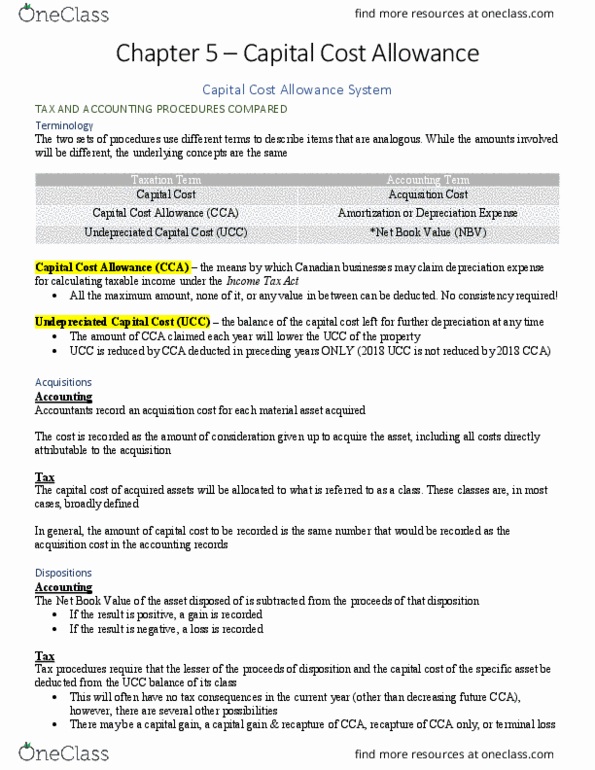

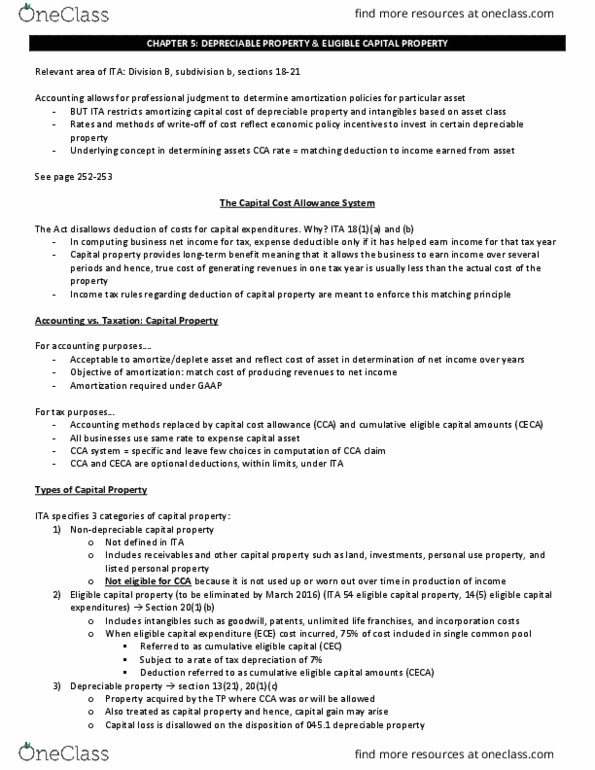

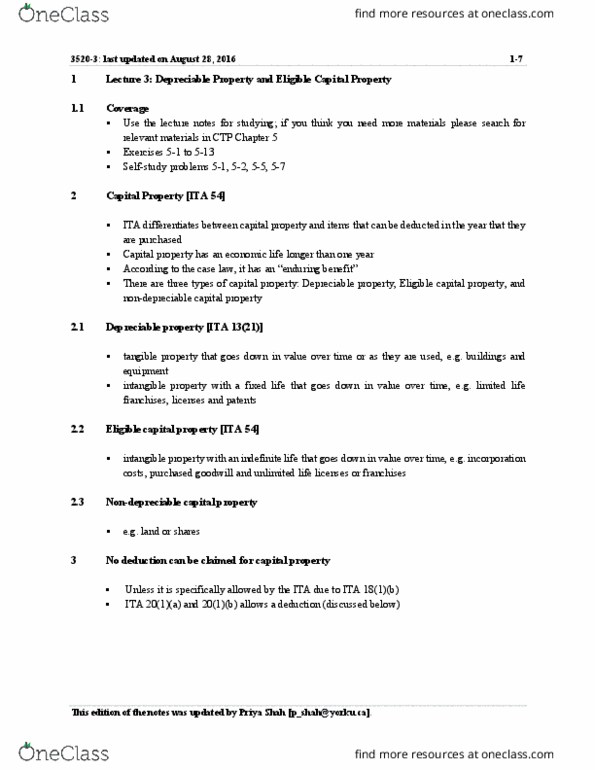

ACCT-4021EL Lecture Notes - Lecture 4: Capital Cost Allowance, Deferred Income, Financial Statement

