MGCR 211 Lecture Notes - International Accounting Standards Board, Financial Accounting Standards Board, Canada Revenue Agency

Document Summary

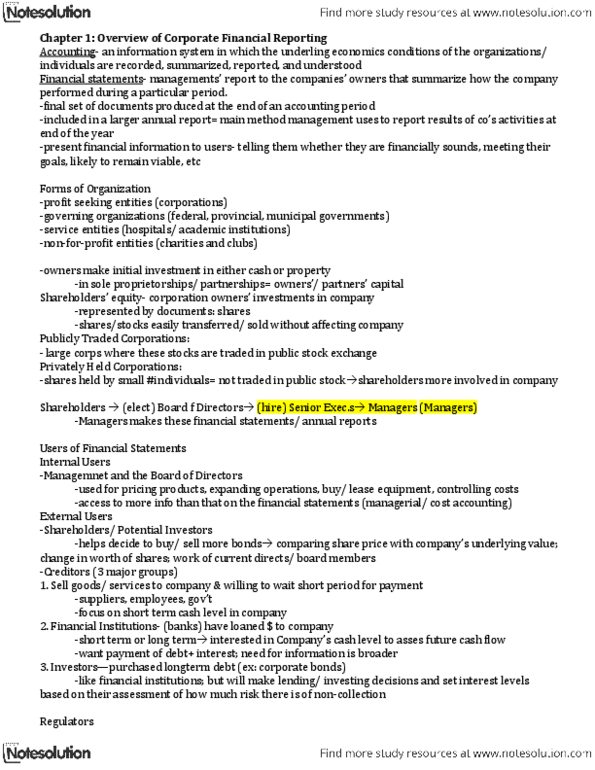

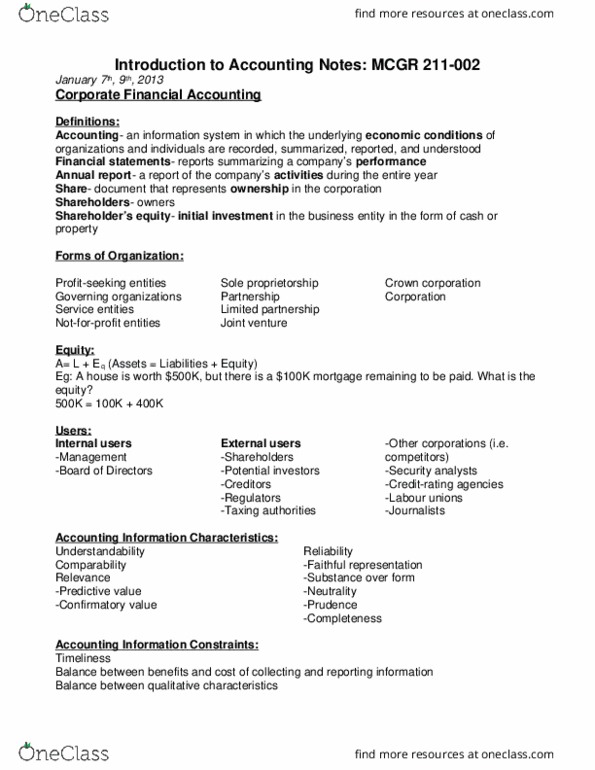

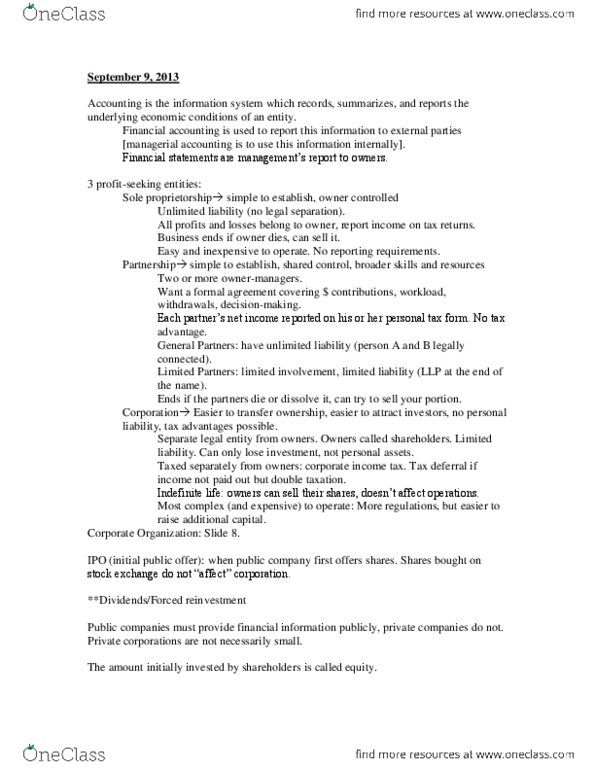

Businesses earn profits for owners: sell products and/or invest in other businesses. Accounting information system in which underlying economic conditions of organizations and, indeed of individuals- are recorded, summarized, reported, and understood: it provides the framework around which people and organizations make decisions. Financial information is captured by the accounting system is used in many different types of organization: profit seeking entities (corporations), governments, service entities (hospitals, academic institutions), not-for- profit charities/clubs. Almost every large business in canada is a corporation, other forms of business also include sole proprietorships, partnerships, limited partnerships, and crown corporations. Corporations whose stocks are traded on a public stock exchange are called publicly traded corporations. Privately held corporations shares are held by a small number of individuals not traded publicly. Shareholders typically not involved in the day-to-day proceedings of business because of this they usually elect a board of directors. Bod then hire individuals to senior executive positions to manage operations.