COMMERCE 1AA3 Lecture 4: Chapter 5 - Lecture 4

9 Dec 2017

School

Department

Course

Professor

Document Summary

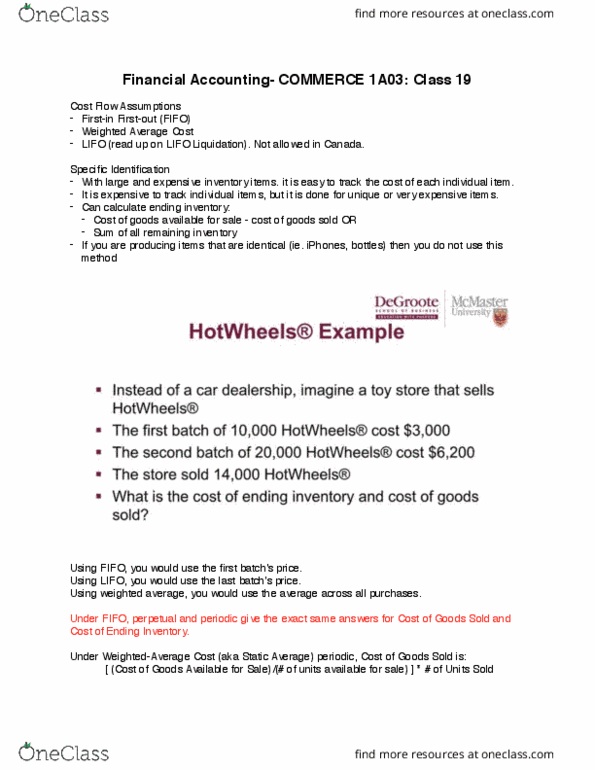

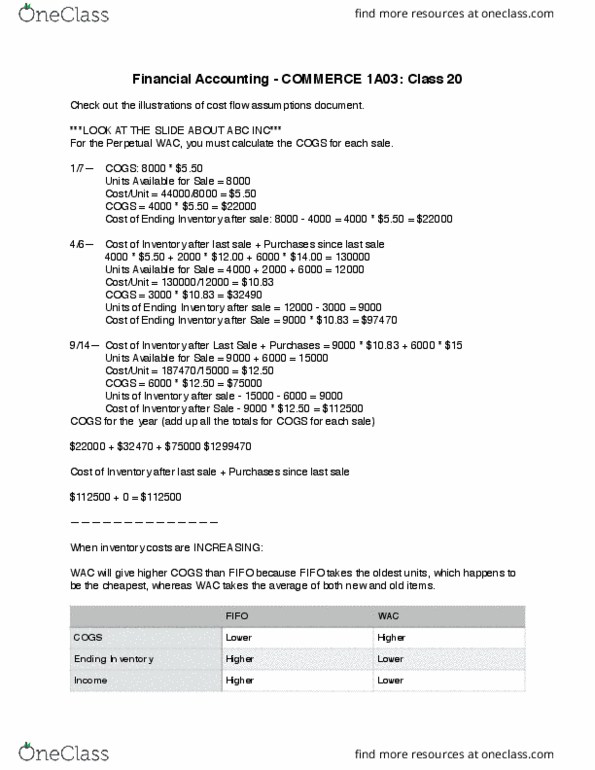

Example question (slide 40): abc inc. began 2006 with ,000 of inventory. The cost of beginning inventory (bi) is composed of 8,000 units purchased for. Units available for sale = units in beginning inventory + purchased units. = 8,000 + 2,000 + 6,000 = 22,000 units. Units sold = 4,000 + 3,000 + 6,000 = 13,000 units. Units in ending inventory = units available for sale - units sold = 22,000 - 13,000. Fifo periodic: fifo perpetual always yields the same results as fifo. Cogs, start with beginning inventory and work your way down until you account for all units sold. 8,000 units x . 5 ( do not account for 13,000 units, need 5,000 more units) + = cgafs - cogs = 24,000 - 110,000 = ,000. Cost per unit = cgafs / units afs = 242,000 / 22,000 = per unit. Cogs = units sold x cost per unit = 13,000 x 11 = ,000.