Document Summary

Get access

Related Documents

Related Questions

12. For the purpose of government-wide financial statements, thecost of cleaning up a government-owned landfill and closing thelandfill

A) Is not recognized until the costs are actually incurred

B) Is accrued and amortized over the expected useful life of thelandfill

C) Is accrued on a pro-rated basis each period based on how fullthe landfill is

D) Is accrued in full at the time the costs become estimable

E) Is treated as an encumbrance at the time it become estimable andas an expenditure when it is actually paid

13. Drye Township has received adonation of a rare painting worth $1,000,000. For Drye'sgovernment-wide financial statements, three criteria must be metbefore Drye can opt not to recognize the painting as an asset.Which of the following is not one of the three criteria?(1.) Thepainting is held for public exhibition, education, or research infurtherance of public service, rather than financial gain.(2.) Thepainting is scheduled to be sold immediately at auction.(3.) Thepainting is protected, kept unencumbered, cared for, andpreserved.

A) Item 1 is not one of the three criteria

B) Item 2 is not one of the three criteria

C) Item 3 is not one of the three criteria

D) All three items are required criteria

E) None of the three items are required criteria

14. Which of the following is nota criterion of a capital lease?

A) The lease transfers ownership of the property to the lesseeby the end of the lease term

B) The present value of the minimum lease payments equals orexceeds 90 percent of the fair value of the leased property, net oflessor's investment tax credit

C) The lease contains an option to purchase the leased property ata bargain price

D) The lease contains an option to renew

E) The lease term is equal to or greater than 75 percent of theestimated economic life of the leased property

15. Which statement is falseregarding the government-wide Statement of Net Assets?

A) The purpose of the Statement of Net Assets is to report theeconomic resources of the government as a whole

B) Assets are reported excluding capital assets

C) Capital assets are reported net of depreciation

D) Investments are reported at fair value rather than historicalcost

E) Business-type activities include Enterprise Funds

16. Which statement is falseregarding the Balance Sheet for Fund-Based Statements?

A) The Balance Sheet for Fund-Based Statements measures onlycurrent financial resources of the governmental entity

B) The Balance Sheet for Fund-Based Statements uses the modifiedaccrual method for timing purposes

C) Capital assets are not reported on the Balance Sheet forFund-Based Statements

D) The Balance Sheet for Fund-Based Statements measures onlylong-term financial resources of the governmental entity

E) Long-term debts are not reported on the Balance Sheet forFund-Based Statements

17. The city operates a publicpool where each person is assessed a $2 entrance fee. Which fund ismost appropriate to record these revenues?

A) General Fund

B) Enterprise Fund

C) Special Revenue Fund

D) Internal Service Fund

E) Capital Projects Fund

18. Which of the following typesof health care organizations follow FASB Accounting StandardsCodification for GAAP?

Investor-Owned Health Care Enterprises | Not-for-Profit Organizations | Governmental Health Care Organizations | |

A) | Yes | Yes | No |

B) | Yes | Yes | Yes |

C) | No | No | Yes |

D) | Yes | No | Yes |

E) | Yes | No | No |

A) Entry A

B) Entry B

C) Entry C

D) Entry D

E) Entry E

19. In accruing patient chargesfor the current month, which one of the following accounts should ahospital credit?

A) Accounts Payable

B) Deferred Revenue

C) Unearned Revenue

D) Patient Service Revenues

E) Accounts Receivable

20. Which account would becredited in recording a gift of medicine to a nursing home from anoutside party?

A) Nonoperating Gain - Contributions

B) Contractual Adjustments

C) Patient Service Revenues

D) Drugs and Medicines

E) Nonoperating Revenues - Contribution

21. Unconditional transfers ofcash or other resources to an entity in a voluntary nonreciprocaltransaction is the GAAP definition for

A) miscellaneous revenues

B) contributions

C) unconditional promises to give

D) exchange transactions

E) pledges

22. On a statement of functionalexpenses for a voluntary health and welfare organization, how areexpenses classified?

A) Health services expenses and operating expenses

B) Program services expenses and administrative servicesexpenses

C) Program services expenses and supporting services expenses

D) Operating expenses and supporting services expenses

E) Operating expenses and administrative expenses

Complex Balance Sheet

Presented below is the unaudited balance sheet as of December31, 2016, prepared by Zeus Manufacturing Corporationâsbookkeeper.

