ECON 201 Lecture Notes - Lecture 18: Perfect Competition, Demand Curve, Marginal Cost

6 Nov 2018

School

Department

Course

Professor

ECON 201 verified notes

18/25View all

Document Summary

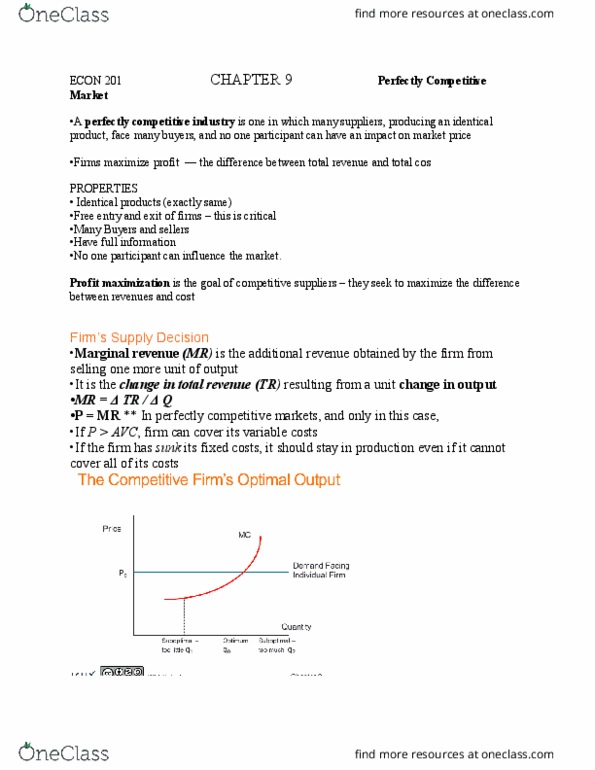

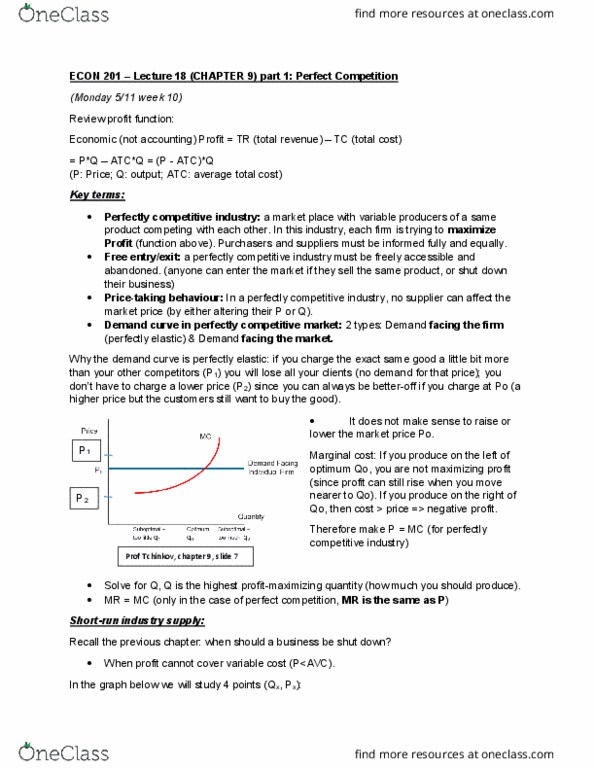

Econ 201 lecture 18 (chapter 9) part 1: perfect competition (monday 5/11 week 10) Economic (not accounting) profit = tr (total revenue) tc (total cost) = p*q atc*q = (p - atc)*q (p: price; q: output; atc: average total cost) Key terms: perfectly competitive industry: a market place with variable producers of a same product competing with each other. In this industry, each firm is trying to maximize. It does not make sense to raise or. Marginal cost: if you produce on the left of optimum qo, you are not maximizing profit (since profit can still rise when you move nearer to qo). Qo, then cost > price => negative profit. Therefore make p = mc (for perfectly competitive industry) Prof tchinkov, chapter 9, slide 7: solve for q, q is the highest profit-maximizing quantity (how much you should produce), mr = mc (only in the case of perfect competition, mr is the same as p)