COMMERCE 1AA3 Lecture Notes - Lecture 6: Deferred Income, Deferral, Retained Earnings

6 Mar 2017

School

Department

Course

Professor

Document Summary

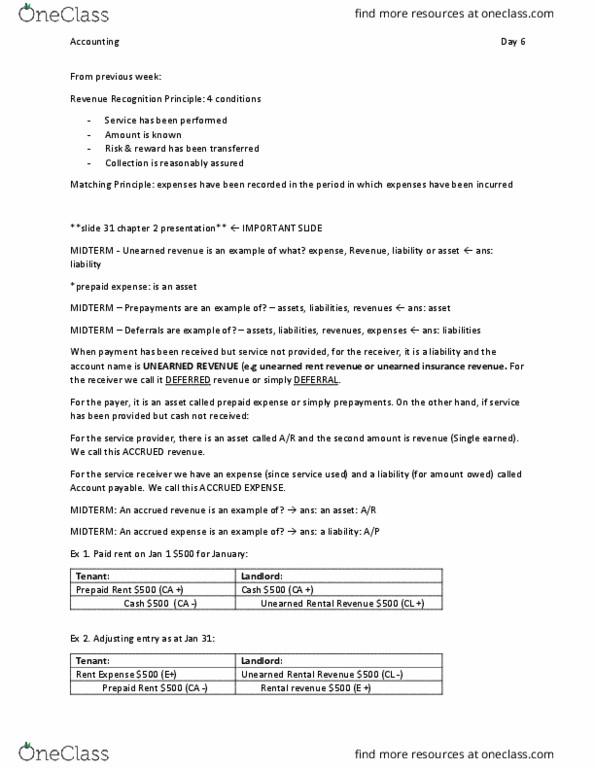

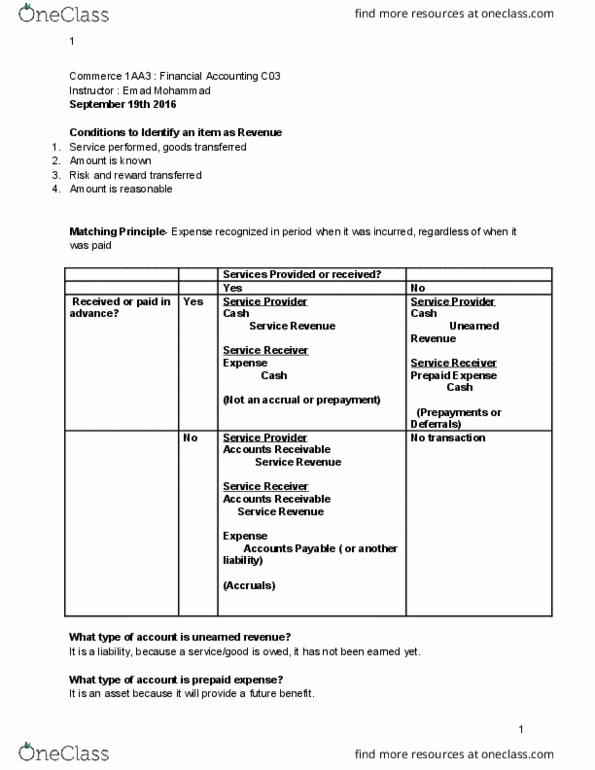

Revenue recognition: service has been performed/goods have been given, amount is known, risk and reward has been transferred, the collection is reasonably assured. Expenses are recorded in the period in which it has been incurred to generate revenue. If neither cash has been exchanged or a service has been provided then it is not a transaction. When payment has been received but service is not provided, but for the receiver, is is a liability and the account name is unearned revenue (eg unearned rent revenue or unearned insurance revenue). For the receiver it is an asset and we call it deferred revenue or simply. For the payer, it is an asset called prepaid expense or simply prepayments. On the other hand, if service provided but cash not received: For the service provider, there is an asset called accounts receivable and the second account is revenue (since earned).