MGCR 211 Lecture Notes - Accounts Receivable, Current Liability, Quick Ratio

15 Jan 2013

School

Department

Course

Professor

Document Summary

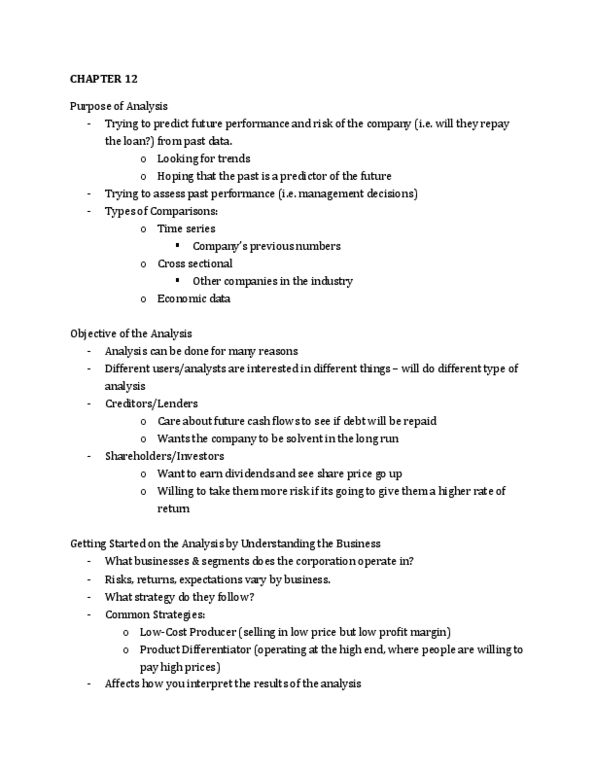

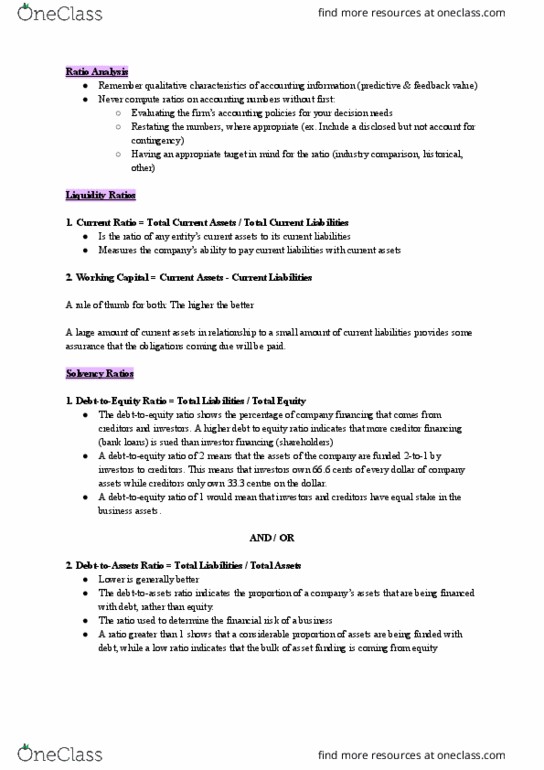

Looks at ability to meet current liabilities and assess the quality of the current assets & liabilities. Looks at using current assets to pay current debts. Shows how liquid the company is in the short term. Represent the most liquid assets that can pay of liabilities. Looks at operating cash to pay off debt. Higher ratio is better (1 or more) in order to be more sure and conservative; however, the size of the ration depends on the business and the types of current assets and liabilities that are considered. Too much means the company has opportunity costs and can thus invest. The higher ratio is, the better ability to repay debt and interest in the short term. If the quick ratio is significantly lower than the current ratio, this signifies the company has too much money tied up inventory. The higher the ratio is, the better it can manage its debt.