ECON 208 Lecture 12: Chapter 8

76 views4 pages

19 Oct 2015

School

Department

Course

Professor

27

ECON 208 Full Course Notes

Verified Note

27 documents

Document Summary

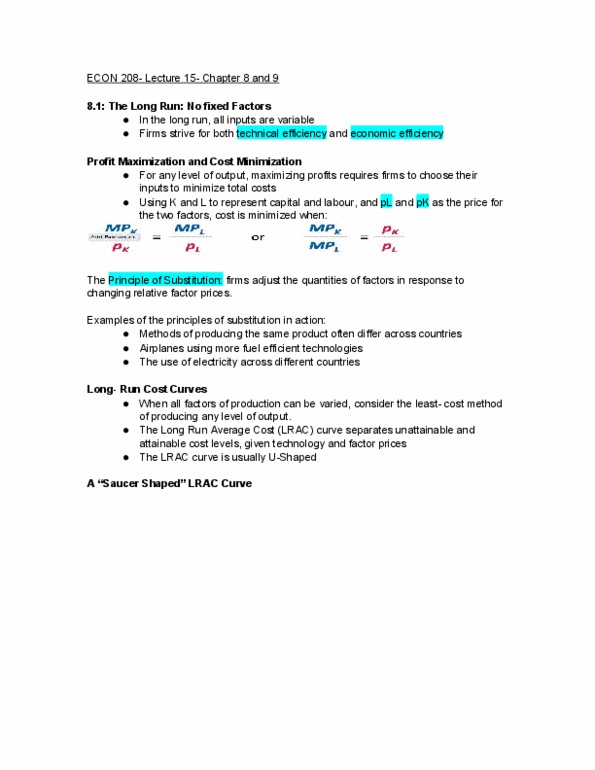

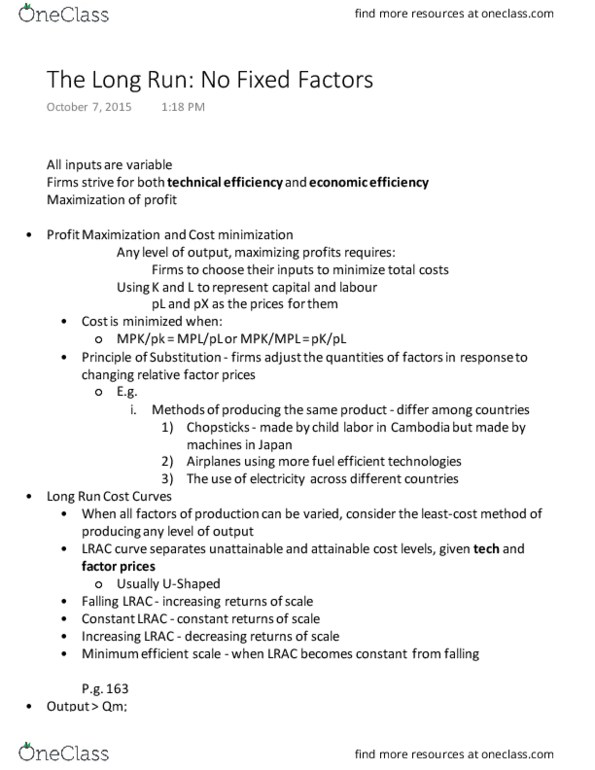

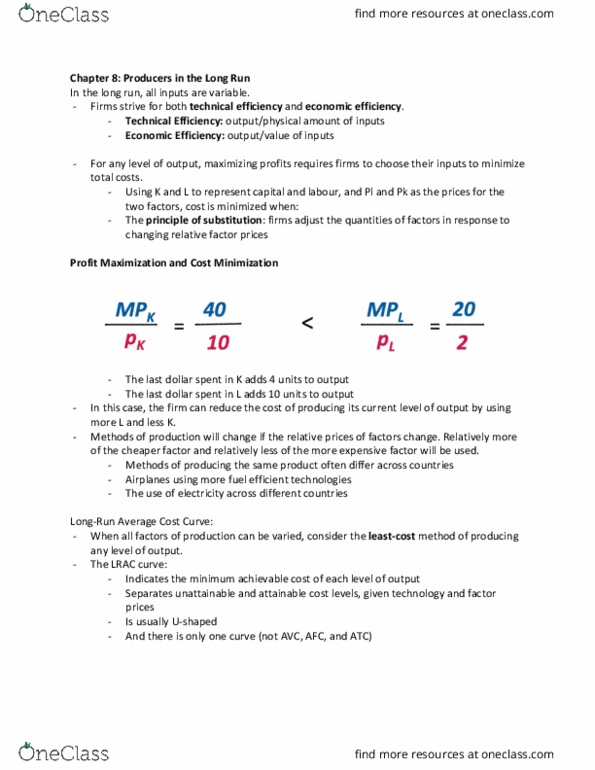

Econ 208- lecture 12- producers in the long run. In the long run, all inputs are variable. Firms strive for both technical efficiency and economic efficiency. For any level of output, maximizing profits requires firms to choose their inputs to minimize total costs. Using k and l to represent capital and labour, and pl and pk as the price for the two factors, cost is minimized when: The principle of substitution: firms adjust the quantities of factors in response to changing relative factor prices. Examples of the principles of substitution in action: Methods of producing the same product often differ across countries. When all factors of production can be varied, consider the least- cost method of producing any level of output. The long run average cost (lrac) curve separates unattainable and attainable cost levels, given technology and factor prices. When output exceeds qm, the firm has rising unit costs.

Get access

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Class+

$8 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

30 Verified Answers