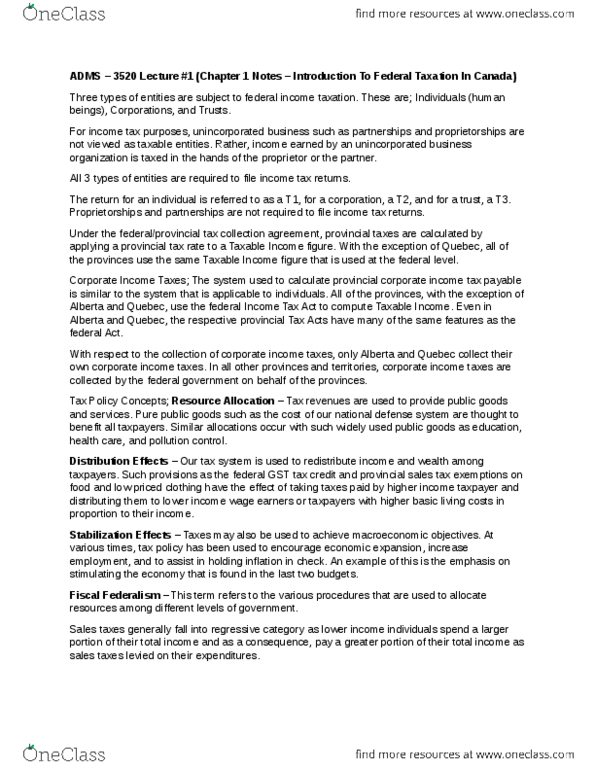

Whe(cid:374) the a(cid:272)t refers to a hu(cid:373)a(cid:374) ta(cid:454)pa(cid:455)er, it uses the ter(cid:373) (cid:862)i(cid:374)dividual(cid:863) All three taxable entities must file an income tax return. Individual t1: corporation t2, trust t3. Proprietorships and partnerships do not file income tax returns as they are not taxable entities. Requirement to register to collect and remit gst generally extends to any person engaged in commercial activity in canada. Definition of person in terms of gst is different, includes: individuals, partnerships, corporations, estates of deceased individuals, trusts, charities, societies, unions, clubs, associations, commissions, and other organizations. Federal, provincial, and territorial governments have the power to impose taxes. Provinces and territories are limited to taxation of income earned in the particular province and the income of persons resident in that province. Provinces impose both personal and corporate taxes. Provincial tax rate applied to taxable income figure to calculate provincial tax: other than quebec all provinces use same taxable income figure that is used at the federal level.