| Zeus Manufacturing Corporation Balance Sheet for the Year Ended December 31, 2016 | ||||

| Assets | Liabilities and Shareholders' Equity | |||

| Cash | $225,000 | Accounts payable | $133,800 | |

| Accounts receivable (net) | 345,700 | Mortgage payable | 900,000 | |

| Inventories | 560,000 | Notes payable | 500,000 | |

| Prepaid income taxes | 40,000 | Lawsuit liability | 80,000 | |

| Investments | 57,700 | Income taxes payable | 61,200 | |

| Land | 450,000 | Deferred tax liability | 28,000 | |

| Building | 1,750,000 | Accumulated depreciation | 420,000 | |

| Machinery and equipment | 1,964,000 | Total Liabilities | $2,123,000 | |

| Goodwill | 37,000 | Common stock, $50 par; 40,000 shares issued | $2,231,000 | |

| Total Assets | $5,429,400 | Retained earnings | 1,075,400 | |

| Total Shareholders' Equity | $3,306,400 | |||

| Total Liabilities and Shareholders' Equity | $5,429,400 | |||

Your company has been engaged to perform an audit, during whichyou discover the following information:

Checks totaling $14,000 in payment of accounts payable weremailed on December 31, 2016, but were not recorded until 2017. Latein December 2016, the bank returned a customerâs $2,000 checkmarked "NSF," but no entry was made. Cash includes $100,000restricted for building purposes.

Included in accounts receivable is a $30,000 note due onDecember 31, 2019, from Zeusâs president.

During 2016, Zeus purchased 500 shares of common stock of amajor corporation that supplies Zeus with raw materials. Total costof this stock was $51,300, and fair value on December 31, 2016, was$47,000. The decline in fair value is considered temporary. Zeusplans to hold these shares indefinitely.

Treasury stock was recorded at cost when Zeus purchased 200 ofits own shares for $32 per share in May 2016. This amount isincluded in investments.

On December 31, 2016, Zeus borrowed $500,000 from a bank inexchange for a 10% note payable, maturing December 31, 2021. Equalprincipal payments are due December 31 of each year beginning in2017. This note is collateralized by a $250,000 tract of landacquired as a potential future building site, which is included inland.

The mortgage payable requires $50,000 principal payments, plusinterest, at the end of each month. Payments were made on January31 and February 28, 2017. The balance of this mortgage was due June30, 2017. On March 1, 2017, prior to issuance of the auditedfinancial statements, Zeus consummated a noncancelable agreementwith the lender to refinance this mortgage. The new terms require$100,000 annual principal payments, plus interest, on February 28of each year, beginning in 2018. The final payment is due February28, 2025.

The lawsuit liability will be paid in 2017.

Of the total deferred tax liability, $5,000 is considered acurrent liability.

The current income tax expense reported in Zeusâs 2016 incomestatement was $61,200.

The company was authorized to issue 100,000 shares of $50 parvalue common stock.

Required:

Prepare a corrected classified balance sheet as of December 31,2016.

| Zeus Manufacturing Corporation Balance Sheet December 31, 2016 | |||

| Assets | |||

| Current Assets: | |||

| Cash | $ | ||

| Accounts receivable (net) | |||

| Inventories | |||

| Total current assets | $ | ||

| Long-Term investment, at fair value | |||

| Property, Plant, and Equipment (at cost): | |||

| Land | $ | ||

| Building | $ | ||

| Machinery and equipment | |||

| Total | |||

| Less: Accumulated depreciation | |||

| Total property, plant, and equipment | |||

| Intangible Asset: | |||

| Goodwill | |||

| Other Assets: | |||

| Cash restricted for building purposes | $ | ||

| Officer's note receivable | |||

| Land held for future building site | |||

| Total Assets | $ | ||

| Liabilities | |||

| Current Liabilities: | |||

| Accounts payable | $ | ||

| Current installments of long-term debt | |||

| Lawsuit liability | |||

| Income taxes payable | |||

| Deferred tax liability | |||

| Total current liabilities | $ | ||

| Long-Term Debt: | |||

| Mortgage payable | $ | ||

| Notes payable | |||

| Deferred tax liability | |||

| Total long-term debt | |||

| Total Liabilities | $ | ||

| Shareholders' Equity | |||

| Contributed Capital: | |||

| Common stock, $50 par value | $ | ||

| Additional paid-in capital | |||

| Total paid-in capital | $ | ||

| Retained earnings | |||

| Accumulated Other Comprehensive Loss: | |||

| Unrealized decrease in value of long-term investment | |||

| Total | $ | ||

| Less: Cost of treasury stock | |||

| Total Shareholders' Equity | |||

| Total Liabilities and Shareholders' Equity | $ | ||