ECON 208 Lecture Notes - Average Variable Cost, Competitive Equilibrium, Economic Equilibrium

13 Jul 2012

School

Department

Course

Professor

27

ECON 208 Full Course Notes

Verified Note

27 documents

Document Summary

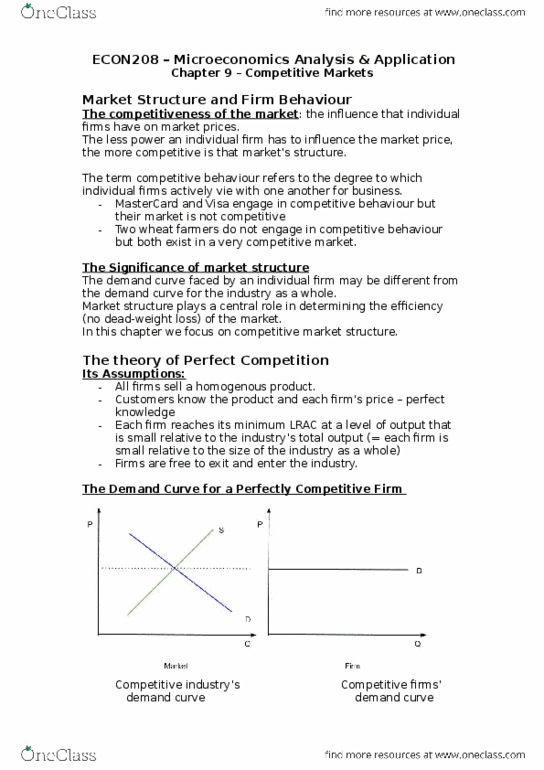

The competitiveness of the market- the influence that individual firms have on market prices. The less power an individual firm has to influence the market price, the more competitive is that market structure. Competitive behaviour refers to the degree to which individual firms actively bie with one another for business. Firms in a perfectly competitive market will see a completely flat demand curve (horizontal), even though the industry demand curve is downward sloping- because they are price taking and have no effect. This does not mean the firm could actually sell an infinite amount at the market price. Normal variations in the firms level of output have a negligible effect on total industry output. For a perfectly competitive firm, ar = mr. A firm should produce only if at some level of output, price exceeds avc (fixed costs have nothing to do with the decision because you have them no matter what.