COMMERCE 1AA3 Lecture Notes - Lecture 12: Cash Flow Statement, Treasury Stock, Cash Flow

Document Summary

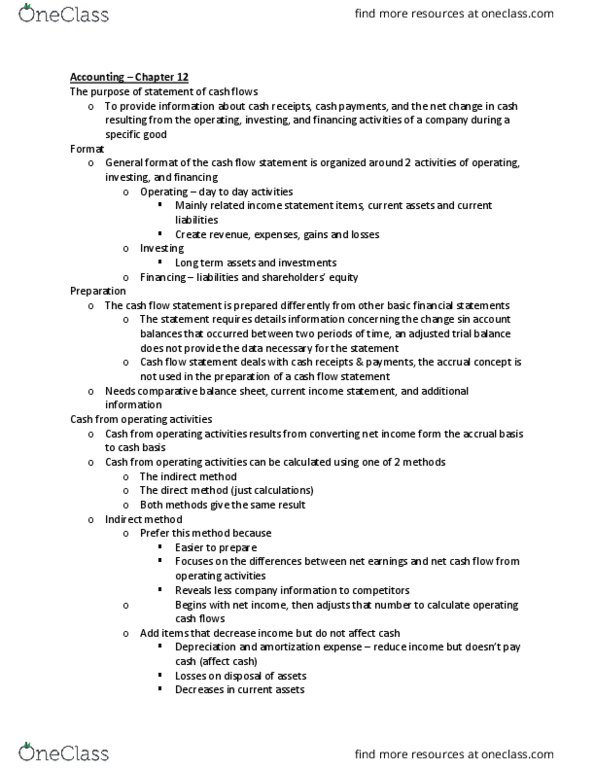

Uses of the statement of cash flows: predict future cash flows, evaluate management decisions, determine ability to pay dividends and interest, asses the relationship of net income to cash flows, compare the operating performance of different companies. Operating activities: all cash flows associated with day to day business (ex ingredients for. Subway restaurant: create revenue, expenses, gains and losses, mainly related income statement items, current assets, and current liabilities. ex. Receiving cash dividends: operating activities are the most important of the three categories because they reflect the core of the organization. A successful business must generate most of its cash from operating activities. Investing activities: non recurring always cash outflow first followed by a cash inflow later, mainly related to long-term assets and investments, activities increase and decrease long-term assets, such as computers, land, buildings, equipment, and investments in other companies. Purchases and sales of these assets are investing activities.