FINA 385 Lecture Notes - Lecture 2: Mutual Fund, Risk Premium, Invertible Matrix

28 Jun 2016

School

Department

Course

Professor

Document Summary

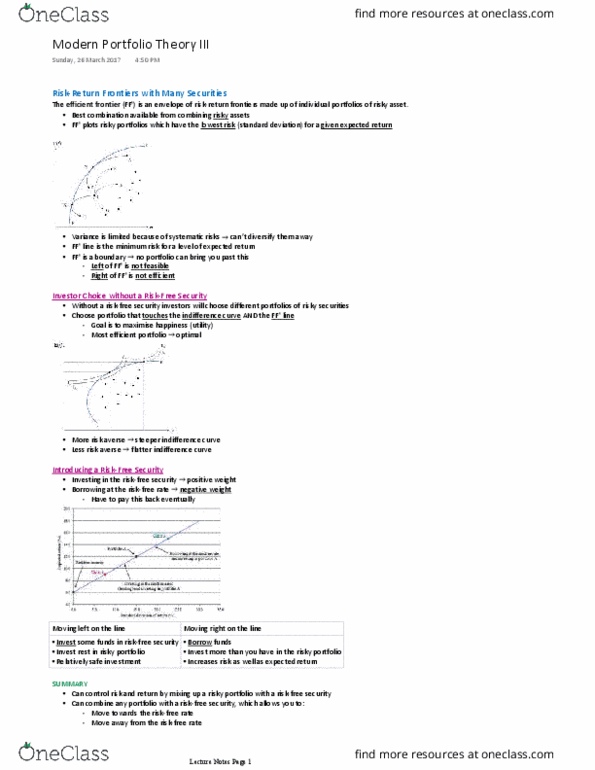

Capital allocation decision: the choice between risk-free and risky assets. Asset allocation decision: the distribution of risky investments across di erent classes of assets (e. g. , stock, bonds, real estate etc. ) To solve the problem rst we determine the risk return tradeo . Then show how risk aversion determines the optimal mix of risky and risk free assets: we do not distinguish between di erent classes of risky assets. That is, we skip the step of asset allocation in portfolio construction: in security selection we consider two risky securities and then extend the analysis to more than two risky securities, we consider only static model of trading: We assume that an investor trades only once (today) and receives payo s in the future. The investment horizon could be a few days, months or years: our analysis is called mean variance analysis since it is based on mean variance preferences.